Amid a struggling athletic wear market, Lululemon Athletica Inc. (NASDAQ:LULU) surprised investors with robust second-quarter fiscal 2017 results. Both sales and earnings topped estimates and improved year over year. While the bottom line marked its second consecutive beat, the top line recorded its seventh straight quarter of positive surprise.

Results were driven by consumers’ favorable response to Lululemon’s product innovations, solid direct-to-consumer (DTC) sales, focus on supply chain initiatives and the company’s commitment to its long-term strategy. Also, the company is on track with the remodeling of its iviva business into an online brand, as announced in June.

The solid second quarter progress makes management confident of generating revenues of $4 billion by 2020. These factors encouraged Lululemon to raise its fiscal 2017 outlook, which was welcomed by investors who were disheartened by the dismal numbers and drab views of sportswear big-wigs like The Finish Line Inc. (NASDAQ:FINL) , DICK’S Sporting Goods Inc. (NYSE:DKS) and Hibbett Sports Inc. (NASDAQ:HIBB) among others.

Evidently, this Zacks Rank #3 (Hold) stock jumped nearly 6% in the after-hours trading session on Aug 31, following the splendid results and outlook. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.Further, the company’s shares have witnessed a 7.4% rise over the last three months, surpassing the industry’s 5.5% growth.

e-Commerce Drives Q2 Numbers

Lululemon posted adjusted earnings of 39 cents per share that came ahead of the Zacks Consensus Estimate of 35 cents and rose 2.6% year over year. Also, the bottom line matched the upper end of the company’s guidance range of 33-35 cents per share. Including the effect of iviva’s restructuring, earnings came in at 36 cents per share.

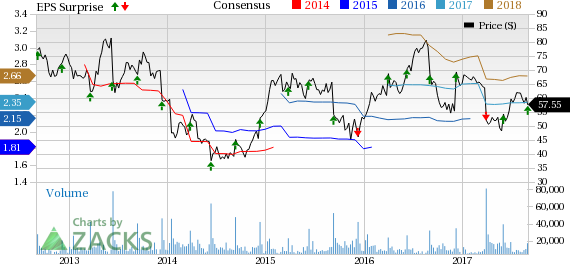

lululemon athletica inc. Price, Consensus and EPS Surprise

lululemon athletica inc. Price, Consensus and EPS Surprise | lululemon athletica inc. Quote

Looking at the top line, the Vancouver, Canada-based company’s quarterly revenues advanced about 13% to $581.1 million, surpassing the Zacks Consensus Estimate of $567.8 million. On a constant dollar basis too, revenue increased 13%. The improvement can be attributed to new store openings, as well as strong e-Commerce sales. Product-wise, the company’s men’s category was the outperformer, making management hopeful of generating revenues over $1 billion in this category, by 2020.

Total comparable store sales (comps), including in-store comps and direct-to-consumer sales, grew by 7% on both reported and constant-dollar basis. In-store comps were up 2% (on a constant dollar basis as well), while DTC sales surged 29% year over year. On constant-dollar basis, DTC sales increased 30%. Excluding the impact of the sale of an online warehouse, which occurred in the second quarter, DTC sales jumped 15% (up 16% on a constant dollar basis).

Margins

Adjusted gross profit rose 18% to $299.7 million in second-quarter fiscal 2017. Moreover, adjusted gross margin expanded 220 basis points (bps) to 51.6%, exceeding management’s expectations. The gross margin was fueled by 260 bps improvement in product margins backed by favorable mix and reduced costs, somewhat negated by increased markdowns stemming from the online warehouse sale.

Adjusted operating income increased marginally to nearly $74.1 million, while the operating margin contracted 160 bps to 12.8%. This could be accountable to the costs related to e-Commerce development.

Store Updates

During the quarter under review, the company opened 11 new stores and closed one. As of the end of second-quarter fiscal 2017, the company operated a total of 421 stores.

For fiscal 2017, the company targets opening 47 company-operated stores, with about 15 expected to be opened in international locations. In the third quarter, the company plans to open about 14 new stores.

