The economy’s fundamentals determine the stock market’s medium-long term outlook. Technicals determine the stock market’s short-medium term outlook. Here’s why:

- The stock market’s long term risk : reward is no longer bullish.

- The medium-term direction (e.g. next 6-9 months) is mostly mixed, although there is a bullish lean.

- The stock market’s short term is neutral

We focus on the long term and the medium term.

Long Term: Valuations

Only two factors affect the stock market’s long term outlook: valuations and fundamentals (macro).

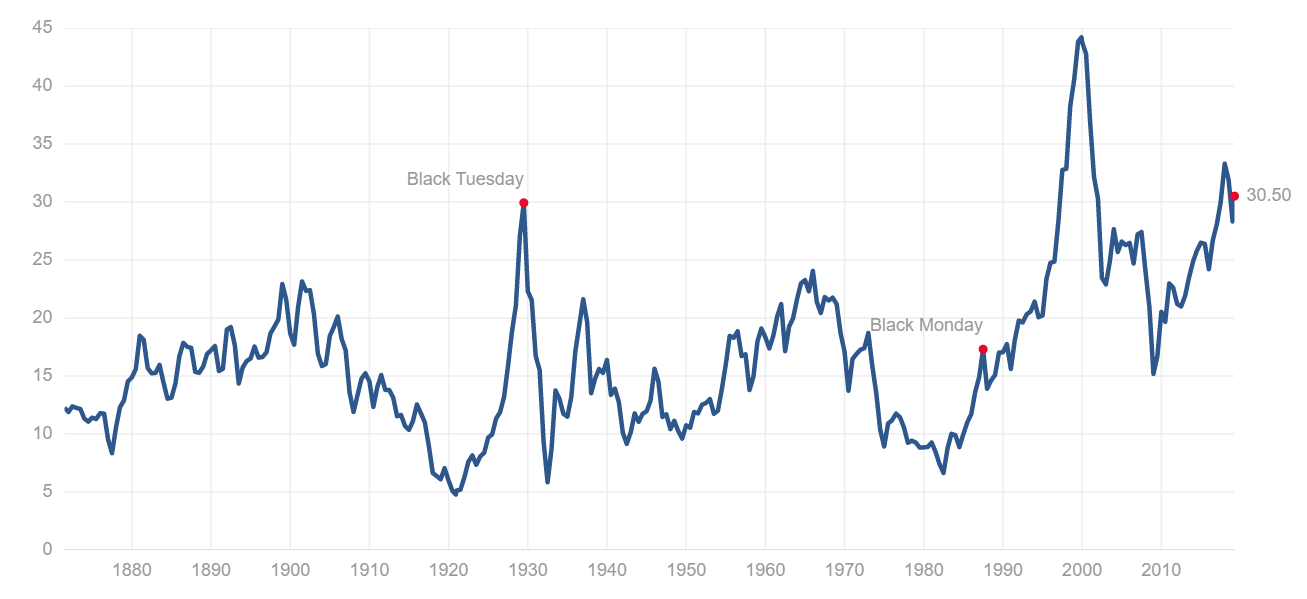

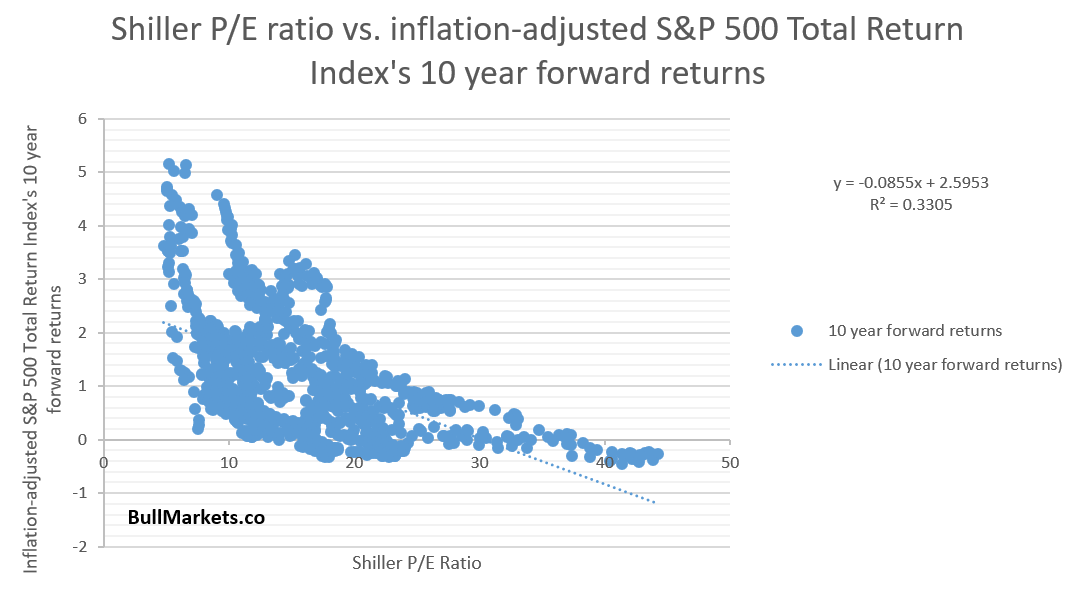

The stock market’s valuation is high right now. Here’s the Shiller P/E ratio and Tobin’s Q ratio, two popular valuation metrics.

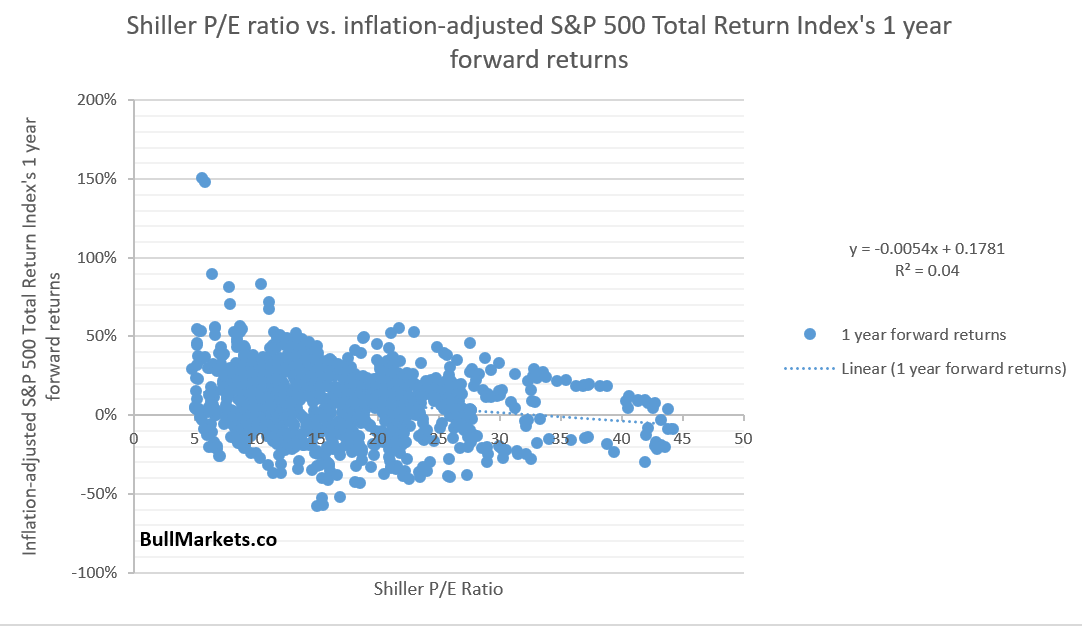

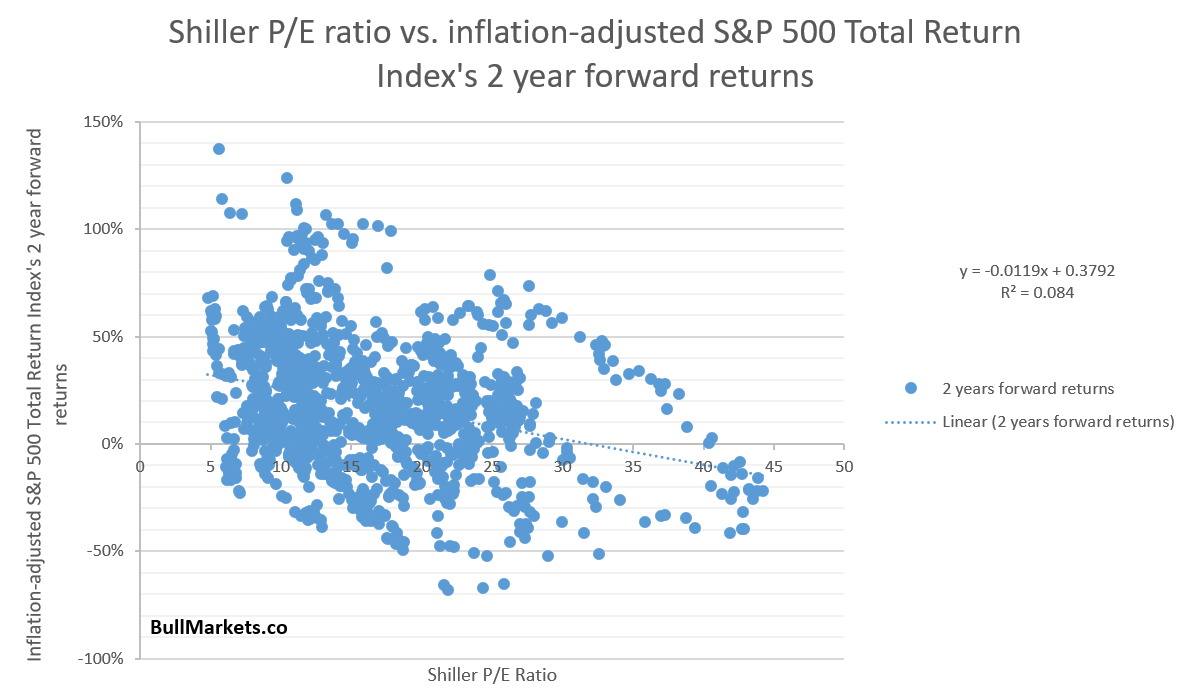

Contrary to popular belief, valuations have very little impact on where the stock market will go over a 1-2 year period. Looking at the r-squares below, it’s clear that valuations only significantly impact the stock market’s 5-10 year forward returns. (R-squared goes from 0.04 to 0.33)

High valuations create the preconditions for a bear market – necessary but not sufficient. So what causes a bear market?

Fundamentals.

