The US dollar, and other safe havens gained yesterday and today in Asia, while Equities and risk-linked currencies tumbled, perhaps due to renewed concerns that the fast-spreading Delta variant of the coronavirus will hamper the global economic recovery.

With that in mind, will central-bank officials, especially at the Fed, start considering delaying any tightening plans? With inflation still well above their objective, the answer to that question is not straight forward.

Safe Havens Gain, Risk Assets Tumble

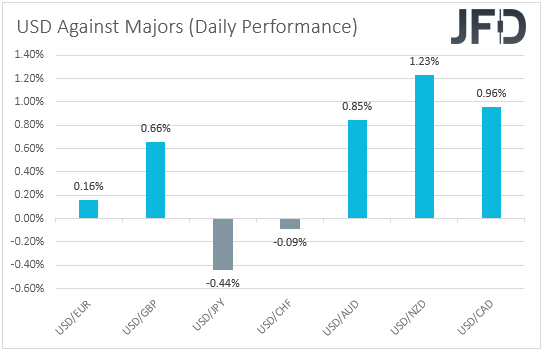

The US dollar continued trading north against most of the other major currencies on Monday and during the Asian session Tuesday. It underperformed only versus JPY and CHF, while it gained the most against NZD, CAD, and AUD.

The strengthening of the safe-harbors, yen, franc and greenback, combined with the weakening of the risk-linked aussie, kiwi and loonie, suggests that investors’ appetite continued to deteriorate.

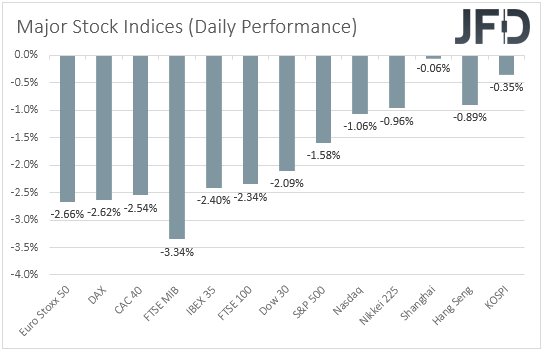

Indeed, looking at the performance in the equity world, we see that all major global indices were a sea or red, with the EU indices falling the most.

Actually, the average tumble in Europe was 2.65%, while later in the US, we saw Wall Street indices falling on average 1.58%. Appetite remained weak during the Asian session today as well.

With no clear catalyst to pinpoint for causing this turmoil, maybe this was the result of an overstretched market or maybe this happened due to increasing concerns that the fast-spreading Delta variant of the coronavirus will hamper the global economic recovery. Maybe it’s both.

The question coming now is: With fears over further spreading of the virus increasing, did expectations over monetary policy change? In other words, have investors started pushing back their hike bets due to those virus fears?

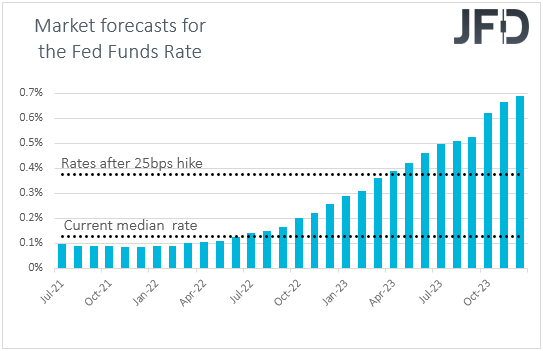

It seems that market participants’ view on monetary policy, at least with regards to the Fed, has not changed much. Looking at the yields of the 30-day Fed funds futures, we see that investors still anticipate the first rate increase to be delivered during the first quarter of 2023.

As for our view, another potential economic slowdown due to the virus, now combined with surging inflation, may be a big headache for policymakers. On the one hand, it will be difficult to keep planning hikes in case the economy is hurt again, while on the other, you cannot ignore inflation if it continues to skyrocket well above your objective.

For now, a cocktail of virus concerns and expectations of rate hikes in early 2023 may keep investors morale dented. In that respect, one of the currency pairs that could feel the repercussions of those concerns and bets the most is AUD/USD. Aussie tends to weaken and the dollar to strengthen when market sentiment deteriorates.

What’s more, monetary policy divergence could also add weigh on this exchange rate. Remember that the RBA stayed in its dovish dress, with policymakers saying that interest rates in Australia are likely to stay at present levels at least until 2024, at a time when the Fed has already signaled 2 hikes in 2023, and started discussing when to start scaling back its QE purchases.

