EU equities traded mixed yesterday, while Wall Street finished slightly lower. However, investors’ morale improved again during the Asian session today, perhaps as some more Fed officials expressed the view that the inflation surge is likely to prove to be temporary.

We also had an RBNZ rate decision, with the Bank sounding more optimistic than previously, allowing NZD-traders to increase their long positions.

Feds Help Sentiment, RBNZ Lifts The Kiwi

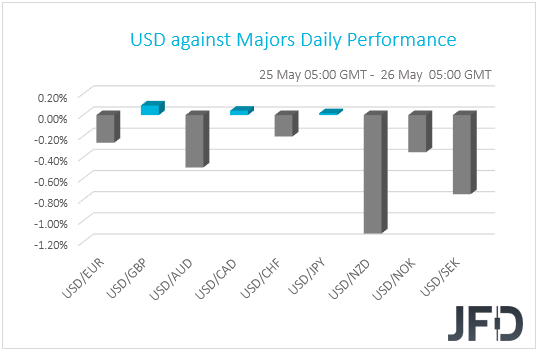

At time of writing, the US dollar continued trading lower against the majority of the other G10 currencies on Tuesday and during the Asian session Wednesday. It underperformed the most against NZD, SEK, and AUD in that order, while it was found virtually unchanged versus CAD and JPY. The greenback eked out some gains only against GBP.

The weakening of the US dollar, combined with the strengthening of the risk-linked aussie and kiwi, suggests that markets continued trading in a risk-on manner yesterday and today in Asia.

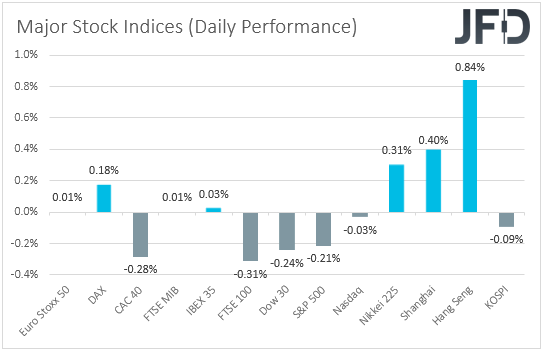

That said, turning our gaze to the equity world, we see that EU indices traded mixed, while in the US, all three of Wall Street’s main indices closed slightly in the red. Only during the Asian session today did market sentiment improve again.

With no clear catalyst behind yesterday’s cautiousness, we believe that this may have been due to getting closer to Friday and the release of the core PCE index, which is the Fed’s favorite inflation metric. However, investors gained some confidence again during the Asian session today, perhaps as some more Fed officials expressed the view that the inflation surge is likely to prove to be temporary and that it’s not the time to discuss withdrawing policy support yet.

"I have not seen anything yet to persuade me to change my full support of our accommodative stance," Chicago Fed President Charles Evans said, while San Francisco’s Mary Daly noted that "Right now, policy is in a very good place."

We also got to hear from Vice Chair Richard Clarida, who although noted that the CPI numbers were a very unpleasant surprise, the baseline case remains that the surge in inflation is transitory. He clarified that if the pressure proves to be persistent, the Fed will act to bring it down, but also added that, even though at some point they will start discussing scaling back their QE purchases, that is not the focus now.

Therefore, with more officials maintaining a dovish stance, we stick to our guns that equities still have room to trend north for a while more, while the US dollar may stay on the back foot.

That said, before getting more confident on that front, we would like to see whether Committee members will keep the same stance after the release of the PCE data on Friday.

Today, during the Asian morning, apart from developments surrounding the broader market sentiment, NZD-traders increased their long positions following the RBNZ interest rate decision.

The Bank decided to keep its monetary policy settings unchanged, but the tone of the accompanying statement and the meeting minutes was much more optimistic than previously. Instead of clearly saying that they remain ready to lower the OCR if required, officials just agreed that the OCR is the preferred tool to respond to future economic developments in either direction.

Most importantly though, they noted that on current projections, the OCR eventually increases over the medium-term, with their forecasts suggesting that this may happen in the second half of 2022.

As for our view, conditional upon further improvement in the broader market sentiment, the upbeat language of the RBNZ is likely to help the kiwi to continue performing well, especially against the US dollar, which we expect to stay pressured due to a dovish Fed.

NASDAQ 100 – Technical Outlook

After the mid-May reversal to the upside, the NASDAQ 100 cash index continues to slowly grind higher, as it trades above a short-term tentative upside support line taken from an intraday swing low of May 19. The price is currently above all of its EMAs on our 4-hour chart, which adds more positivity, at least to the near-term outlook.

If the cash index jumps above yesterday’s high, at 13740, this will confirm a forthcoming higher high, potentially setting the stage for higher areas.

NASDAQ 100 could then drift to the high of May 7, at 13823, a break of which might clear the path to the 13958 level, marked by the current highest point of May.

On the other hand, if the price breaks the aforementioned upside line and falls below the 13609 hurdle, marked by the low of May 25, that could attract more sellers into the game.

NASDAQ 100 might then drift to the 13572 obstacle, or to the 13480 zone, marked by intraday swing lows of May 20 and 24. If the bears continue to dictate the rules, the index may easily drop to the current lowest point of this week, at 13360.

NZD/USD – Technical Outlook

NZD/USD made a strong move higher during the Asian trading session, after the RBNZ policymakers stated that they expect a rate hike by September 2022.

The pair managed to climb and stay above the 0.7305 hurdle, which is now the previous highest point of May. At the same time, the rate continues to balance well above its steep short-term upside support line taken from the low of May 24. As long as NZD/USD remains above that upside line, we will continue aiming higher.

A further push north could bring the pair towards the 0.7363 barrier, marked by an intraday swing low of Feb. 24 and the high of Feb. 26, where the rate may stall for a bit, or even retrace back down from there.

That said, as long as NZD/USD stays above the aforementioned upside line, the bulls might stay interested. If so, the pair could get lifted higher again and if this time it is able to overcome the 0.7363 obstacle, the next potential target might be at 0.7393, marked by an intraday swing high of Feb. 24 and an intraday swing high of Feb. 25.

Alternatively, if the pair breaks the previously discussed upside line and then falls below the 0.7250 hurdle, marked by yesterday’s high, that could temporarily spook the bulls from the field.

The bears might take control and drive NZD/USD to the 0.7222 obstacle, or to the 0.7200 zone, marked by an intraday swing low of May 24. If the slide continues, the next possible target may be at 0.7180, marked by an intraday swing high of May 24, or the pair could test another short-term upside support line drawn from the low of May 4.

As For The Rest Of Today's Events

The calendar today appears very light, with the only release worth mentioning being the EIA (Energy Information Administration) report on crude oil inventories for last week, with expectations pointing to a 1.050mn barrels decrease following a 1.321mn barrels increase the week before.

However, bearing in mind that yesterday, the API report revealed only a 0.439mn barrels slide, we would consider the risks surrounding the EIA report as tilted to the upside.

We also have two speakers on today’s agenda and those are Fed Board Governor Randal Quarles and BoC Governing Council member Timothy Lane.

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes 6 winning stock portfolios chosen by our advanced AI. In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. Which stock will be the next to soar?

Unlock ProPicks AI