- Low valuations + recession = big correction (e.g. 20-30%)

- High valuations + recession = bear market (e.g. 40-50%)

Think of a “recession” like jumping out of a building, and “valuations” as which floor you are jumping out from. If you jump out from the first-floor window (i.e. low valuations), you will probably break a leg. If you jump out from the 10th-floor window (i.e. high valuations), you will probably die.

Given that valuations are high rate now, the next recession-driven stock market decline will be much bigger than a normal -20% decline.

Long Term: Fundamentals

While the bull market could keep going on, the long term risk : reward no longer favors bulls. Towards the end of a bull market, risk : reward is more important than the stock market’s most probable long term direction.

Some leading indicators are showing signs of deterioration. The usual chain of events looks like this:

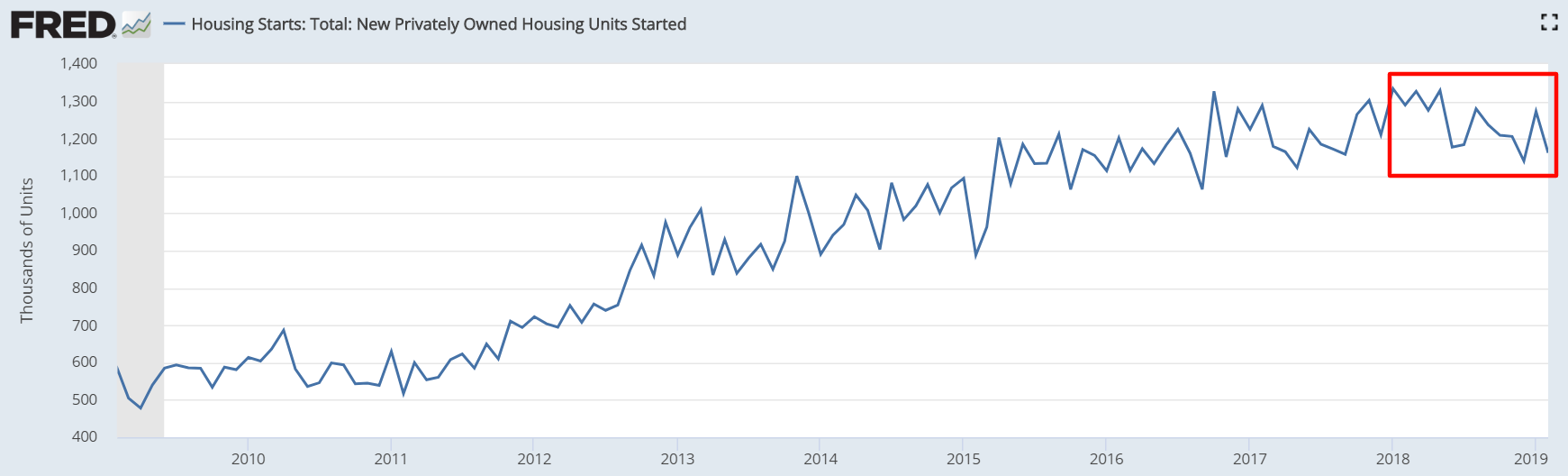

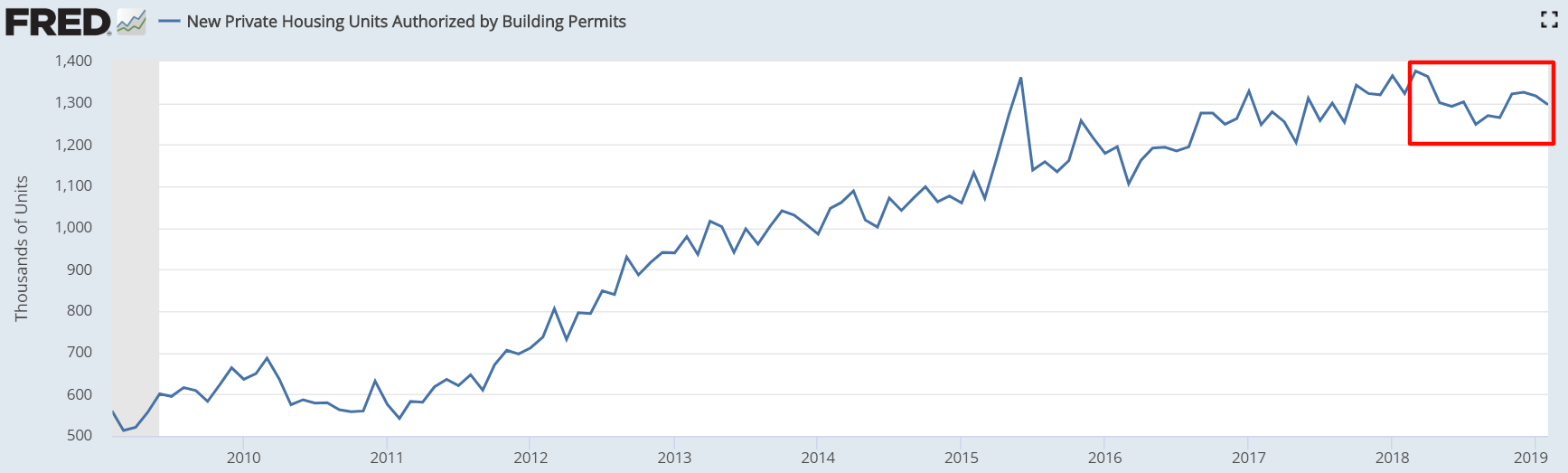

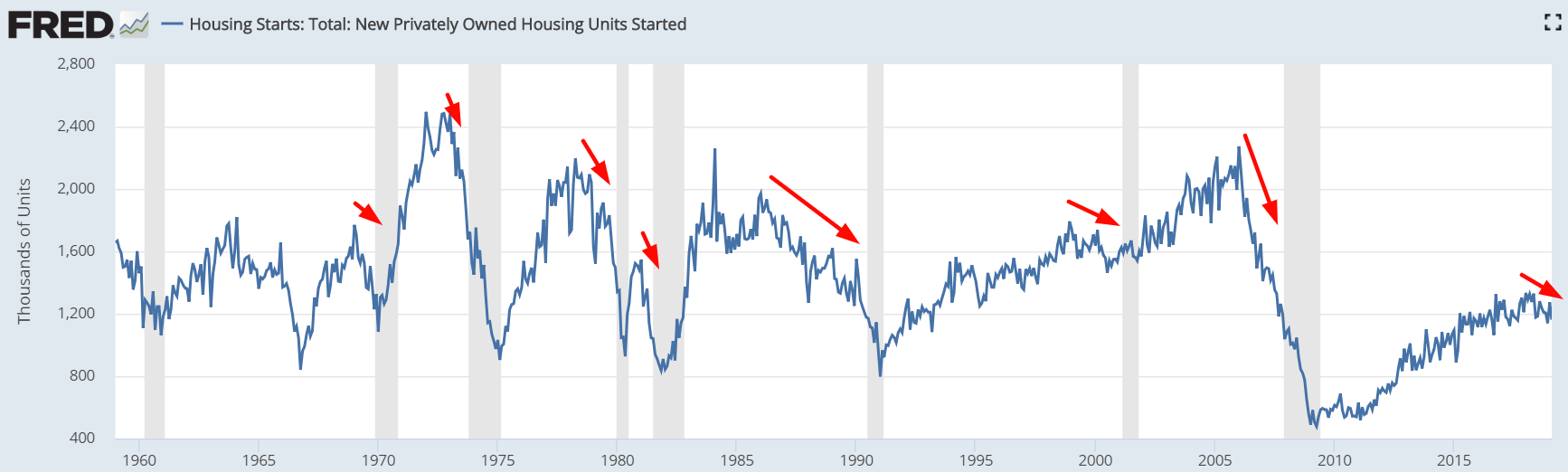

- Housing – the earliest leading indicators – starts to deteriorate. This has occurred already

- The labor market starts to deteriorate. Meanwhile, the U.S. stock market is in a long term topping process. We are in the early stages of this process, but the deterioration is not significant.

- Other economic indicators start to deteriorate. The bull market is definitely over, and a recession has started. A U.S. recession is not imminent right now

