Value investing is easily one of the most popular ways to find great stocks in any market environment. After all, who wouldn’t want to find stocks that are either flying under the radar and are compelling buys, or offer up tantalizing discounts when compared to fair value?

One way to find these companies is by looking at several key metrics and financial ratios, many of which are crucial in the value stock selection process. Let’s put Tate & Lyle (LON:TATE) PLC (OTC:TATYY) stock into this equation and find out if it is a good choice for value-oriented investors right now, or if investors subscribing to this methodology should look elsewhere for top picks:

PE Ratio

A key metric that value investors always look at is the Price to Earnings Ratio, or PE for short. This shows us how much investors are willing to pay for each dollar of earnings in a given stock, and is easily one of the most popular financial ratios in the world. The best use of the PE ratio is to compare the stock’s current PE ratio with: a) where this ratio has been in the past; b) how it compares to the average for the industry/sector; and c) how it compares to the market as a whole.

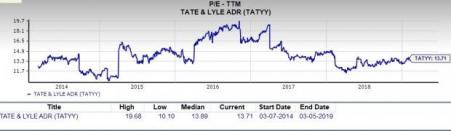

On this front, Tate & Lyle has a trailing twelve months PE ratio of 13.7, as you can see in the chart below:

This level actually compares pretty favorably with the market at large, as the PE for the S&P 500 stands at about 17.7x. If we focus on the long-term PE trend, Tate & Lyle’s current PE level puts it slightly below its midpoint of 13.9 over the past five years. Moreover, the current level is fairly below the highs for this stock, suggesting it might be a good entry point.

Further, the stock’s PE also compares favorably with the Zacks Consumer Staples sector's trailing twelve months PE ratio, which stands at 18.4. At the very least, this indicates that the stock is relatively undervalued right now, compared to its peers.

We should also point out that Tate & Lyle has a forward PE ratio (price relative to this year’s earnings) of just 14.4, so it is fair to say that a slightly more value-oriented path may be ahead for Tate & Lyle stock in the near term too.

P/S Ratio

Another key metric to note is the Price/Sales ratio. This approach compares a given stock’s price to its total sales, where a lower reading is generally considered better. Some people like this metric more than other value-focused ones because it looks at sales, something that is far harder to manipulate with accounting tricks than earnings.

Right now, Tate & Lyle has a P/S ratio of about 1.2. This is significantly lower than the S&P 500 average, which comes in at 3.2x right now. Also, as we can see in the chart below, this is well below the highs for this stock in particular over the past few years.

Broad Value Outlook

In aggregate, Tate & Lyle currently has a Value Score of B, putting it into the top 40% of all stocks we cover from this look. This makes Tate & Lyle a solid choice for value investors, and some of its other key metrics make this pretty clear too.

For example, the P/CF ratio (another great indicator of value) comes in at 8.61, which is far better than the industry average of 11.4. Clearly, Tate & Lyle is a solid choice on the value front from multiple angles.

What About the Stock Overall?

Though Tate & Lyle might be a good choice for value investors, there are plenty of other factors to consider before investing in this name. In particular, it is worth noting that the company has a Growth Score of A and a Momentum Score of A. This gives TATYY a Zacks VGM score — or its overarching fundamental grade — of A. (You can read more about the Zacks Style Scores here >>)

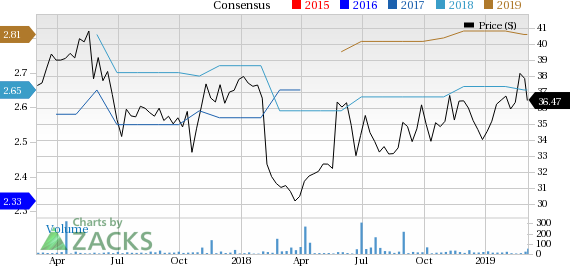

Meanwhile, the company’s recent earnings estimates have been slightly disappointing. We note that the full year estimate has seen one downward revision and no upward revisions in the past 60 days.

This has had just a small impact on the consensus estimate as the full year estimate has inched down by a penny in the past two months. You can see the consensus estimate trend and recent price action for the stock in the chart below:

Owing to this somewhat bearish trend, the stock has just a Zacks Rank #3 (Hold), which is why we are looking for in-line performance from the company in the near term.

Bottom Line

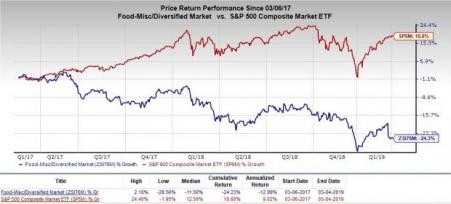

Tate & Lyle is an inspired choice for value investors, as it is hard to beat its incredible lineup of statistics on this front. However, with a sluggish industry rank (bottom 41% out of more than 250 Zacks industries) and a Zacks Rank #3, it is hard to get too excited about this company overall. In fact, over the past two years, the Zacks Food-Misc/Diversified industry has clearly underperformed the broader market, as you can see below:

So, value investors might want to wait for estimates and analyst sentiment to turn around in this name first, but once that happens, this stock could be a compelling pick.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Tate & Lyle PLC (TATYY): Free Stock Analysis Report

Original post

Zacks Investment Research