More positive US data today as US Retail Sales came in better than expected. The one-day FOMC meeting today may be short on new developments, but the market may react nonetheless.

EUR/USD: the rare earth angle?

Some are suggesting that today’s EURUSD sell-off was aggravated by the EU joining the US and Japan in officially protesting to the WTO on China’s rare earth element policy, as China recently decided to strictly limit the export of those exotic metals, which are key in a number of high-tech industries (hybrid autos, cell phones, etc.). China contains the vast majority of the world’s supply of rare earth metals. One can suppose that the thinking here is that if the EU is willing to antagonize China on this issue, then China will be more reluctant to pour money into Europe’s sovereign debt black hole.

Regardless, the dye was somewhat cast already late last week, and this news item may have simply broad forward weakness that already looked to be in the pipeline. The pair managed to slice all the way through the 55-day moving average that supported yesterday around 1.3080 and 1.3000 is the next obvious area of support, below which EURUSD hasn’t closed since mid-January. The Euro even managed to weaken despite a strong new surge in the German ZEW survey, which has been screaming off the lows of late last year and managed to post its highest level since mid-2010. Normally, this index has proven a leader to the equity market, but this time around, it may be the tail that is wagging the dog.

UK terms of trade improvement

The UK trade balance number came in far better than expected, even if the deficit widened relative to December, and there now seems to be a structural turnaround under way in the UK terms of trade, a necessary development for the pound’s longer term prospects. Car and oil exports were the main factors contributing to the improving balance.

US data

More good economic data out of the US today, with Advance Retail Sales up +0.6% ex Autos and Gas for February, marginally better than expected, but also on top of a +0.4% boost to the January number (to +1.0% MoM). So despite very low growth in incomes and higher petrol prices, US consumers managed to spend more over the last couple of months, which is an impressive showing. Mild weather may be a factor in play here, but there is still some degree of momentum in the US economy.

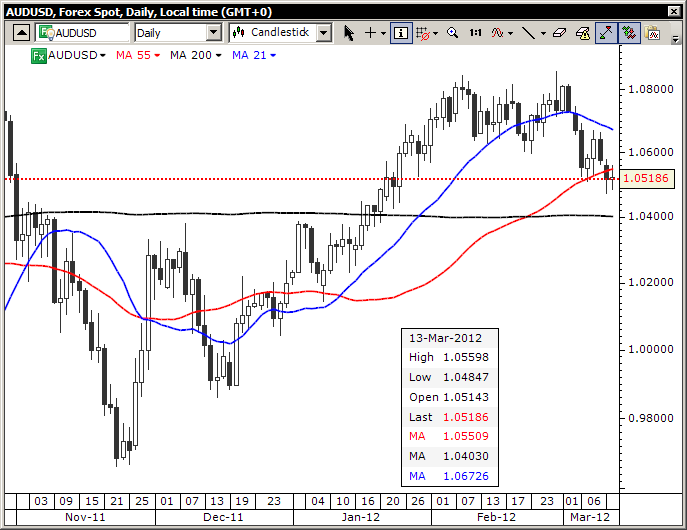

Chart: AUD/USD

AUD/USD has crossed below its 55-day moving average recently and tested that level as resistance today. Note the next key support is the 200-day moving average just above 1.0400. The chart looks nominally neutral in the big picture and still positive in the shorter term picture, but a dip through there and through 1.0350 would begin to tilt the bias to the downside. Note the key mining tax vote coming up for the Gillard government. AUD/USD" title="Chart: AUD/USD" width="687" height="530">

AUD/USD" title="Chart: AUD/USD" width="687" height="530">

Looking ahead – FOMC preview

The FOMC is up shortly. The general expectations after Bernanke’s less urgently dovish rhetoric of late is that the US is on hold for now, even if the Fed r. This is only a one-day meeting and will not feature a Bernanke press conference, so unless language in the statement changes dramatically, the market may take this meeting relatively in stride, though we’ve yet to see the “disappointment trade” that we though might develop once the market realized that the easy money won’t be coming for a while.

The most interesting market to watch in the wake of the FOMC meeting tonight – if it decides to move – will be the US treasury market, as the 10-year yield is pushing the envelope close to the 2.07-2.10% yield level that has amazingly contained it since last October. In the past, I would normally have stated that the JPY crosses are the most sensitive to the bond market moves, but now that USDJPY has already exploded higher, I’m not sure the volatility potential for the JPY crosses to the upside is as great unless treasuries see a large scale extension of their recent sell-off. As well, the JPY seems to be more focused on risk appetite lately as it has become the preferred carry trade funding currency together with the Euro, so the focus may be more on that front than on interest rates (remember that during the recent brief equity market swoon, the JPY outpaced the USD for a time). We should also remember that, despite today’s USDJPY rally to new highs for the cycle, the BoJ didn’t provide much new at its meeting.

Looking further ahead – tomorrow is eerily quiet save for the Norwegian deposit rate (note still ludicrous AUDNOK level near the 6.00 handle) and then Thursday we have the potential for more fireworks, with the SNB set for its quarterly meeting after EURCHF has gone dormant a scant few tens of pips above the declared 1.20 floor. We also have the US Mar. Empire and Philadelphia Fed manufacturing surveys out that day.

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes 6 winning stock portfolios chosen by our advanced AI. In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. Which stock will be the next to soar?

Unlock ProPicks AI