*All economic data charts are from FRED

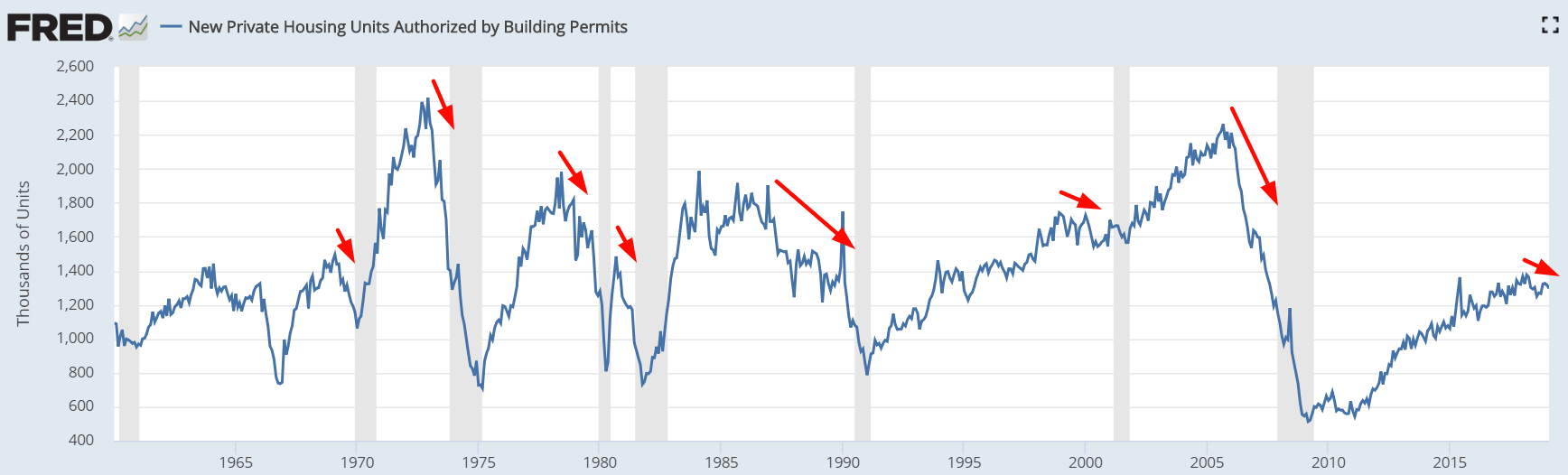

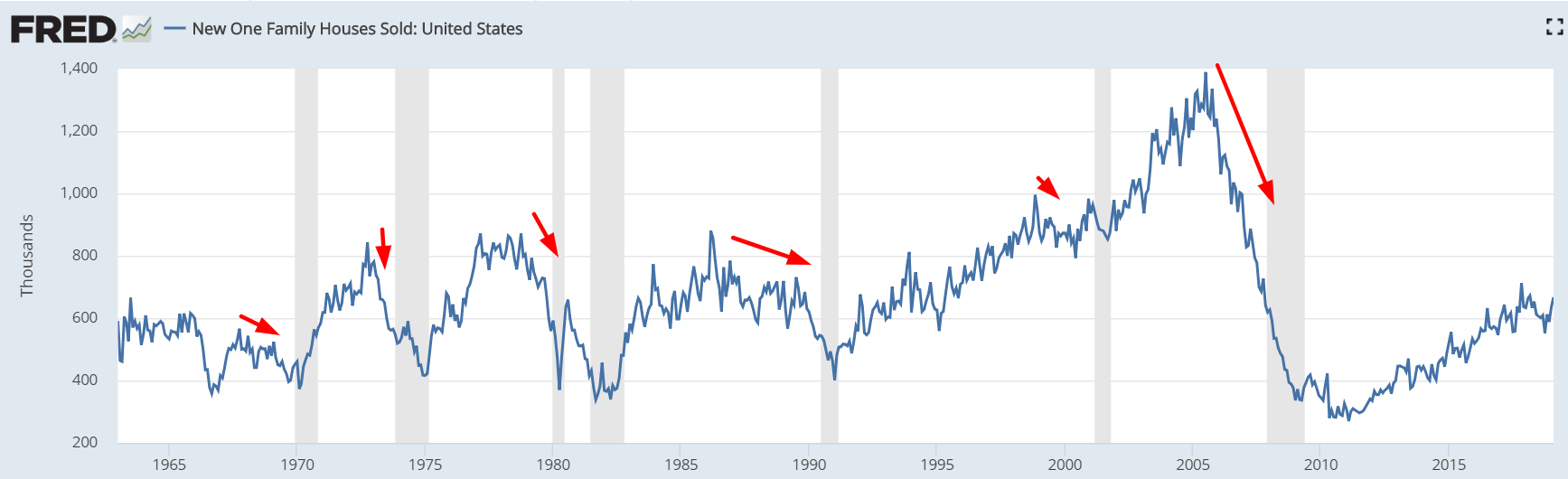

Housing

The housing sector is trending downwards/sideways. Here’s Housing Starts, Building Permits, and New Home Sales.

In the past, these three housing indicators trended downwards before bear markets and recessions began. You can see that the deterioration right now is mmildermild than the deterioration pre-2007, which is why I think “the next one” won’t be as bad as 2008.

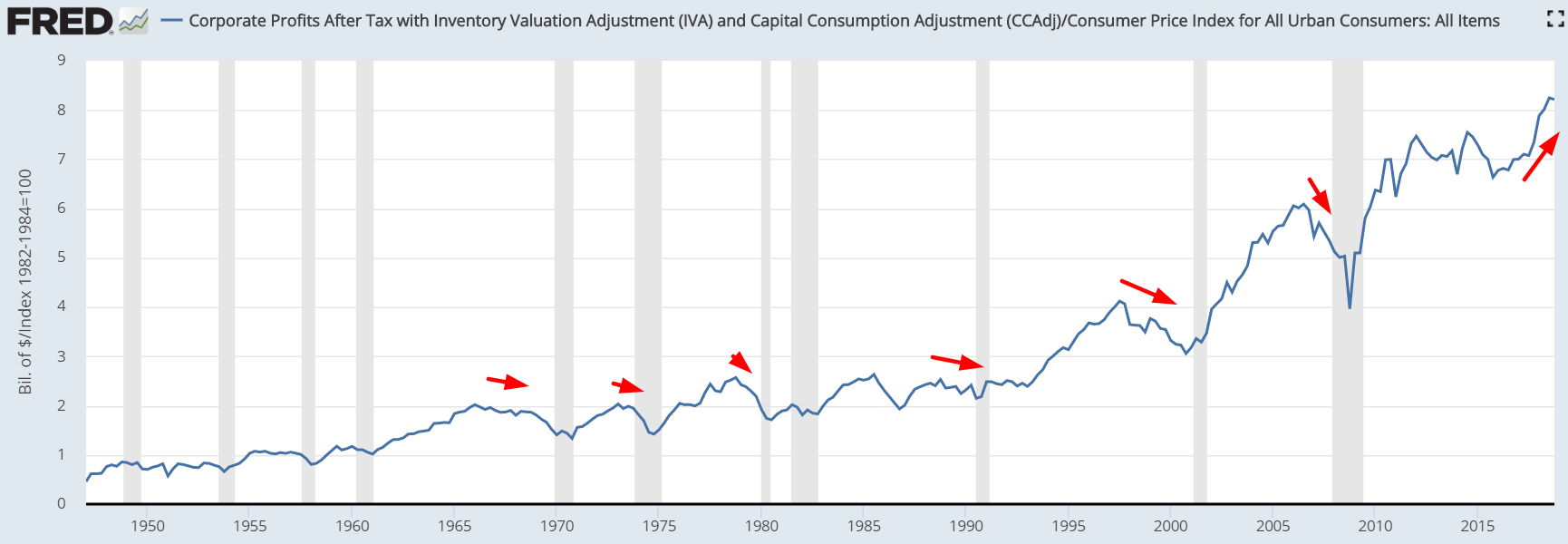

Corporate Profits

Inflation-adjusted corporate profits are still trending higher. This is encouraging for 2019. Historically, inflation-adjusted corporate profits trended downwards for a few quarters before bear markets and recessions began.

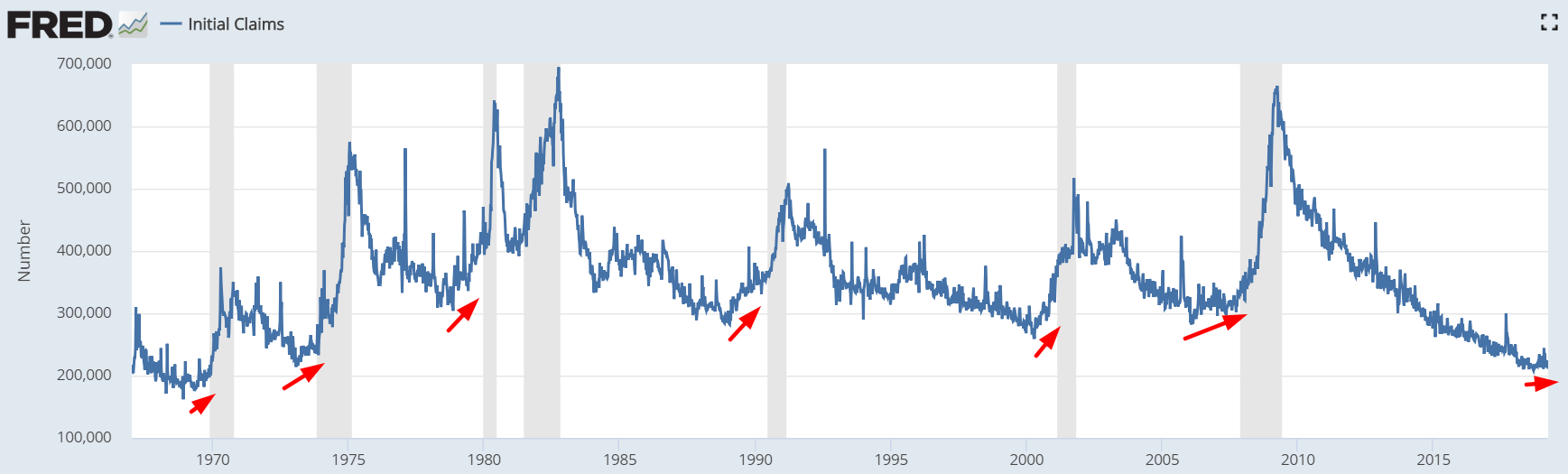

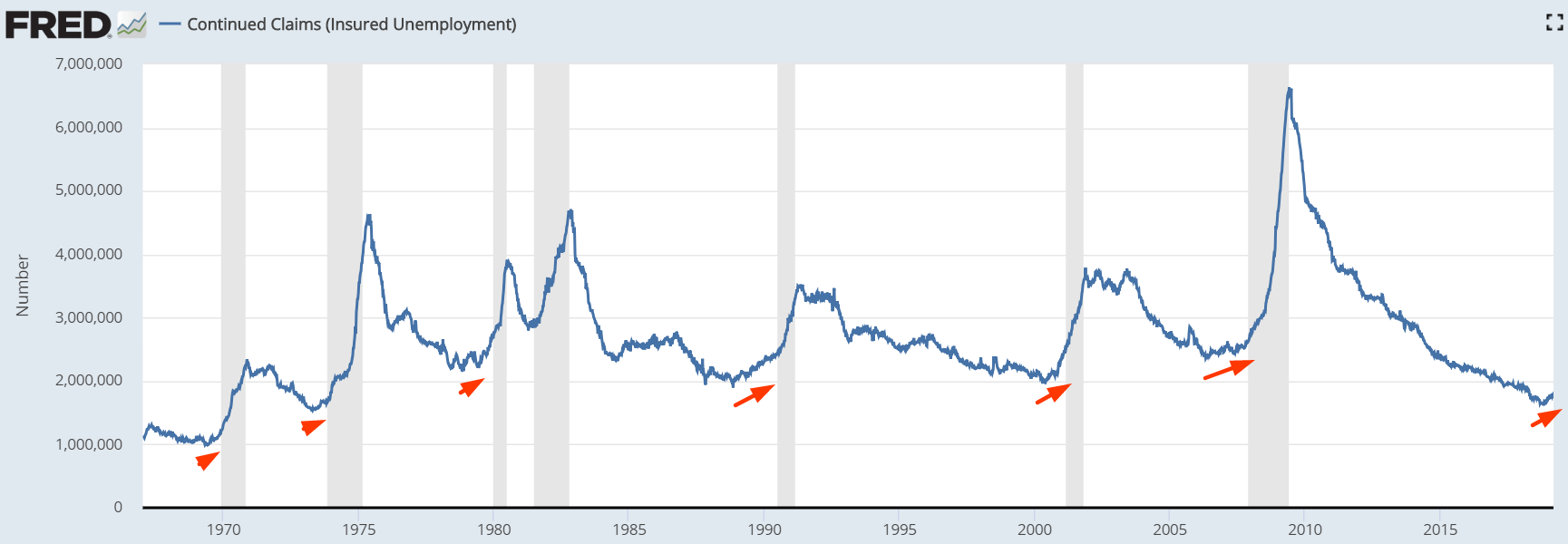

Labor market

Initial Claims is trending sideways from a very low level while Continued Claims is trending upwards.

