Gold prices surged to an all-time high of $2,940 per ounce last Thursday, pushing its market cap above $20 trillion for the first time ever, as trade tensions between the U.S. and Europe have stoked fears of a global economic slowdown. And while safe-haven demand is certainly a driver, there’s another potential catalyst that could send prices soaring even higher: the revaluation of America’s gold reserves.

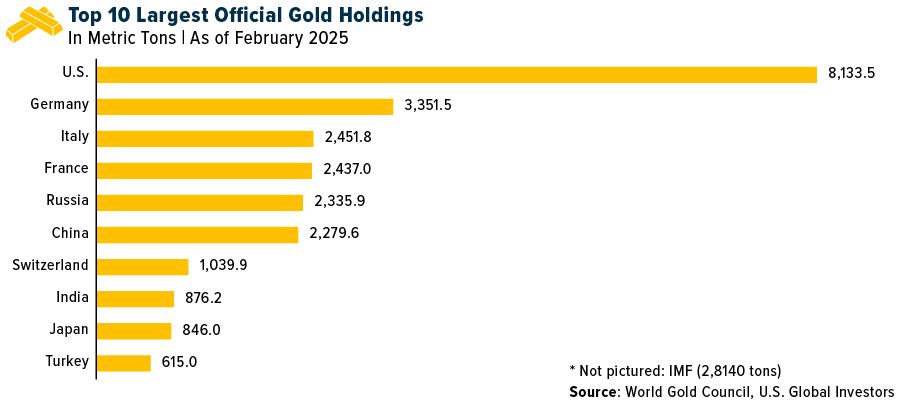

As many of you are aware, the U.S. holds the most gold of any country on earth by far, with reserves totaling 8,133 metric tons. But what’s less well-known is that the stockpile’s value has remained at just $42 per ounce since 1973, putting its total value at around $11 billion.

Let’s say we were to revalue those reserves at today’s price of around $2,900, which some people are in favor of. The total value, then, would jump to a staggering $760 billion, creating a windfall of $749 billion.

This could provide the government with options to sell a portion of its gold or enhance its balance sheet by reducing debt. It could even be used to fund a Sovereign Wealth Fund (SWF), which I wrote about earlier in the month.

Treasury Secretary Scott Bessent has tried to tamp down speculation that the U.S. will go through with this process, stating that it’s “not what [he] had in mind,” but I believe the fact that we’re having this discussion highlights gold’s importance as a financial asset and geopolitical tool.

Verifying the Gold at Fort Knox

Before any revaluation can occur, though, it’s probably best to verify that the gold reserves actually exist—a concern that’s lingered for decades.

The U.S. Bullion Depository at Fort Knox, which houses the bulk of the nation’s gold, has only opened its doors to non-authorized personnel three times in history: 1) in 1943 for President Franklin D. Roosevelt, 2) in 1974 for a small group of Congress members and 3) in 2017 for a delegation including Senator Mitch McConnell and then-Treasury Secretary Steven Mnuchin.

Elon Musk has announced plans to conduct an in-person audit of Fort Knox’s gold reserves on behalf of his cost-cutting operation, the Department of Government Efficiency, or DOGE. In a tweet on February 17, Musk wrote, “Who is confirming that gold wasn’t stolen from Fort Knox?… We want to know if it’s still there.”

Who is confirming that gold wasn’t stolen from Fort Knox?

— Elon Musk (@elonmusk) https://twitter.com/elonmusk/status/1891555910218097122?ref_src=twsrc%5Etfw">February 17, 2025

Maybe it’s there, maybe it’s not.

That gold is owned by the American public! We want to know if it’s still there. https://t.co/aEBXK1CfD6">https://t.co/aEBXK1CfD6

I don’t doubt that the gold’s where it should be, but I fully support Musk and President Trump’s efforts to provide transparency. If the audit confirms the reserves—which I believe it will—it could boost confidence in the U.S. government’s finances. Conversely, if discrepancies are found, it could send shockwaves through global markets, adding further momentum to gold prices.

