EU and US indices pulled back yesterday, perhaps due to end-of-month position adjustments, or because they turned careful as we get closer to Friday’s NFPs. Yesterday’ Eurozone’s inflation accelerated, but the euro barely reacted, as this is unlikely to alter the ECB’s plans, while today, traders of oil and oil-linked currencies are likely to pay attention to the OPEC+ gathering, where major producers will decide whether there is a need to add more supply now.

EU And US Traders Turn Careful Ahead Of The NFPs, OPEC+ Meets

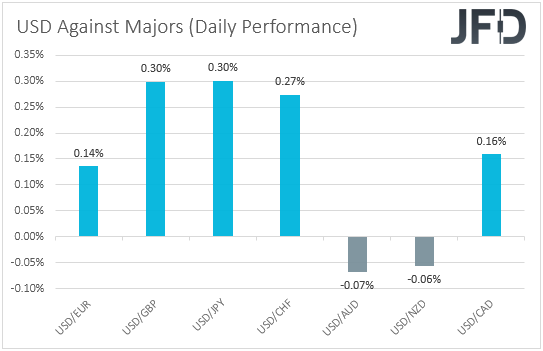

The US dollar traded higher against the majority of the other major currencies on Tuesday and during the Asian session Wednesday. It underperformed slightly only against AUD and NZD, while it gained the most ground against GBP, JPY, and CHF.

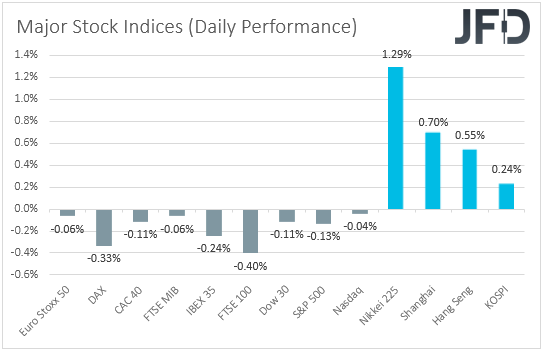

The weakening of the safe havens yen and franc, combined with the strengthening of the risk-linked Aussie and Kiwi, points to a risk-on trading environment. However, the strengthening of the greenback, and the weakening of the pound and the Loonie, point otherwise. Thus, in order to get a clearer picture with regards to the broader market sentiment, we prefer to turn our gaze to the equity world. There, major EU, and US indices traded slightly in the red, though sentiment improved during the Asian session today.

Maybe EU and US indices pulled back due to end-of-month position adjustments, or it could be what we said yesterday, that market participants may have started trading more carefully as we get closer to Friday’s NFPs. Market appetite returned during the Asian session today, perhaps due to the beginning of the new month in the continent. In any case, we stick to our guns that investors may head into the US jobs report with a relatively careful strategy, as they try to figure out the next policy moves of the Federal Reserve. As we noted yesterday, expectations are for another strong report, which may raise the volume of the hawkish voices among the FOMC, something that may result in a majority vote in favor of tapering sooner than Chair Powell thinks.

Yesterday, we had Eurozone’s preliminary CPIs for August, with both the headline and underlying inflation measures accelerating by more than expected. However, as we have been expecting, the euro did not receive a massive boost, as an underlying rate still decently below 2%, and the latest slide in the PMIs, were unlikely to allow a surging headline print to alter expectations around the ECB’s policy plans. So, we repeat that, with the ECB pledged to stay accommodative for long, we see the case for the euro to stay under pressure against currencies the central banks of which are expected to start normalizing their respective policies soon, the likes of the Kiwi and, conditional upon a strong NFP report on Friday, the US dollar.

As for today, traders of oil and oil-linked currencies, like the Loonie, are likely to pay attention to the OPEC+ gathering, where major producers will decide whether there is a need to add more supply now. The group agreed to add 400k bpd until the end of December, and market chatter suggests that they will stick to their guns, despite pressure for the US to pump more.

On Sunday, Hurricane Ida knocked at least 94% of offshore Gulf of Mexico oil and gas production and caused catastrophic damage to Louisiana’s grid. Although this could mean supply disruptions, analysts say that three-quarters of that output could be resumed by the end of the week. Thus, it seems that there are more concerns that power outages and flooding in Louisiana after the Hurricane will cut demand from refineries. All this is negative for oil prices, and perhaps OPEC and its allies may want to avoid any further declines by increasing output at the moment. So, we agree with the consensus, and we do believe that the cartel will stick to the existing plan. As for a market reaction, we could just see a relief bounce, as even the slim chance of output increase is dismissed.