In the past, these 2 figures trended higher before bear markets and recessions began.

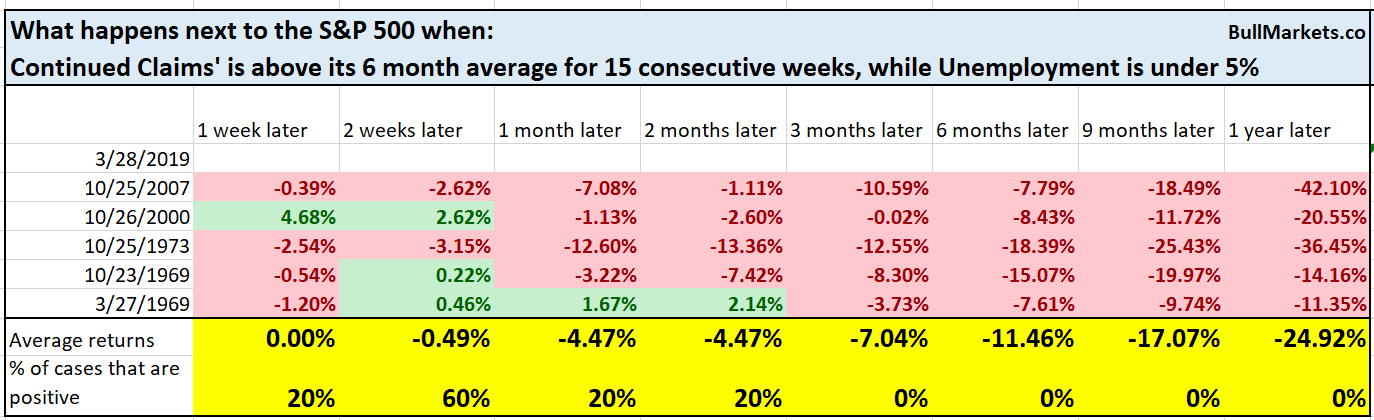

Continued Claims has been above its 6 month average for 15 consecutive weeks, while Unemployment is under 5% (late-cycle). Historically, this is bearish for the S&P on all time frames.

This is worth monitoring, but do not panic immediately. It’s best to use Initial Claims together with Continued Claims. While Continued Claims is trending up, Initial Claims is still mostly trending sideways. So not immediately bearish, but watch out if this persists for a few more months.

Industrial Production

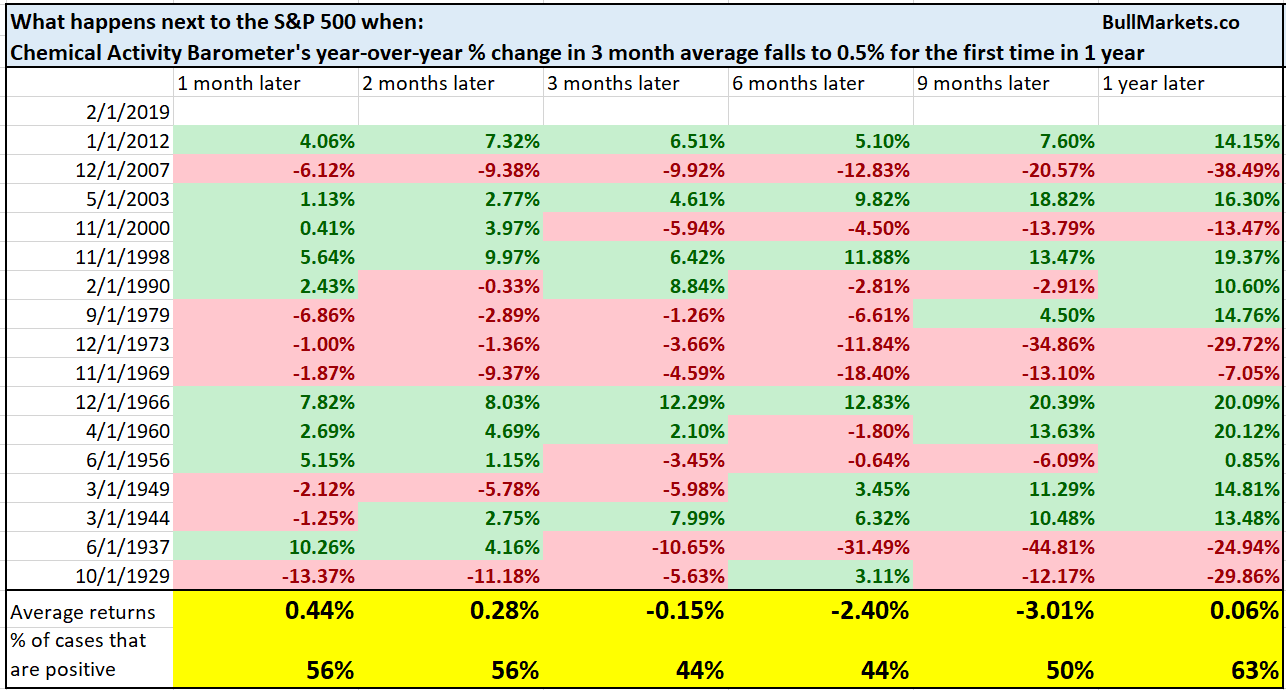

The year-over-year % change in the 3 month average of the Chemical Activity Barometer is now almost at zero. This can be used as a leading indicator for Industrial Production YoY % growth.

Here’s what happens next to the S&P 500 when the year-over-year change falls to 0.5%

The S&P’s forward returns are slightly less bullish than random.

Global trade slowdown

Global economic growth is slowing down. This economic weakness is more pronounced outside of the U.S. than within the U.S. This is the 3 month % change in the 3 month average of global trade growth.

Here’s what happens next to the S&P when the 3 month % change in global trade’s 3 month average falls below -1%.

I would treat this as a warning sign rather than an outright bearish sign. You should generally be hesitant when using ex-U.S. economic data to predict the U.S. stock market.

Late-cycle signs

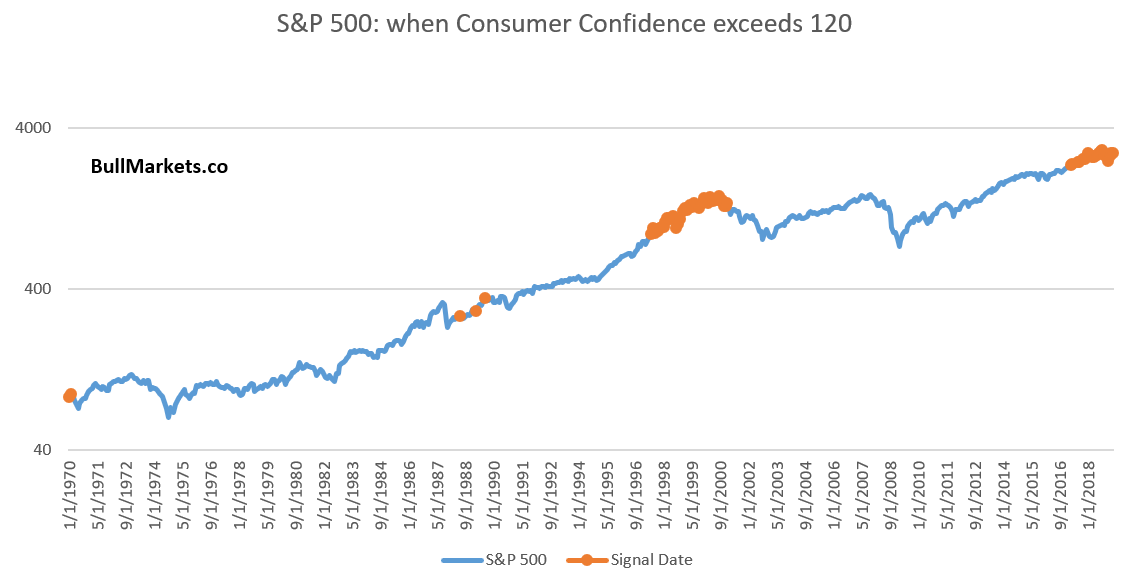

Consumer Confidence remains extremely high, which demonstrates that the current economic expansion and bull market are late-cycle. (Remember that “late-cycle” does not mean the bull market will end today).

