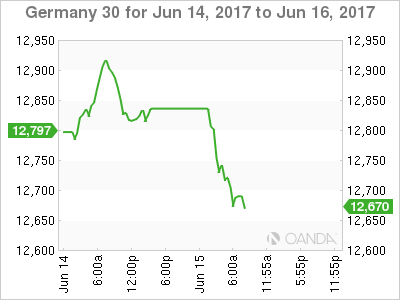

The DAX index has posted considerable losses in the Thursday session, dropping 1.04 percent. The index is currently at 12,684.50 points. On the release front, the eurozone trade surplus dropped sharply, coming in at EUR 19.6 billion. This was well short of the forecast of EUR 22.4 billion. On Friday, the eurozone releases Final CPI, which is expected to drop to 1.4 percent.

The ECB has indicated it is in no rush to change its ultra-loose monetary policy, despite better economic conditions in the euro-area. However, a major player has long been unhappy about this, and the complaints are getting louder. Germany wants to see a tighter policy out of Brussels, arguing that the current low-interest environment is hurting savers and is ill-fitted to Germany’s strong economy.

On Tuesday, German finance minister Wolfgang Schaeuble called on the ECB to change its policy in a “timely manner”. For its part, the cautious ECB has argued that it must keep its asset -purchase program and low interest rates in place while inflation remains at low levels. However, with Germany facing elections in September, the pressure on the ECB to tighten policy will only increase, especially if economic indicators continue to points upwards.

The US released key consumer indicators on Thursday, and the readings disappointed the markets, as CPI and retail sales reports missed estimates. CPI declined 0.1%, short of the estimate of 0.2%. This was the second decline in three months, as inflation is currently at 1.5%, well below the Federal Reserve’s target of 2.0%. Retail Sales, the primary gauge of consumer spending was dismal, coming in at -0.3%, compared to a forecast of +0.1%.

This marked the indicator’s weakest reading since August 2016. Weak retail sales is clearly an area of concern – the soft reading could drag down GDP for the second quarter, as as consumer spending accounts for more than two-thirds of economic growth. Although surveys continue to show that US consumers remain optimistic about the economy, this hasn’t translated into stronger consumer spending.

The markets had priced in a rate hike at close to 100%, and the Federal Reserve complied, as it hiked rates on Thursday by 25 basis points, to a target range of 1.00 percent to 1.25 percent. The rate statement was more hawkish than expected, as policymakers portrayed an optimistic picture, noting that the economy was growing and the labor market remained strong. As for inflation, which remains stubbornly low, the statement acknowledged that inflation remained below the Fed’s target of 2.0%, but expected that goal to be reached in the “medium term”. The Fed projected one more rate hike in 2017, and the markets are circling the December meeting as the most likely date.

The odds for a September hike are at 18%, down from 23% a week ago, according to the CME Group. As for a December increase, the odds are currently at 38%. One surprising development was that Fed Chair Janet Yellen outlined a plan to reduce its $4.2 trillion balance sheet (comprised of Treasury bonds and mortgage-backed securities). Yellen was short on specifics, saying that the goal was to begin the normalization “relatively soon”.

The balance sheet ballooned after the financial crisis in 2008, as the Fed implemented a massive quantitative easing program as part of its accommodative monetary policy, together with interest rates of zero. The gradual reduction in the purchase of these assets signifies an important vote of confidence in the strength of the US economy.

Fed surprises but is it enough to turn the dollars tide

Economic Calendar

Thursday (June 15)

- 5:00 Eurozone Trade Balance. Estimate 22.4B. Actual 19.6B

- All Day – Eurogroup Meetings

Friday (June 16)

- 5:00 Eurozone Final CPI. Estimate 1.4%

- 5:00 Eurozone Final Core CPI. Estimate 0.9%

- All Day – ECOFIN Meetings

*All release times are EDT

*Key events are in bold

DAX, Thursday, June 15 at 7:00 EDT

Open: 12,805.00 High: 12,808.00 Low: 12,669.75 Close: 12,684.50