- Dollar stays subdued as US CPI data awaited for clues on peak inflation

- Euro edges up as ECB preps for summer rate hike

- Equities attempt a rebound, falling infections in China lend some support

Dollar slips before US inflation reveal

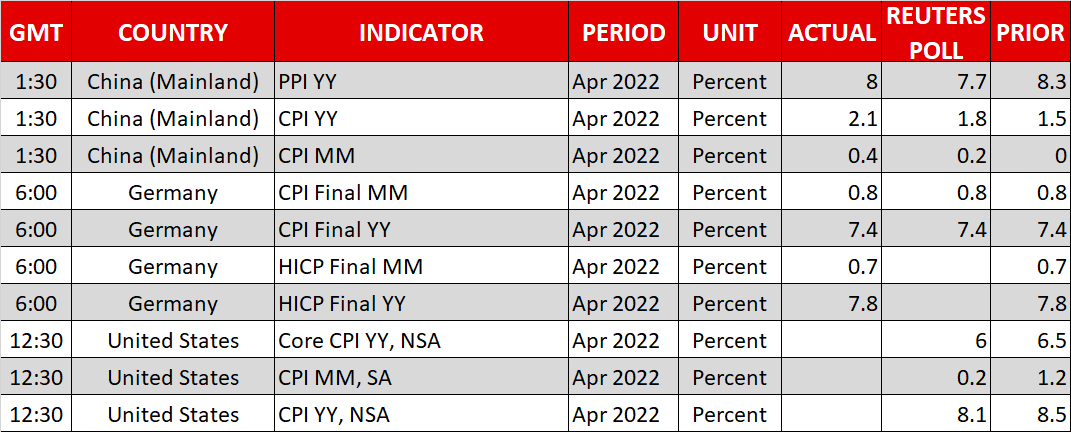

Markets were in a cautiously optimistic mood ahead of the April inflation report out of the United States later on Wednesday, as investors geared up for a possible soft print this time after months of acceleration in the headline figure. The consumer price index had jumped by a 41-year high of 8.5% year-on-year in March but the surge in prices is predicted to have moderated in April to 8.1%.

Following some preliminary indications in the March numbers that inflation is slowing, hopes are growing that a peak is near. Whilst that would not stop the Fed from pushing up borrowing costs aggressively for several more meetings, it would at least cap rate hike expectations.

The question is, would peak inflation necessarily be the silver lining investors are looking for? Policy tightening by the Fed will only go so far in stemming price pressures as a lot of the inflation is imported, arising from the ongoing supply-chain issues and the rally in commodities. There’s a real prospect that it will take far longer than anyone is anticipating for inflation to fall to the Fed’s 2% target even if we are now seeing price growth level off.

Until there’s a considerable easing of inflationary pressures, Treasury yields and the US dollar may stay elevated at their current high levels. Nevertheless, the dollar is vulnerable to a sharp near-term correction if today’s CPI numbers are weaker than expected.

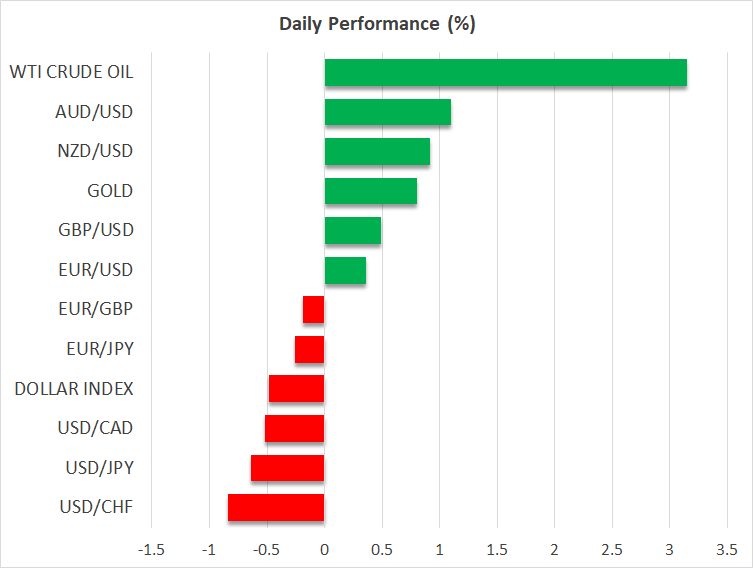

The dollar index was last quoted down by about 0.3%, holding near Monday’s 20-year top of 104.19. The 10-year Treasury yield, however, has pulled back more substantially, falling to around 2.94% at the European open.

ECB rate hike talk gathers steam, bolsters euro

The softer greenback provided some breathing space for downtrodden currencies. The euro climbed to around $1.0570 and the pound recovered above $1.2350. But the biggest gainers were the Australian and New Zealand dollars, which rose by about 0.7%.

Ebbing risk-off sentiment and higher commodity prices are likely lifting the aussie and kiwi, although the loonie is lagging slightly despite the 3% rebound in oil prices today. Sterling is lacking any boost of its own and is only advancing because of the sluggish dollar.

What is more interesting, however, is how well the euro has held up during May when other majors were pummelled by the greenback. The single currency has been steadily crawling higher over the past 10 days as the hawkish voices at the ECB have been getting louder lately.

A string of ECB policymakers have flagged a July rate hike in the last 24 hours, including the central bank chiefs of Germany and France. President Christine Lagarde’s language has been less explicit but is increasingly aligned with that of the hawks.

With a July liftoff looking more and more likely, the euro may have bottomed. What traders will now be watching is how resilient economic growth will be in the face of rising interest rates around the world.

Stocks set to extend gains; falling China cases offset growth jitters

In the United States, President Biden yesterday gave the Fed his blessing to continue to tighten policy to contain high inflation, while Fed officials seem to be in agreement that the central bank needs to hike rates by 50 basis points at least at the next two meetings.

The sudden reversal in monetary policy globally towards normalization has knocked confidence in equity markets. The S&P 500 closed higher on Tuesday for the first time in three sessions but could only manage gains of 0.25%. The Nasdaq Composite put up a more convincing fight, rising 1% and e-mini futures point to similar gains today.

Still, there’s no clear sign yet that the bear market is coming to an end, but risk appetite could benefit in the short term if China begins to ease its lockdown restrictions. Chinese authorities reported that eight districts in Shanghai recorded no community transmission on Wednesday, raising hopes that infections may soon drop low enough for the draconian measures to be abandoned.

China’s benchmark CSI 300 index (+1.4%) climbed for a second day and shares in Europe were higher too.

On Wall Street, earnings will be back in focus today as Walt Disney (NYSE:DIS) reports its results after the closing bell.