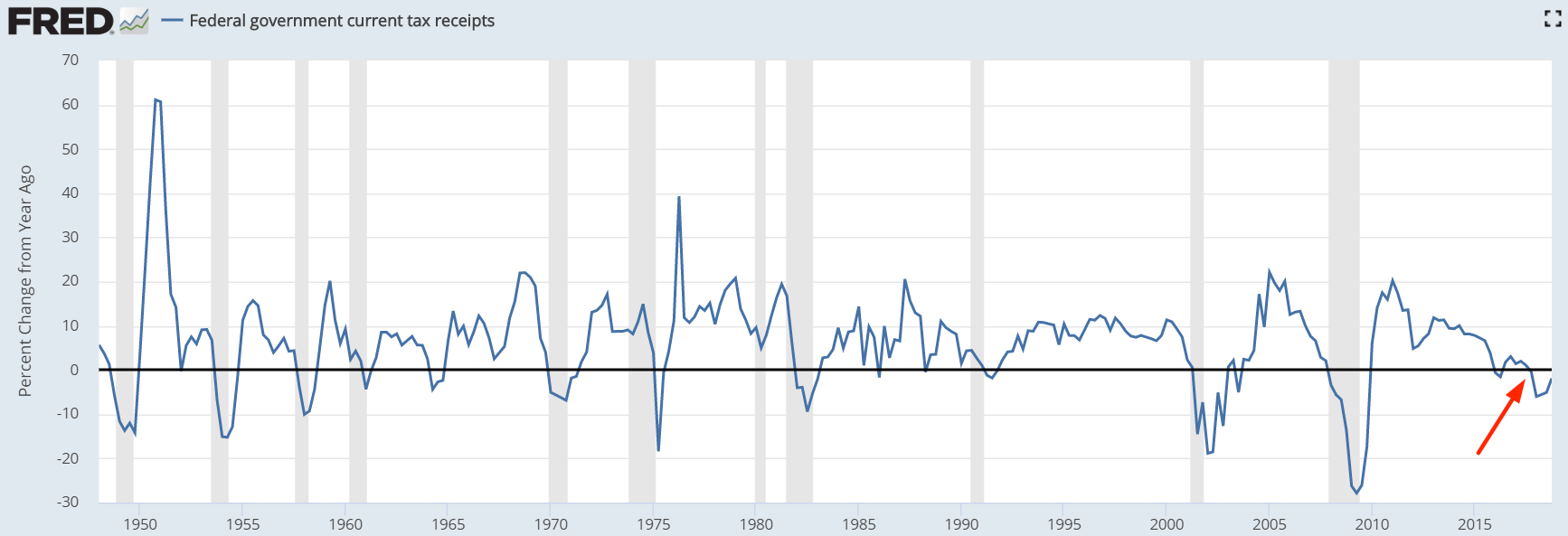

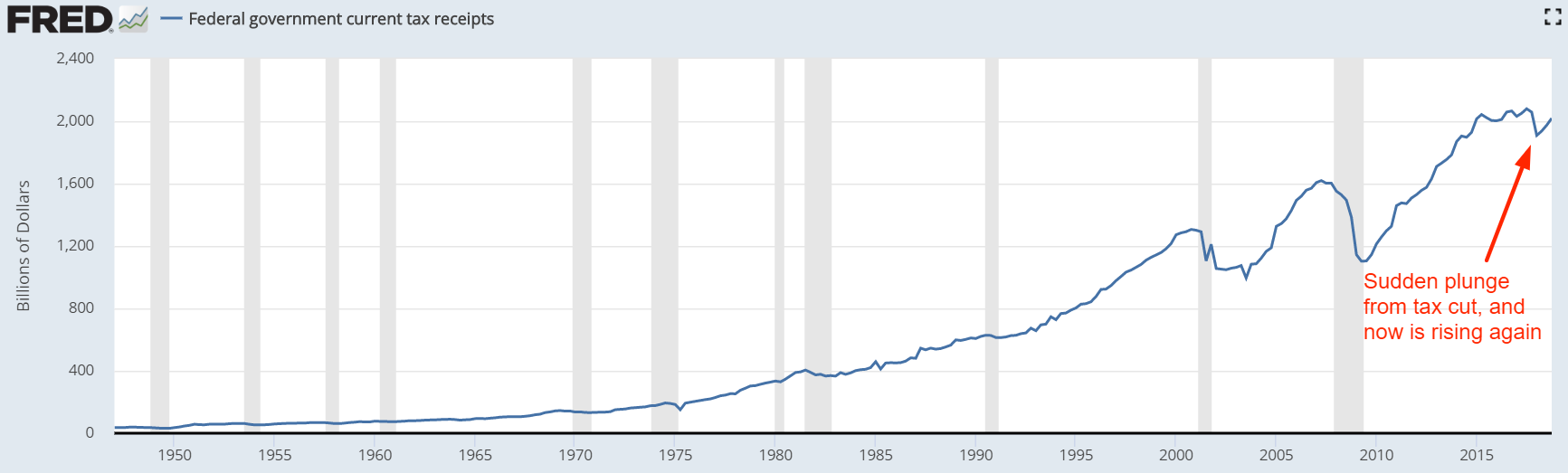

What not to worry about: Federal tax receipts

% growth in Federal tax receipts has been negative for a few consecutive quarters. Some traders see this is “a hallmark of economic recessions”.

It’s not. While many dips in Federal tax receipts are due to economic recessions (slowing economy = fewer tax $), the recent dip is due to Trump’s tax cut. Same symptom, different reasons.

You can see that tax receipts are once again rising now that the effects of Trump’s tax cuts are wearing off. Why are tax receipts rising? Because the economy is still growing.

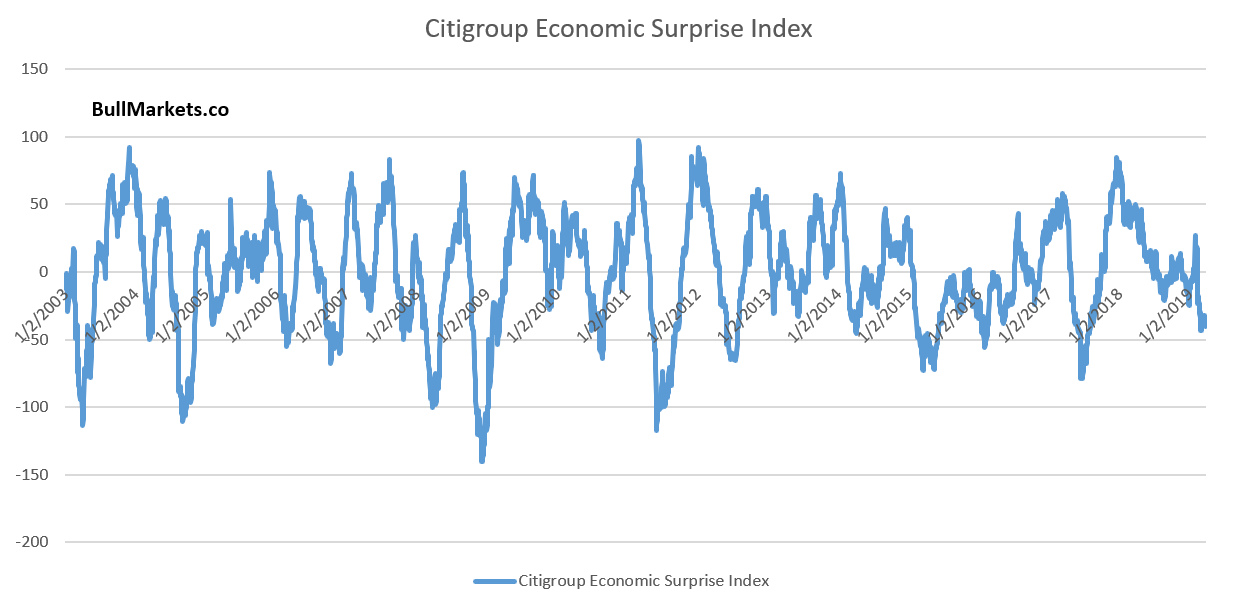

What not to worry about: Citigroup Economic Surprise Index

The (Citigroup) Economic Surprise Index measures how recent U.S. economic data releases stack up against analysts’ expectations. The index has “decoupled” with the S&P recently

While on the surface this looks scary, a rational trader/investor would look at the bigger picture and examine how useful these correlations actually are. Correlations break all the time. Not exactly “decoupling”.

Here’s a longer term look at the (Citigroup) Economic Surprise Index.

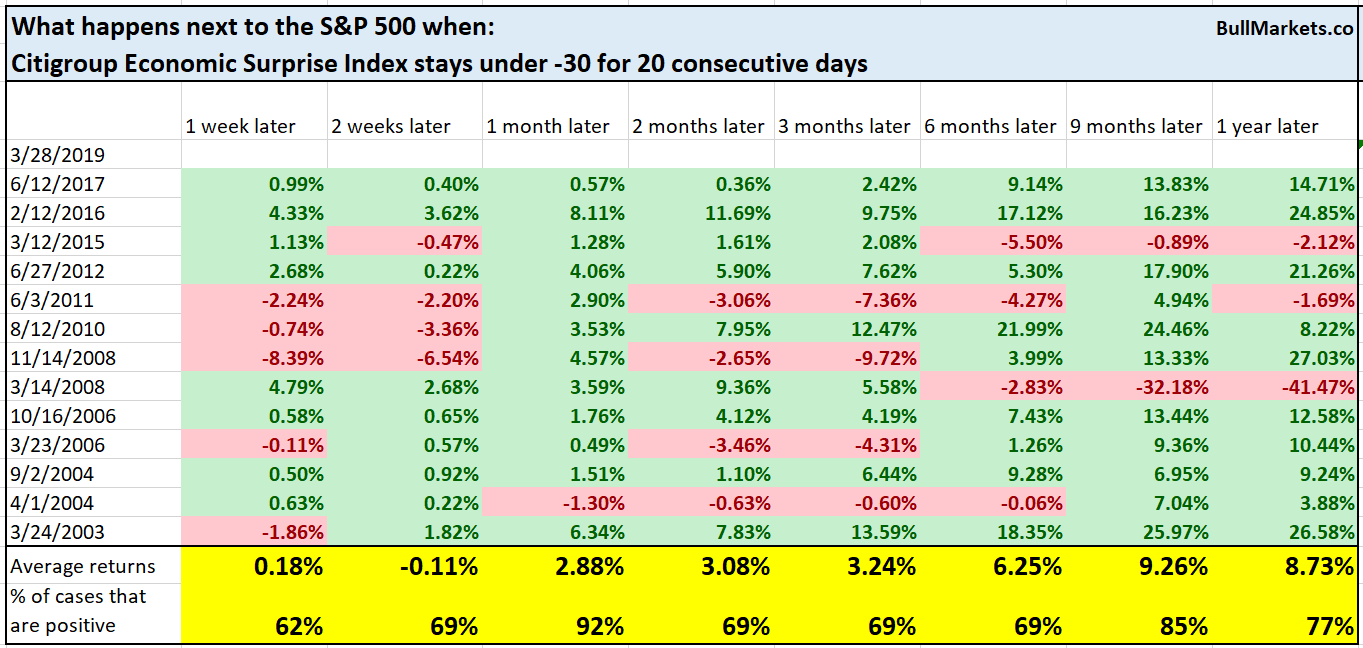

The Citigroup Economic Surprise Index has been under -30 for 20 consecutive days, which is quite low. Historically, such low readings were more bullish than bearish for stocks 1 month and 9 months later.

What not to worry about: Baltic Dry Index

Baltic Dry Index (a measure of global shipping) has diverged with the S&P recently.

This is not consistently bearish for the stock market.

You can see that this has happened consistently from 2009-present. The current bull market has seen continued weakness in global shipping, which is probably a hallmark of foreign economic weakness (European crisis, China crisis, Turkey crisis, Argentina crisis, emerging markets crisis….).

Conclusion:

The stock market’s biggest long term problem right now is that as the economy reaches “as good as it gets” and stops improving, the long term risk is to the downside.

The end of a bull market is always very tricky to trade. The stock market can go up a lot in its final year, even if the macro economy is deteriorating (e.g. 2006-2007). That’s why it’s better to focus on long term risk : reward instead of trying to time exact tops and bottoms. Even when you think the top is in, the stock market could very well surge for 1 more year. (Just ask the people who thought that the dot-com bubble would end in 1998. It lasted another 1.5 years).

Medium Term

*For reference, here’s the random probability of the U.S. stock market going up on any given day, week, or month.

Monthly statistics

These stats use each month’s CLOSE $ (so 3/1/2019 = the closing price for March 2019).