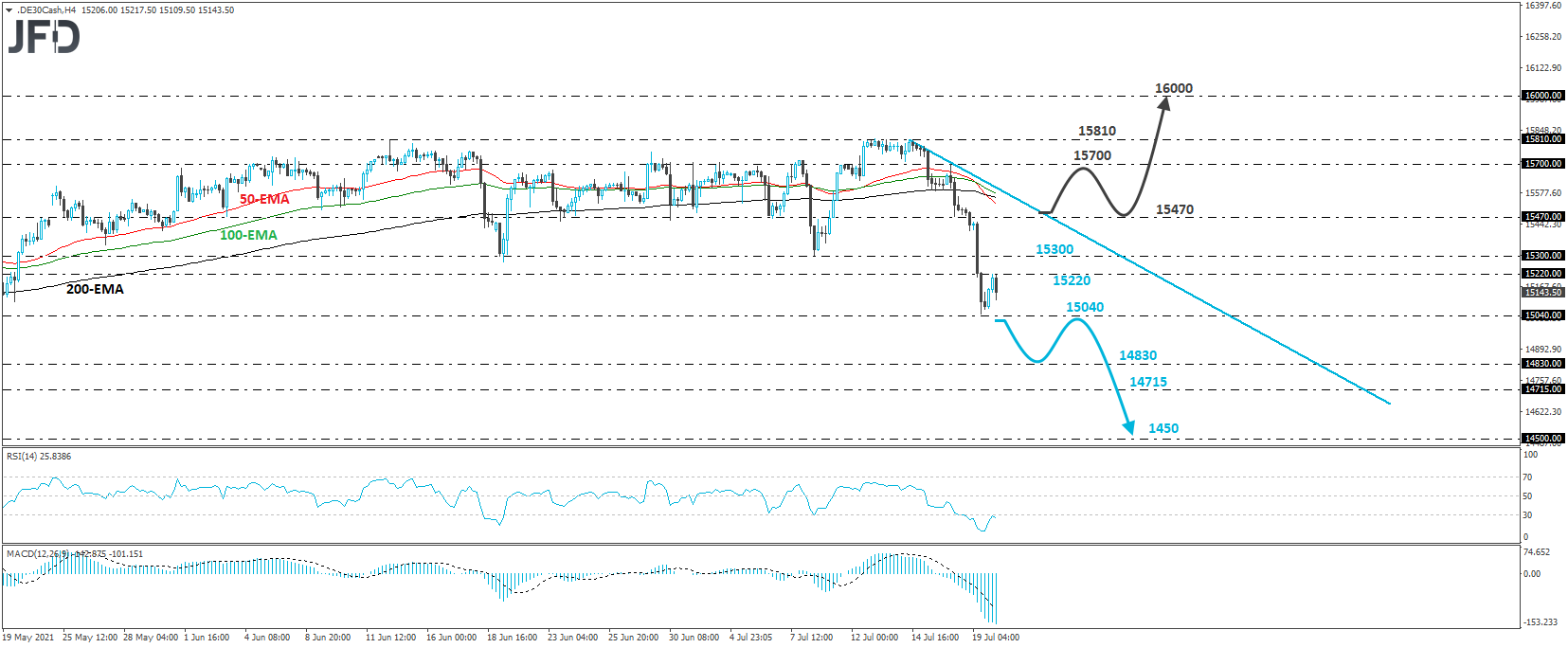

DAX – Technical Outlook

The German DAX cash index tumbled yesterday to hit support near the 15040 level, from where it rebounded somewhat. However, the recovery remained limited, as the index hit resistance near the 15220 area and during the Asian session, it retreated again. Even if we see another round of recovery, given yesterday’s large tumble, and also that the index is trading below the downside resistance line drawn from the high of July 14, we see decent chances for another round of selling.

A break below 15040 would confirm a forthcoming lower low and may initially pave the way towards the 14830 zone, which is defined as a support by the lows of May 4 and 13. Slightly lower lies the 14715 area, marked by the low of Mar. 29, the break of which could extend the fall towards the 14500 territory, which provided strong support between March 11 and 25.

On the upside, we would like to see a recovery back above 15470 before we start examining the bullish case again. This would take the index above the aforementioned downside line and may initially open the path towards the 15700 level, marked by the high of July 16, or the all-time high of 15810, which acted as a ceiling on June 14, and July 13 and 14.

If market participants eventually enter the uncharted territory, the next to consider as a resistance may be the round figure of 16000.