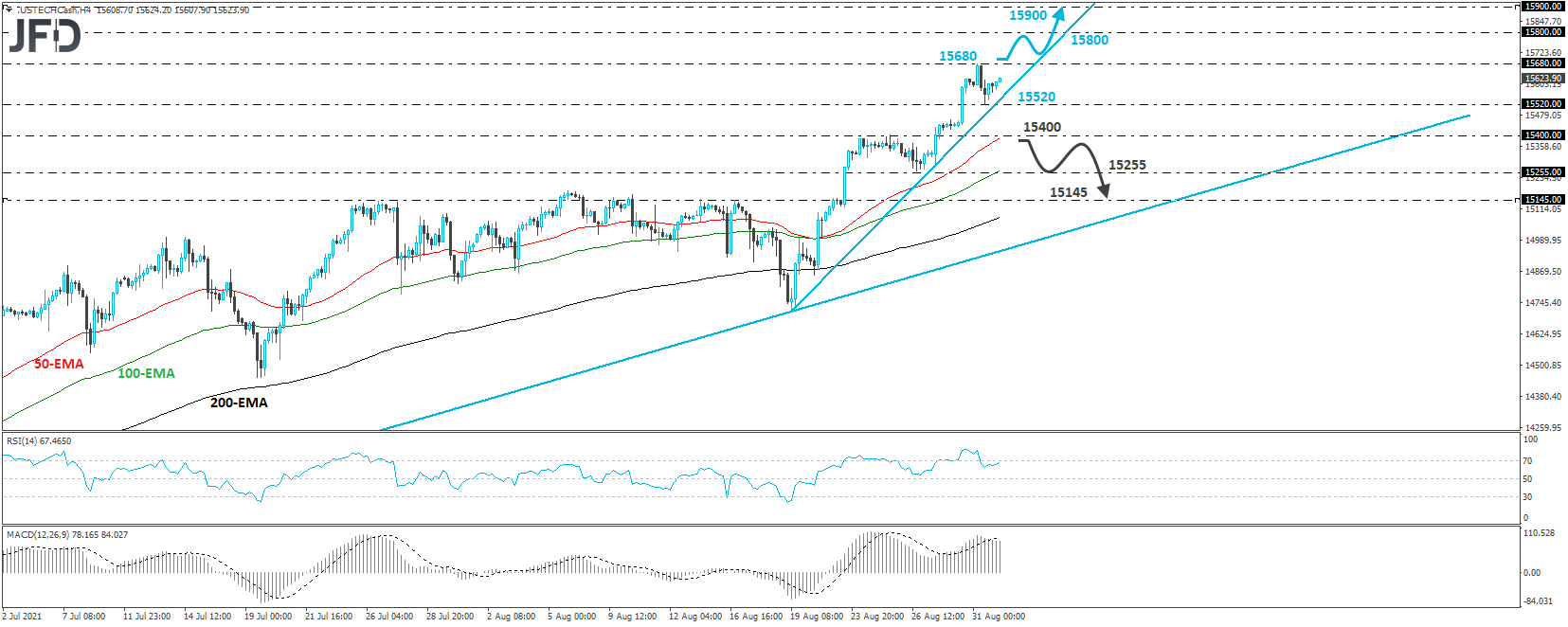

NASDAQ 100 Technical Outlook

The NASDAQ 100 cash index traded lower yesterday, after it hit a fresh record of 15680. Then, the index hit support at 15520, above the short-term upside support line drawn from the low of Aug. 19, and then it rebounded again. As long as it stays above that line, we would see decent chances for further advances and new records in the days to come.

A break above 15680 would place the index into the uncharted territory, and with no prior highs or inside swing lows to make upcoming resistance barriers, we will mark as one the round number of 15800. If that are doesn’t hold, we will aim for the next round figure of 15900.

In order to start examining the case of a deep correction, we would like to see a break below 15400, which is the inside swing high of Aug. 25. The index would already be below the aforementioned upside line and may see scope for declines towards the low of Aug. 26, at around 15255. Another break, below 15255, could extend the slide towards the inside swing high of Aug. 16, at 15145.