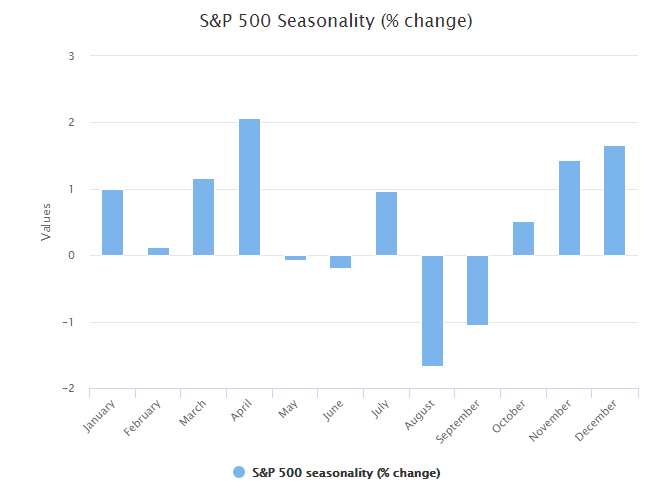

Seasonality

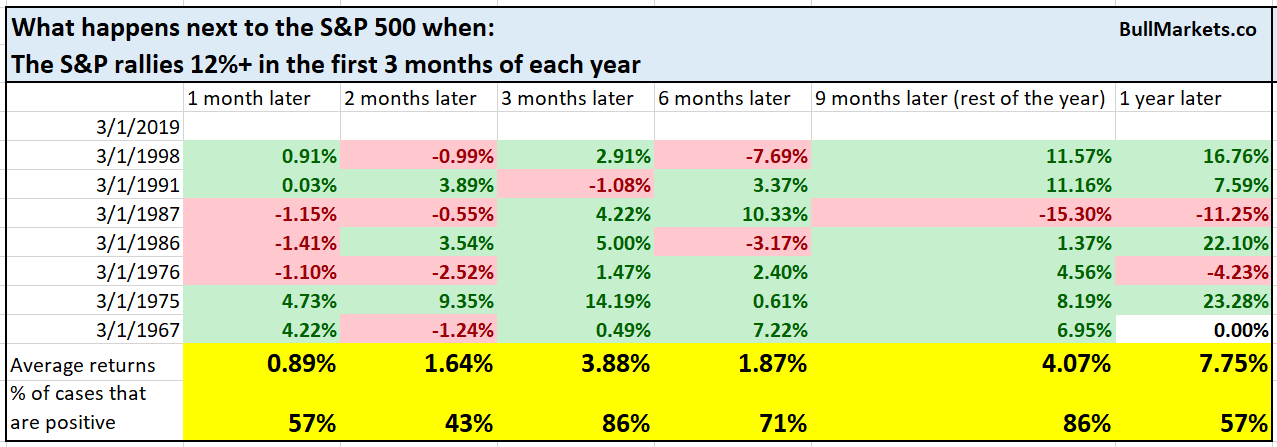

This has been one of the strongest starts to the year, with the S&P up more than 13% from January-March 2019. Similar rallies usually saw the S&P push higher throughout the rest of the year.

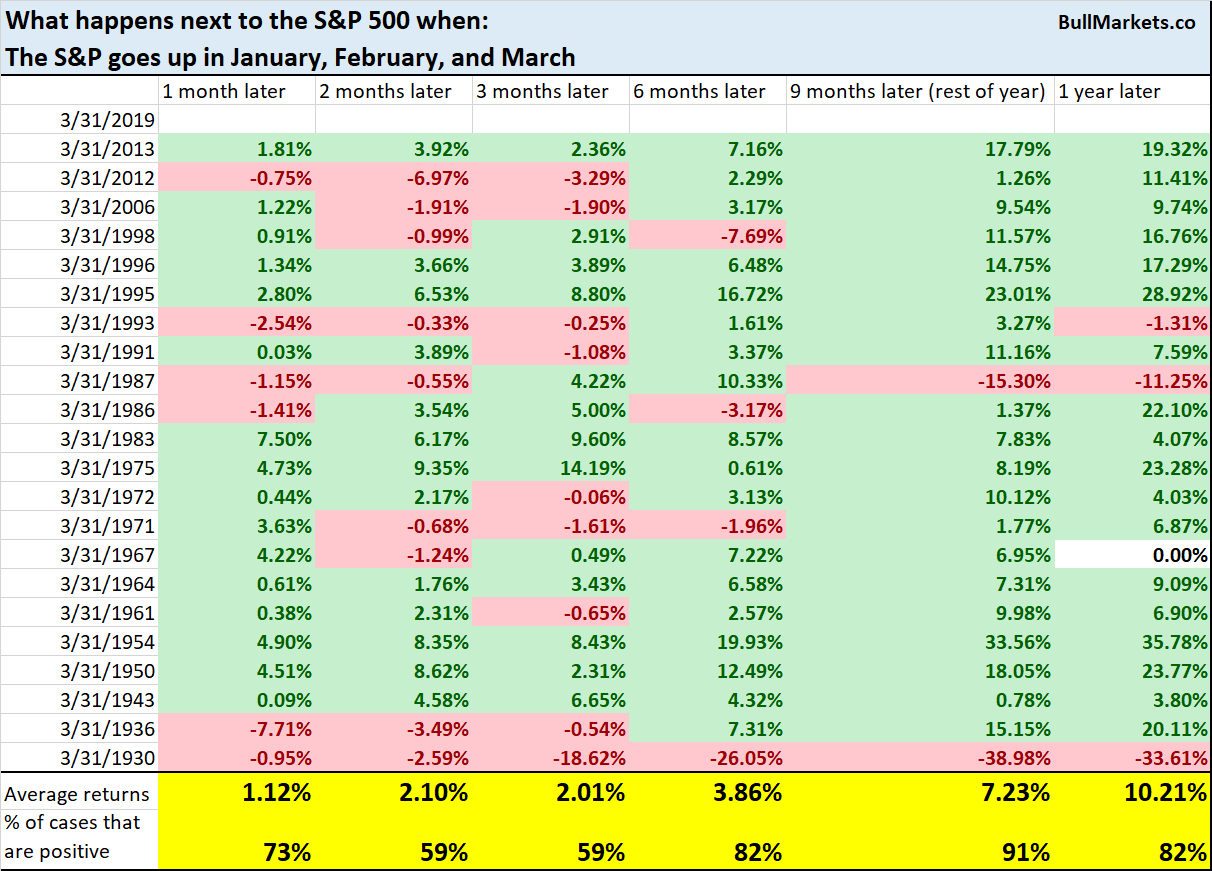

The S&P has gone up in January, February, and March. Likewise, this is quite bullish for the stock market throughout the rest of 2019.

April is the stock market’s most seasonally bullish month. Becareful with seasonality: it is of tertiary importance.

USD

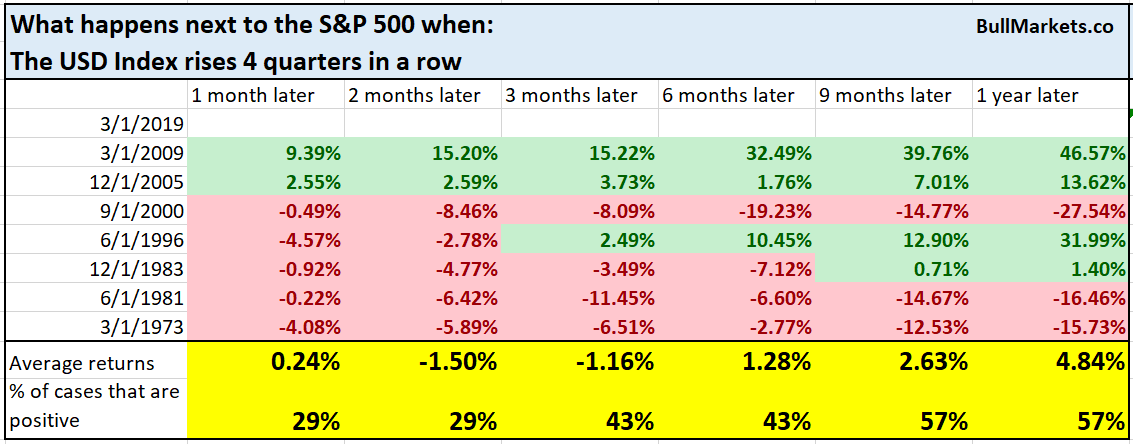

The USD Index has been rising over the past year, and is now up 4 quarters in a row.

This does appear to be a short term headwind for the S&P.

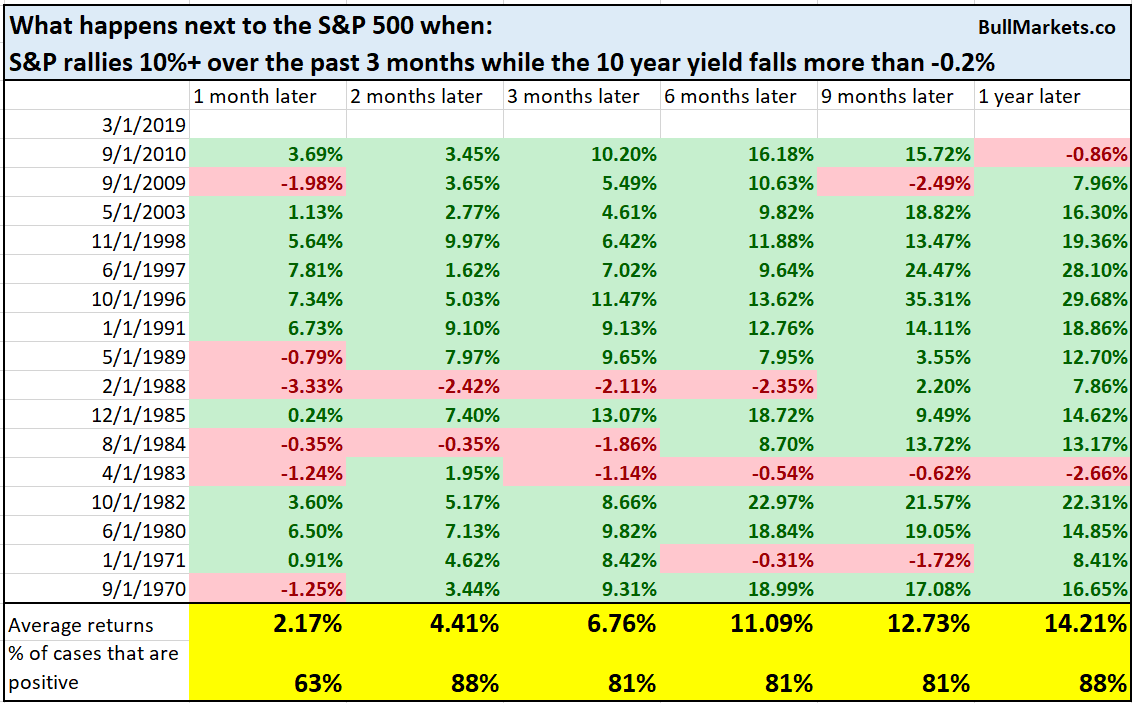

Treasury Bonds

While the S&P 500 rallied over the past 3 months, Treasury yields have fallen. The popular story in the media is that “this is bad for stocks”, because the bond market is smarter than the stock market. (Stocks decoupling from yields!)