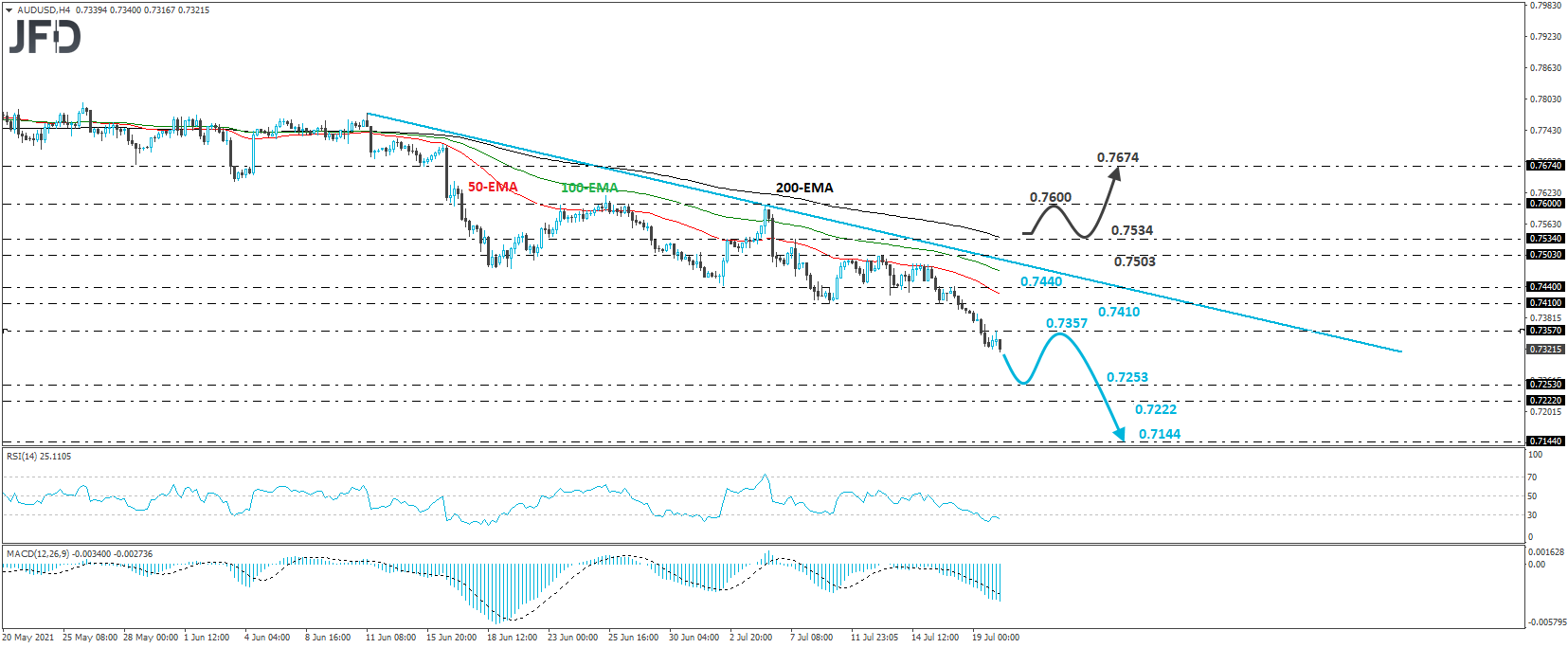

AUD/USD – Technical Outlook

AUD/USD drifted south as well yesterday and today in Asia, extending the short-term downtrend marked by the tentative downside resistance line taken from the high of June 11. With that in mind, and also taking into account that the rate is also trading below all three of our moving averages on the 4-hour chart, we will consider the short-term picture to be negative.

We believe that if the bears are willing to stay in the driver’s seat, we could soon see a test near the 0.7253 barrier, marked by the low of Nov. 19, or the 0.7222 hurdle, defined as a support by the low of Nov. 13. If neither zone is able to stop the decline, then a break lower may see scope for extensions towards the low of Nov. 5, at 0.7144.

In order, to abandon the bearish case and start examining a bullish reversal, we would like to see a break above the aforementioned downside line, followed by a move above the 0.7534 resistance level, marked by the high of July 7.

This may also take the rate above all three of our moving averages on the 40 hour chart and may set the stage for the 0.7600 zone, defined as a resistance by the high of July 6. Another break, above 0.7600, could set the stage for advances towards the 0.7674 area, marked by the inside swing low of June 15.

As For Today's Events

During the Asian session, we already got the minutes from the latest RBA monetary policy meeting, and as we expected, they passed unnoticed. They just confirmed officials’ dovish stance and the view that interest rates are likely to stay untouched until 2024. This, combined with lockdowns in Australia being extended, could keep the aussie under selling pressure.

The rest of the day appears to be light, with the only releases worth mentioning being the US housing starts and building permits for June, as well as the API report on crude oil inventories for last week.

Both the housing starts and building permits are expected to have increased somewhat, while, as it is always the case, no forecast is available for the API number.

As for tomorrow, during the Asian session Wednesday, we have Australia’s preliminary retail sales, which are forecast to have slid 0.5% mom after increasing 0.4%.