- Fed rate cut bets continue to be priced out, all eyes on core PCE inflation

- US dollar softer today but still headed for third weekly gain

- Debt deal progress and AI buzz lift Wall Street, global equities

Fed rate cut bets pushed back as summer hike seen certain

The US dollar eased off two-month highs on Friday as the three-week rally paused for breath amid the sharp repricing of the Fed’s rate path. Treasury yields also cooled off as investors await the next set of clues on Fed policy from the latest PCE inflation data due later today.

The big swings of late in Fed fund futures are unusual in the sense that there’s still not enough clarity about the possibility as well as the timing of one more rate increase, yet the Fed’s message that it is inconceivable to be thinking about rate cuts finally seems to be getting through to investors.

Markets have dramatically scaled back expectations of looser policy in 2023 and the current pricing indicates just one 25-basis-point cut with around 70% probability by year end. However, whilst they see high odds of a summer hike, investors have become less certain on the precise timing following the May meeting minutes on Wednesday, which appeared to be making the case for a pause in June even as several policymakers argued for the need for further tightening.

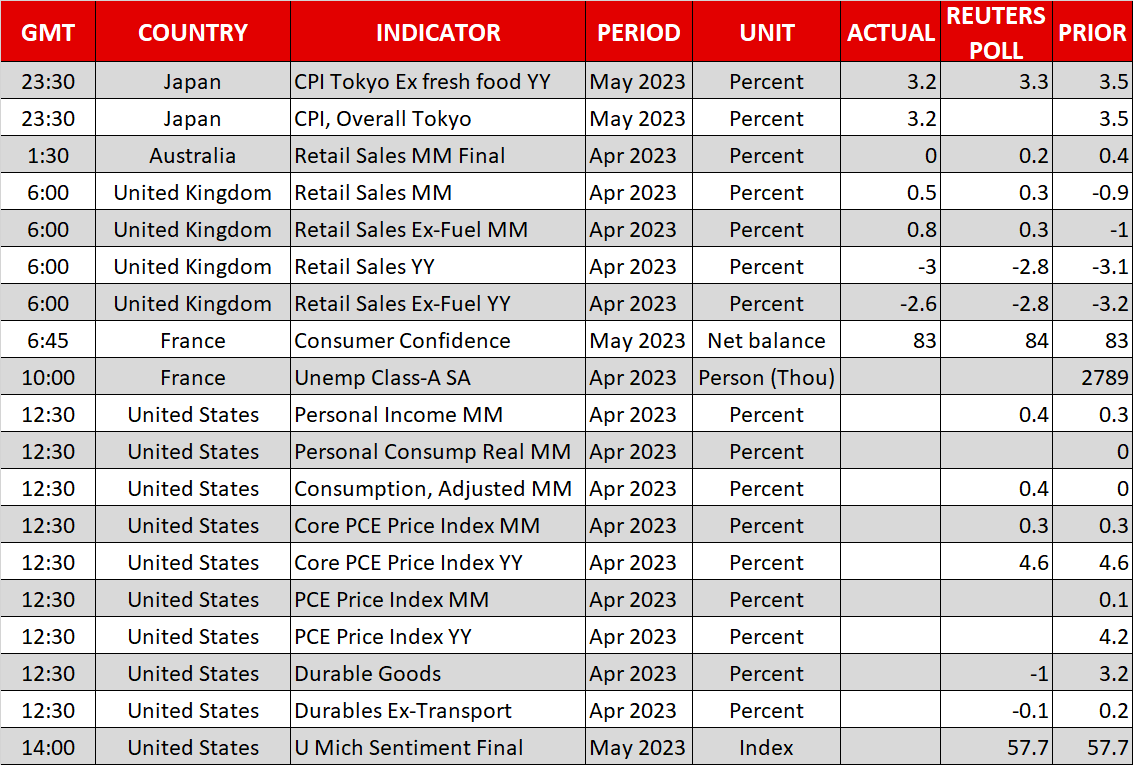

Dollar bulls on standby ahead of core PCE

Persistently high inflation and a hot labour market are two of the three big concerns for Fed officials. The other is tightening credit conditions, which was stressed several times in the minutes. With two more inflation reports and one jobs report to go until the June meeting, the incoming data will be crucial, putting the spotlight on today’s releases.

The all-important core PCE price index is expected to have held steady at 4.6% y/y in April, while personal consumption likely rebounded by 0.4% m/m. US GDP growth in Q1 was revised slightly up yesterday in the second estimate and weekly jobless claims beat expectations, so more strong numbers today could reverse the dollar’s early session pullback.

Pound leads the recovery against the dollar

For the time being though, battered currencies are capitalizing on the greenback’s softness to claw back some of the heavy losses from this week. The aussie and kiwi slumped to more than six-month lows yesterday and overnight, while the euro and pound are at two-month lows. The yen also hit a six-month trough as US-Japanese yield differentials are back in focus after the latest hawkish Fed bets and the absence of any explicit tightening signal from the Bank of Japan.

Leading the rebounds on Friday is sterling, as better-than-expected retail sales figures out of the UK earlier have reinforced the view that the Bank of England has more rate hikes in the pipeline than other central banks. CPI readings for the Tokyo region on the other hand were slightly weaker than anticipated. Nevertheless, the yen is joining in today’s bounce back against the mighty dollar.

In emerging market currencies, the Turkish lira hit a new record low against the greenback, breaching the 20 mark for the very first time amid the second round of presidential elections in Turkey on Sunday where incumbent President Tayyip Erdogan is widely expected to win another term.

Rising yields offset by AI and debt deal boost in equity markets

On Wall Street, there were few signs of stress from surging yields as an AI-driven rally and relief that a deal on increasing the US debt ceiling is nearing bolstered equities.

Nvidia (NASDAQ:NVDA) led the charge in AI stocks as its share price skyrocketed by 24%, lifting the Nasdaq Composite by 1.7%. The S&P 500 closed up 0.9%, but the Dow Jones shed 0.1%, highlighting how uneven this latest upswing on Wall Street has been.

The AI revolution has clearly injected some fresh lease of life into stocks, but it doesn’t change the fact that there are still a number of uncertainties hanging over the markets. However, one of those uncertainties could be removed soon as the White House and Republicans appear to be edging closer to reaching a deal on raising the debt ceiling.

With time running out fast before the June 1 deadline, President Biden and Republican House Speaker Kevin McCarthy are on the verge of agreeing to cap federal spending for two years while raising the debt limit.

The optimism spread to Asian markets today, though European stocks were mixed and US futures were either flat or marginally in the red.