This is actually more bullish than bearish for stocks.

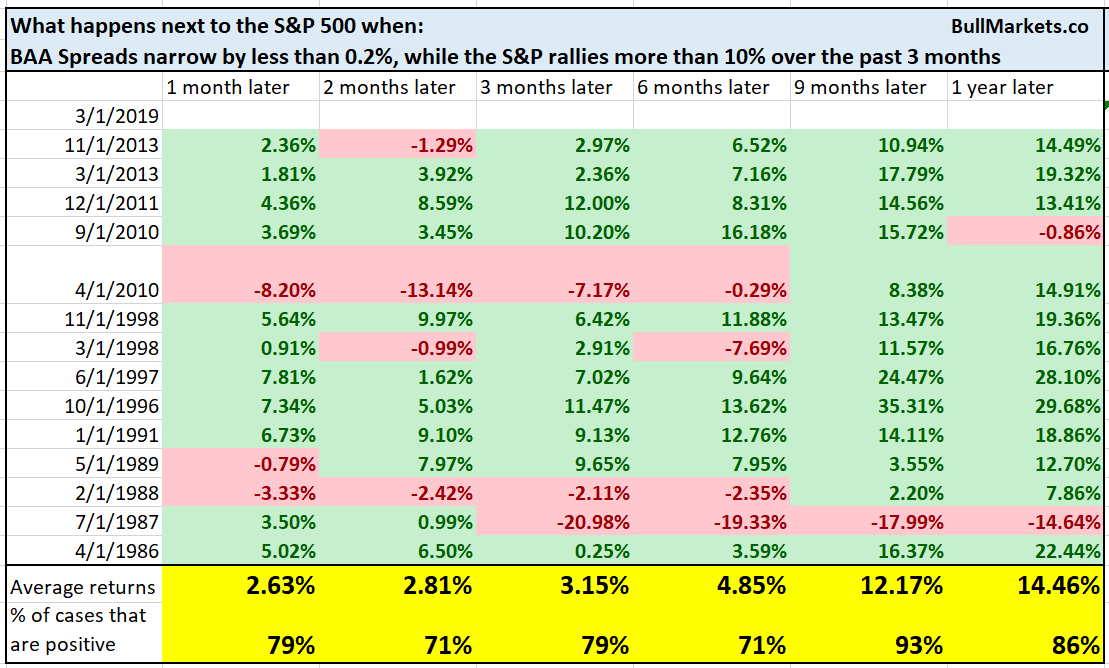

Bond spreads

While the S&P 500 is rallying, corporate bond spreads are not shrinking significantly.

While this may seem bearish, it’s not. This happens quite often, and is not ominous for stocks.

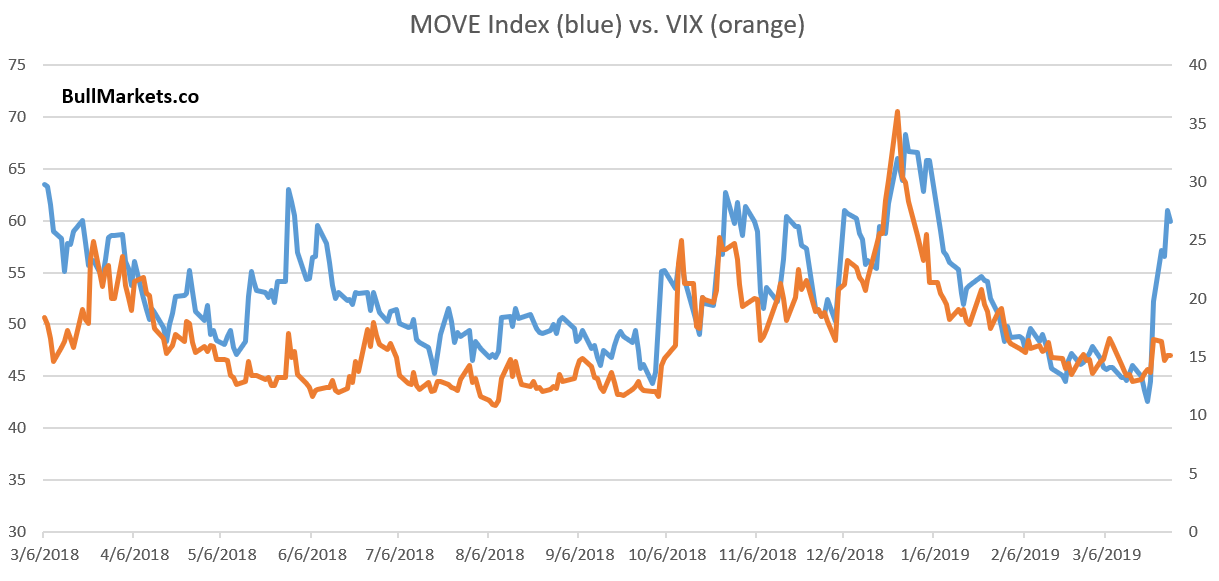

Volatility

The stock market has “diverged” from the bond market in many ways. For example, bond market volatility spiked while stock market volatility remains low.

Here’s the MOVE Index (bond market volatility) vs VIX (stock market volatility) as of Thursday.

Such a divergence between MOVE and VIX is rare. The only other time a divergence of this magnitude happened from 1990-present was June 2007. N=1, so worth watching.

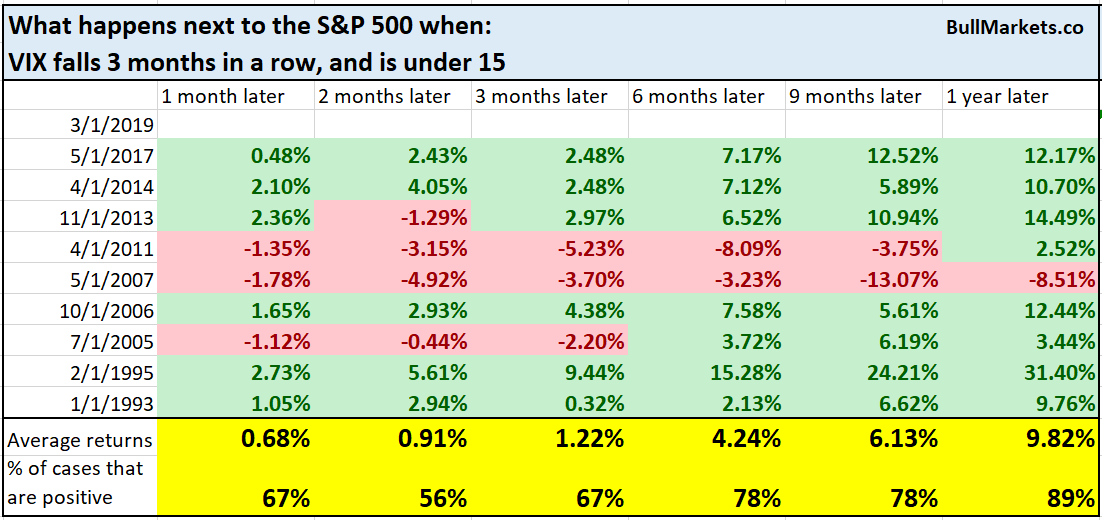

VIX has fallen 3 months in a row.

This is more bullish than bearish for stocks over the next year

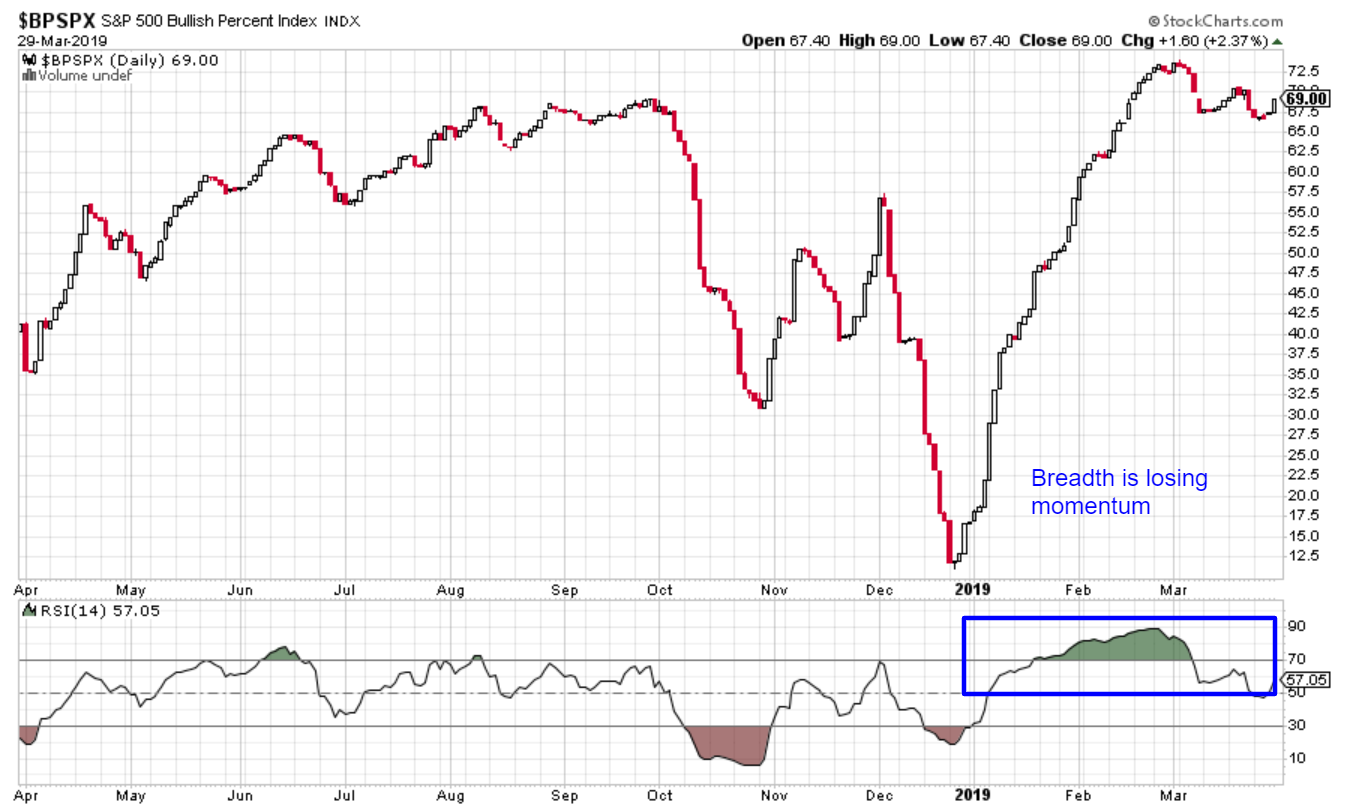

Breadth

Breadth is now weakening. The S&P 500 Bullish Percent Index’s (a breadth indicator) 14 day RSI fell below 50 for the first time in a long time this Monday.

