- Jump in payrolls halts tech rally, revives dollar bulls; Fed speakers eyed next

- Yen tumbles on reports that Kuroda successor will be architect of BoJ’s ultra-easy policy

- Gold takes a hit from surging yields, but pares losses on US-China tensions

Markets learning to not fight the Fed

Friday’s payrolls report sent markets into a spin as the US economy added a staggering 517k jobs in January, disproving concerns about a worsening slowdown. More crucially, the fact that the labour market is spawning so many jobs at this late stage of the tightening cycle fully backs the ‘higher for longer’ case for interest rates, while seriously questioning the market bets for rate cuts later this year.

But the NFP figures weren’t the only dealbreaker for those holding out for an early policy pivot by the Fed. The potential nail in the coffin came from the ISM non-manufacturing PMI, which also surpassed expectations, not just activity and new orders, but also for the prices paid components. The latter likely served as a reminder to traders that the fight against inflation is far from complete even if the worst is over.

The data sparked a sharp repricing in Fed fund futures, pushing the Fed’s expected terminal rate back above 5.0%, while the odds of a rate cut in the second half of 2023 fell significantly. The US economic agenda is a lot quieter this week but that won’t mean markets will be calmer as there’s a slew of Fed speakers lined up, including Chair Powell on Tuesday.

After Powell’s mixed signals last week, which fuelled the rally on Wall Street, policymakers’ comments in the coming days will likely determine whether Friday’s selloff was just a blip or a much-needed reality check.

Stocks are down, but no panic selling

Tech shares, which had been leading the latest advance in equity markets tumbled the most on Friday as bond yields shot up in the aftermath. The US 10-year Treasury yield is continuing to climb today, brushing an intra-day high of 3.58%, which is a gain of more than 20 basis points from Friday’s lows.

With tech valuations already under scrutiny following the January rebound, higher yields could cap further gains if this is only the start for the recovery in yields. But investors will probably want to see more when it comes to the outlook for the US economy before cutting their exposure more substantially. Although payrolls surged and the jobless rate ticked lower, wage growth moderated slightly in January, boosting hopes of a soft landing. Next week’s CPI report will be vital for supporting this view.

Another reason why the damage on Wall Street wasn’t greater is that the Fed is unlikely to become even more hawkish than it already is and the worst-case scenario is that rates will reach 5.0-5.25% and stay there for a while – something that’s already been communicated by policymakers.

The Nasdaq Composite closed 1.6% lower on Monday and the S&P 500 by 1.0%. E-mini futures remain in the red today ahead of earnings from Activision Blizzard (NASDAQ:ATVI).

Gold takes a knock, but pares losses on geopolitical flare-up

Gold prices were attempting a recovery on Monday after briefly touching a low of $1,860/oz earlier in the session. The revival in yields and the dollar does not bode well for gold’s uptrend and although the precious metal is down about 5% from last week’s peak of just under $1,960/oz, this could be an overdue short-term correction following an impressive three-month rally.

For now, though, gold is finding support from geopolitical tensions amid renewed frictions between Washington and Beijing. The US shot down a Chinese satellite flying over American airspace on Saturday, suspected to be a spy balloon. China says the balloon was gathering weather data and has accused the US of overreacting. The incident comes just as the relationship between the two sides was seen to be thawing recently.

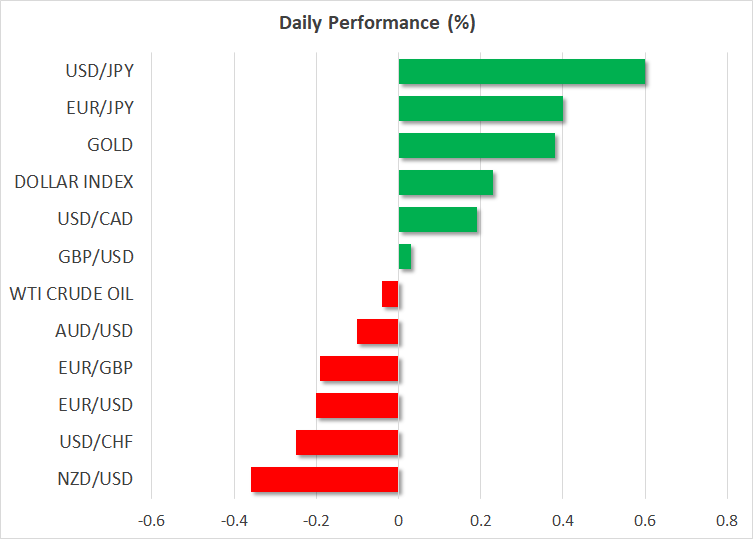

Dollar extends post-NFP gains as yen sinks

But there was no safe-haven boost for the Japanese yen as the currency slid across the board today on the back of reports that the next governor of the Bank of Japan falls under the same dovish camp as Kuroda. The Japanese government is denying the report but if correct, Deputy Governor Masayoshi Amamiya, who was one of the architects of the Bank of Japan’s ever-expanding stimulus programme, would succeed Kuroda when his term expires in April.

What this means for the yen is that if Amamiya is appointed the next chief, he would not be in any hurry to scale back all the stimulus, and even if yield curve control is scrapped, negative interest rates are less likely to be normalized.

The US dollar jumped above the 132-yen level today, while against a basket of currencies, it is at a near four-week high.

The New Zealand dollar was the worst performing major on Monday and the aussie wasn’t far behind. But there could be a boost for the Australian currency early on Tuesday if the Reserve Bank of Australia strikes a somewhat more hawkish tone when it announces its latest policy decision.