Financials

Lululemon exited the quarter with cash and cash equivalents of $721.2 million and stockholders' equity of $1,397.8 million. Inventories were up 14%, at $316.4 million.

In first-half fiscal 2017, Lululemon generated about $102 million as cash flow from operating activities. Further, the company spent $30 million as capital expenditure in the second quarter of fiscal 2017.

In the quarter, the company bought back 1.5 million shares at an average price of $52.93 per share.

ivivva Strategy on Track

In June, Lululemon announced plans to develop iviva, its activewear brand, into an e-Commerce focused business, with only eight iviva stores operating across North America. The company revealed plans to close about 40 of the total 55 iviva stores and convert nearly half of the remaining stores into lululemon branded stores. The company is also on track to shut down 16 iviva showrooms and other temporary stores, in order to streamline corporate infrastructure. These closures are expected to be concluded by the end of third-quarter fiscal 2017.

In the first half of fiscal 2017, Lululemon recognized pre-tax charges of $23.2 million with regard to its iviva restructuring plan. Including these charges, the company still anticipates recording pre-tax costs of about $50-$60 million in fiscal 2017. These charges are mainly associated with long-lived asset impairment and lease termination expenses.

The Road Ahead

Lululemon remains on track with its efforts to build upon its supply chain network and e-Commerce business. Incidentally, the company’s supply chain initiatives have fueled its product margins over the past year. With regard to e-Commerce, the company targets updating its website with advanced features in the third quarter. This is likely to boost Lululemon’s holiday period performance. All said, the company provided a fresh third-quarter view, alongside increasing its outlook for fiscal 2017. Notably, the company’s guidance for the third quarter and fiscal 2017 excludes any impact from the iviva restructuring.

Q3 Forecasts

For third-quarter fiscal 2017, Lululemon anticipates revenues in the range of $605-$615 million, with constant dollar comps expected to increase in mid-single digits. The company expects normalized gross margin to remain in line with the year-ago period level. Management anticipates SG&A expense deleverage of about 50 bps. This is mainly related to the ongoing endeavors being undertaken to expand e-Commerce business.

Lululemon envisions normalized earnings (excluding the impact from iviva’s restructuring) for the third quarter to lie in a band of 50-52 cents per share. The current Zacks Consensus Estimate is pegged at 52 cents.

Raised FY17 View May Boost Estimates

For fiscal 2017, Lululemon projects sales to range from $2.545-$2.595 billion, up from the previous forecast of $2.53–$2.58 billion. The guidance is based on low-single digits comps growth on a constant dollar basis. This growth reflects the planned closure of iviva stores and the related reduction in revenues, offset by the strengthening of the e-Commerce business.

The company expects normalized gross margin expansion of 100 bps year over year in fiscal 2017, up from the old forecast of 50-100 bps increase. This will be backed by product margin enhancements, partly offset by higher product and supply chain costs as well as increase in occupancy and depreciation expenses.

Further, the company still anticipates SG&A expense to deleverage 50-100 bps driven by one-time digital investments, technological investments and costs related to global expansion. The company further stated that it expects SG&A rate to moderate in the third quarter, and improve in the final quarter. Normalized earnings for the fiscal year are now projected in a band of $2.35-$2.42 per share, up from the previous range of $2.28-$2.38. The current Zacks Consensus Estimate is pegged at $2.35, which is likely to witness upward revisions following the heartening projection.

Capital expenditures for fiscal 2017 are estimated in the range of $175-$180 million. Capital expenditures mainly include new store openings, renovation, relocation capital along with strategic IT and supply chain capital investments.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

lululemon athletica inc. (LULU): Free Stock Analysis Report

The Finish Line, Inc. (FINL): Free Stock Analysis Report

Dick's Sporting Goods Inc (DKS): Free Stock Analysis Report

Hibbett Sports, Inc. (HIBB): Free Stock Analysis Report

Original post

Zacks Investment Research