Central Bank Buying and Global Market Trends

Central banks have been on a gold buying spree, having snapped up over 1,000 tons of the metal for the third consecutive year in 2024, according to the World Gold Council (WGC). The National Bank of Poland (NBP) led the pack, adding 90 tons to its reserves, while the People’s Bank of China (PBoC) announced a fresh purchase of 5 tons to start 2025, bringing its total holdings to 2,285 tons.

Central banks are often considered the “smart money” in the gold market, and their sustained accumulation of gold reflects a broader strategy to diversify reserves and hedge against their very own policies. What’s more, this buying activity supports prices, creating a favorable backdrop for gold as an investment.

Peak Gold Ahead?

On the supply side, total gold production rose to a record 4,974 tons in 2024, driven by increased mine output and recycling. Initial estimates suggest mine production reached an all-time high of 3,661 tons, though final figures could revise this record. However, the long-term supply outlook is less rosy.

According to S&P Global’s Paul Manalo, the gold supply is expected to peak in 2026 before declining as a result of fewer new discoveries. Exploration budgets, which surged to $7 billion in 2022, have cooled off but remain higher than historical averages. This trend could support higher gold prices over the medium to long term, particularly if demand from central banks and investors remains robust.

Positioned for Growth

The high gold price environment has allowed gold mining companies to expand operations, prioritize sustainability initiatives and attract investor interest. Bank of America estimates that companies under its coverage could generate around $3 billion in free cash flow (FCF) in the fourth quarter of 2024, with even more expected this year.

However, rising costs present a challenge. The average All-In Sustaining Cost (AISC) for gold miners hit a record $1,456 per ounce in the third quarter of 2024, driven by higher labor costs and maintenance expenses.

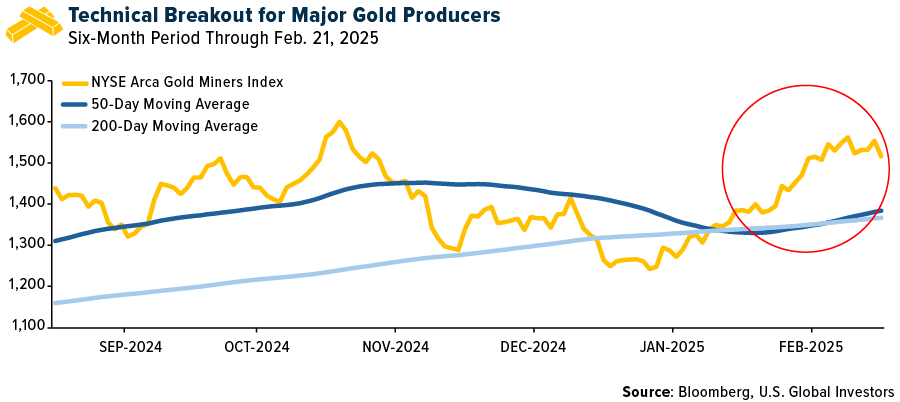

Despite these pressures, many miners remain highly undervalued, making them attractive to value investors. The NYSE Arca Gold Miners Index, which tracks major gold producers, recently made a technical breakout, with the 50-day moving average crossing above the 200-day moving average.

Strategic Takeaways

So what does all this mean for your portfolio?

Gold remains a vital asset for diversification. I believe its role as a hedge against inflation, currency devaluation and geopolitical risks is as relevant today as ever for long-term investors.

For more tactical investors, the potential revaluation of U.S. gold reserves—or even the publicity surrounding Musk’s proposed audit—could act as a catalyst for price movements.

Meanwhile, the continued buying by central banks and supply constraints in the mining sector offer additional support for a bullish outlook on gold.

As always, I recommend a 10% weighting in gold, with 5% in physical gold (coins, bars, jewelry) and 5% in high-quality gold mining stocks, mutual funds, and ETFs.

The NYSE Arca Gold Miners Index is a stock market index that measures the performance of companies that mine gold and silver. It’s a modified market capitalization-weighted index that includes companies from around the world.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate for every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Which stock should you buy in your very next trade?

With valuations skyrocketing in 2024, many investors are uneasy putting more money into stocks. Unsure where to invest next? Get access to our proven portfolios and discover high-potential opportunities.

In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. That's an impressive track record.

With portfolios tailored for Dow stocks, S&P stocks, Tech stocks, and Mid Cap stocks, you can explore various wealth-building strategies.