Here’s what happens next to the S&P when the S&P 500 Bullish Percent Index’s 14 day RSI falls below 50 for the first time in 50 days.

You can see that the stock market’s 6-12 month forward returns are more bullish than random.

Price action

The S&P 500 will make a “golden cross” on Monday, with its 50 dma rising above its 200 dma.

In the S&P 500’s big historical bear markets, golden crosses always happened AFTER bear markets ended (i.e. golden crosses did not happen within bear markets). This is true of the following bear markets:

- 2007-2009

- 2000-2002

- 1973-1974

- 1969-1970

- 1937-1942

- 1929-1932

This technical factor suggests that the current rally is not a bear market rally, but a rally within a bull market.

*Do not take price action at face value. Price action changes over the decades. What was bullish price action in the past might not be bullish price action today.

Sectors

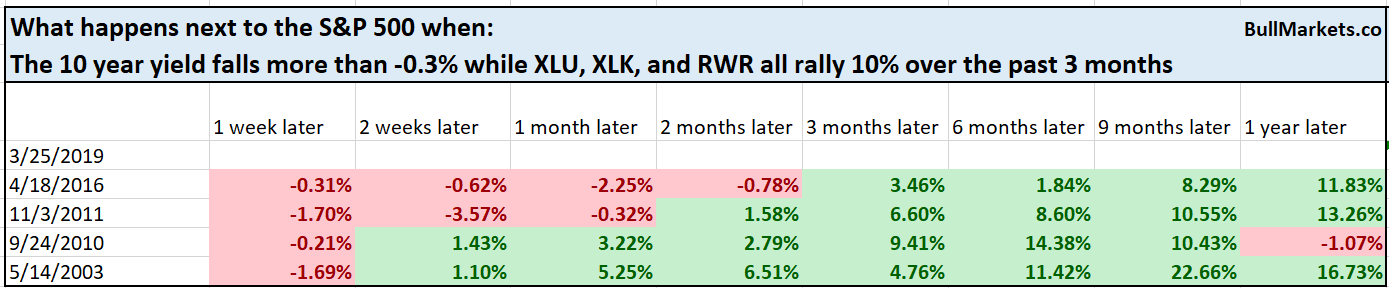

The recent stock market rally has been quite strong, with XLU (defensive stocks, XLK (high flying tech stocks), and RWR (real estate sector) all performing well.

This is remarkably different from the 2000-2002 and 2007-2009 bear market rallies. The 2000-2002 bear market saw incessant weakness in XLK (tech bust) and the 2007-2009 bear market saw incessant weakness in RWR (real estate bust).

Here’s what happens next to the S&P 500 when the 10 year yield falls while XLU, XLK, and RWR all rally 10% over the past 3 months. Sample size is small (n=4), but this is more bullish than bearish.

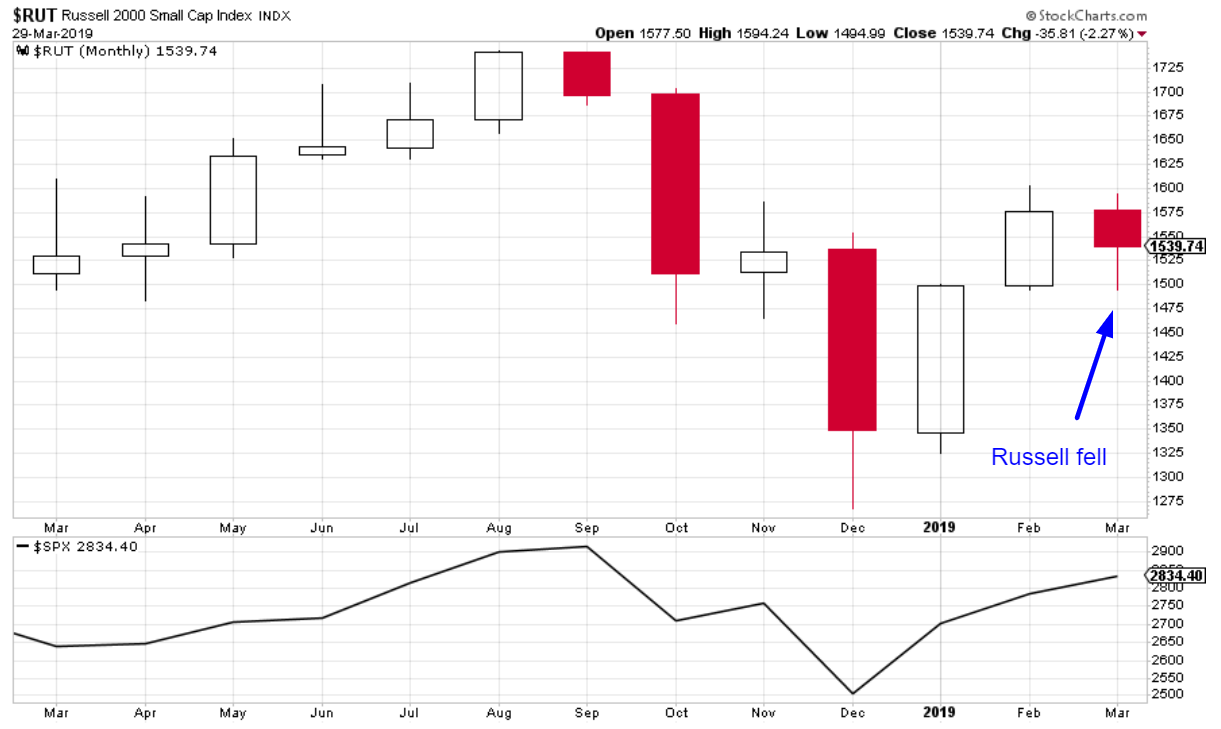

While the S&P rallied in March, the Russell 2000 fell.

This is quite rare. This kind of divergence between the S&P and Russell has only happened 2 other times from 1988-present.

*N=2, so I wouldn’t treat this as a “it’s the dot-com bubble all over again!” signConclusion

Here is our discretionary market outlook:

- The U.S. stock market’s long term risk:reward is no longer bullish. In a most optimistic scenario, the bull market probably has 1 year left. Long term risk:reward is more important than trying to predict exact tops and bottoms.

- The medium term direction (e.g. next 6-9 months) is mostly mixed, although there is a bullish lean.

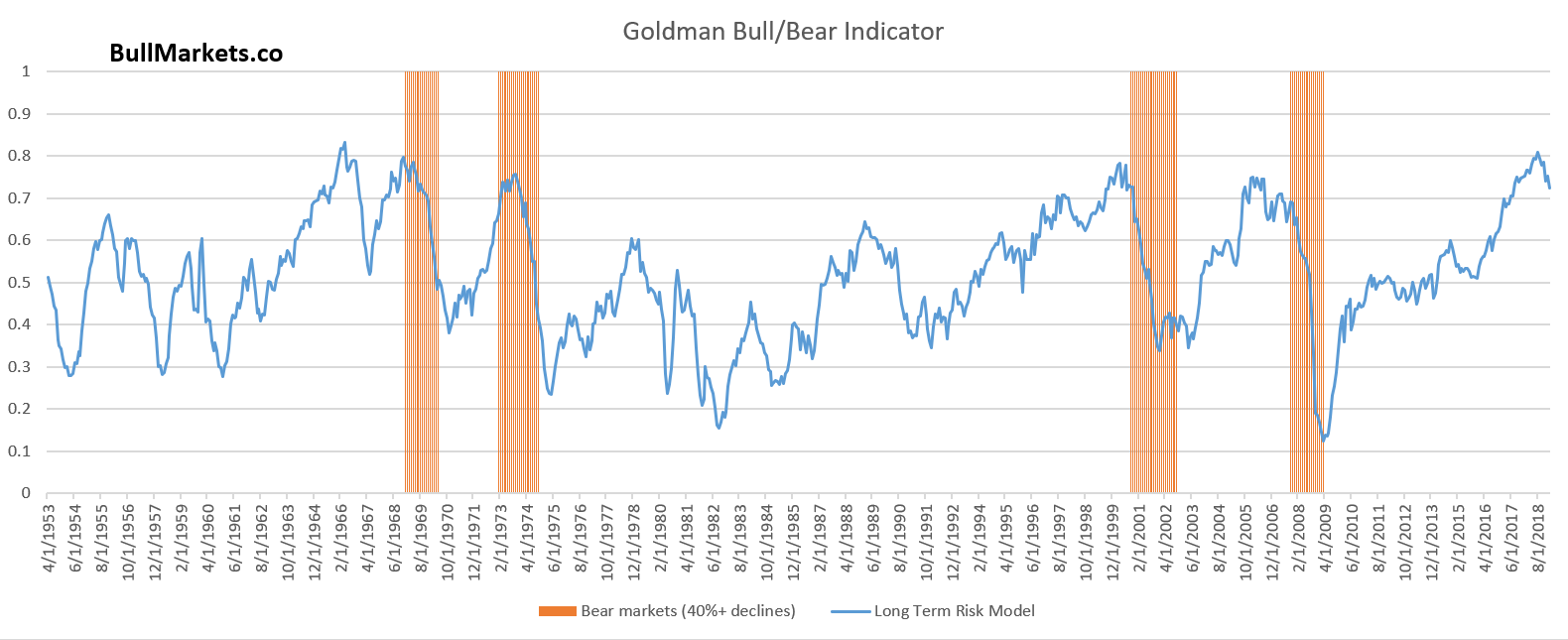

Goldman Sachs’ Bull/Bear Indicator demonstrates that risk:reward does favor long term bears.