On Aug 22, we issued an updated research report on Deere & Company (NYSE:DE) , a producer and distributor of agricultural and forestry equipment, construction equipment and engines.

Deere is expected to gain from continued strength in farm income and improving construction. However, declining global grain supply use balance, unfavorable impact of raw material prices and rising expenses will hurt its performance.

In its third-quarter conference call, Deere raised total equipment sales growth outlook to about 10% year over year for fiscal 2017. It projects 24% sales growth for the fiscal fourth quarter, compared with year-ago period.

For 2017, the United States Department of Agriculture (USDA) forecasts increase in global grain consumption for the 22nd consecutive year. The World Agriculture Supply Demand (WASD) report forecasts ample supplies of corn and soybeans from large acreages. Notably, a turnaround in farm income is forecast for calendar year 2017, the first increase since the peak reached in 2013.

Meanwhile, global food and agricultural trade is growing despite sluggish GDP growth and the prospects are better for 2018 and 2019. Per the latest IMF forecast, global GDP growth is projected at around 3.6% in 2018 and 3.7% in 2019 compared with 3.5% forecast for this year. All of these factors hint at continued strength in farm income.

Deere also expects commercial and institutional construction to continue increasing moderately in fiscal 2017. Notably, machinery rental utilization rates have improved in each of the last six months and rental rates are looking up. Also, construction investment is projected to grow in fiscal 2017 by about 3% led by a rebound in oil and gas and residential activity.

However, the global grain supply use balance is tightening somewhat with consumption outpacing production for the first time since 2012. This suggests that the commodity markets might get more sensitive.

Deere expects sales to be flat to down 5% in the EU28 region in fiscal 2017 due to low commodity prices and farm income. Low crop prices and arable farm income continues to weigh on the local market.

Deere’s fiscal 2017 cost of sales outlook is pegged at about 77% of net sales. Further, the company forecasts SA&G expense hike of about 11% for the full year. Most of the full-year change is expected to come from incentive compensation, voluntary separation expenses, commissions paid to dealers, acquisition-related activities and currency exchange. These expenses will hurt earnings considerably.

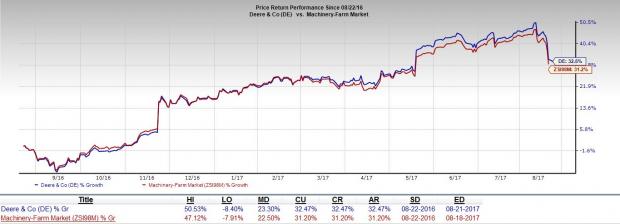

It should be noted that Deere has outperformed the industry in the last one year. While shares of the company have gained 32.5%, the industry gained 31.2% in the same period.

Currently, Deere carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the industrial product space are Caterpillar Inc. (NYSE:CAT) , Terex Corporation (NYSE:TEX) and AGCO Corporation (NYSE:AGCO) . All of these stocks sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Caterpillar has an expected long-term growth of 9.50%.

Terex has an expected long-term growth of 19.67%.

AGCO projects long-term growth at around 13.51%.

Zacks' 10-Minute Stock-Picking Secret

Since 1988, the Zacks system has more than doubled the S&P 500 with an average gain of +25% per year. With compounding, rebalancing, and exclusive of fees, it can turn thousands into millions of dollars.

But here's something even more remarkable: You can master this proven system without going to a single class or seminar. And then you can apply it to your portfolio in as little as 10 minutes a month.

Learn the secret >>

Terex Corporation (TEX): Free Stock Analysis Report

Caterpillar, Inc. (CAT): Free Stock Analysis Report

Deere & Company (DE): Free Stock Analysis Report

AGCO Corporation (AGCO): Free Stock Analysis Report

Original post