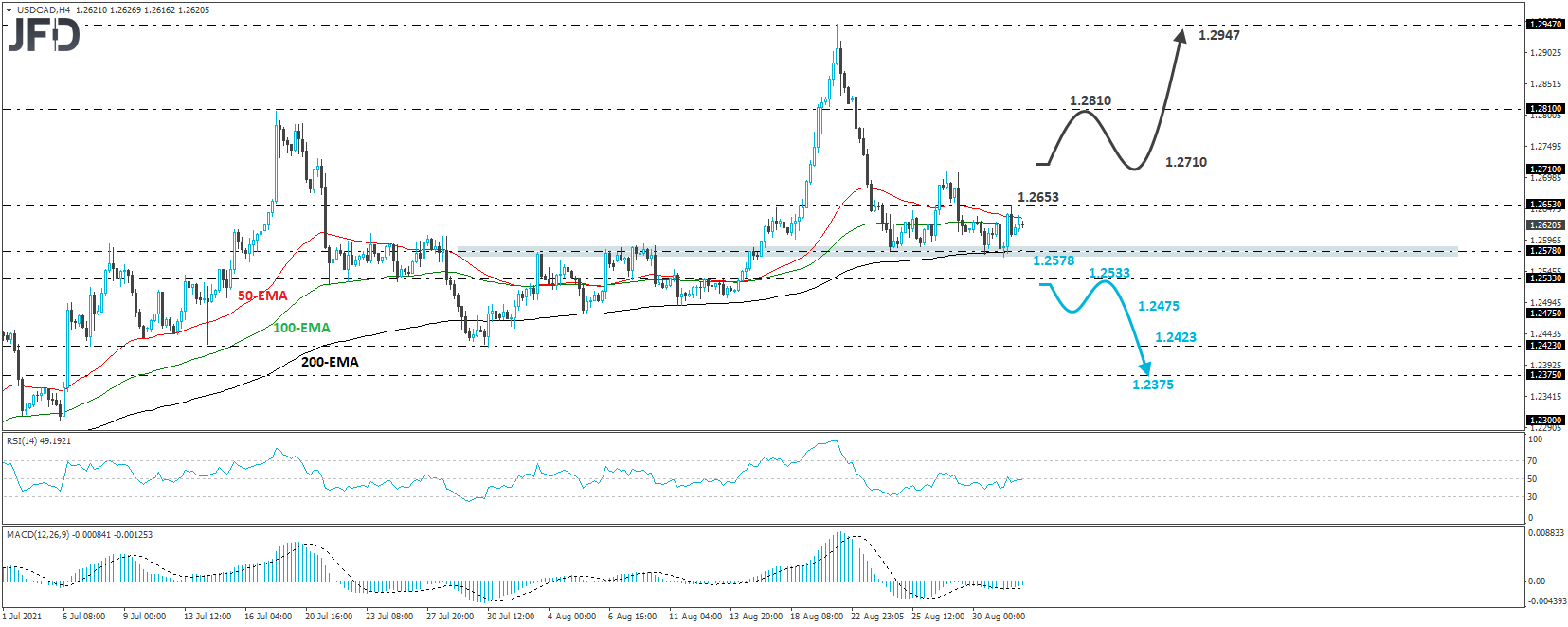

USD/CAD Technical Outlook

USD/CAD traded slightly higher after it hit once again the key support zone of 1.2578. That said, the recovery stayed limited near 1.2653. Lately, the pair has been trading in a consolidative manner, and thus, we will refrain from confidently calling its next trending direction.

In order to start examining the bearish case, we would like to see a dip below that key support. This will confirm a forthcoming lower low and may initially target the 1.2533 zone. Another break, below 1.2533, could invite more bears into the game, who may drive the action towards the low of Aug. 5, at 1.2475, or the low of July 30, at 1.2423.

On the upside, we would assess a bullish-case scenario, when we see a recovery above the high of Aug.27, at 1.2710. This could set the stage for upside extensions towards the high of July 19, at 1.2810, the break of which could extend the rally towards the peak of Aug. 20, at 1.2947.

As For The Rest Of Today's Events

Later in the day, the US ADP employment report for August is coming out and it is expected to have accelerated to 638k from 330k. Accelerating jobs growth in the private sector could raise some speculation that the NFPs, due out on Friday, may accelerate as well. However, we will not rely much on the ADP print, as it is far from a reliable predictor for the NFPs. Even last month, when the ADP number fell to 330k from 680k, the NFPs held more or less steady around 940k. The ISM manufacturing PMI for the month is also coming out and it is anticipated to have slid to 58.5 from 59.5.

As for the speakers, we have only one on today’s agenda and this is Atlanta Fed President Raphael Bostic.