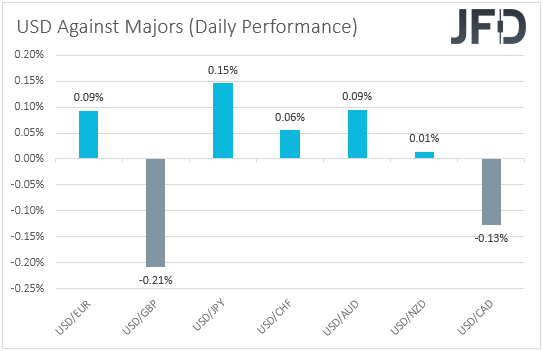

Yesterday, it was a quiet day for the major currencies, with the US dollar staying within a narrow range against most of them. The only one to gain slightly more was the British pound, the traders of which may have increases somewhat their long positions after the BoE said that it will start unwinding its QE program when interest rates hit 0.5%. As for today, the spotlight is likely to turn to the US employment report for July, as market participants try to estimate the time of when the Fed will start normalizing policy.

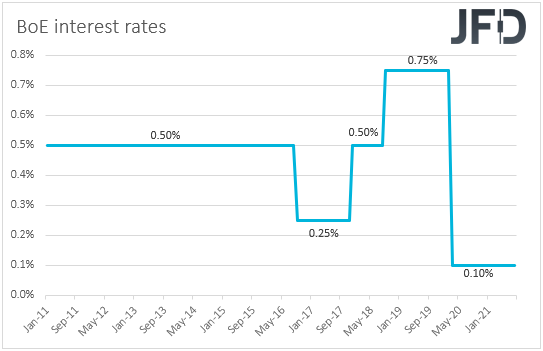

Bank Of England Stands Pat, Will Start Unwinding QE After Rates Hit 0.5%

The US dollar traded quietly against the other major currencies on Thursday and during the Asian session Friday. It traded within a ±0.15% range against all but one. The exception was the British pound, which was found higher against its US counterpart by 0.21%.

What resulted in a slight strengthening in the British currency may have been the outcome of the BoE monetary policy gathering. The Bank kept all its policy settings unchanged, with policymakers voting unanimously in favor of keeping interest rates untouched, but with one member descending on the QE voting. Expectations were for two members to descent, and thus, at first glance, only one official supporting tapering seems somewhat dovish. However, the highlight was not the voting. In our view, it was the Bank’s statement that they will start reducing their stock of bonds when the policy rate hits +0.50%, by not reinvesting the proceeds of maturing debt, as long as that makes sense for the economy. The previous guidance was for the Bank to not start unwinding its bond purchases until interest rates were near +1.5%.

Some participants may have interpreted this as a way of saying that QE tapering may start earlier than previously anticipated and that’s why they bought some pounds. However, it could also be translated as interest rates staying lower for longer. That’s why the pound did not gain much. In any case, markets are pricing a first rate increase to 0.25% around August next year, with the 0.5% threshold expected to be hit in late 2023 or early 2024.

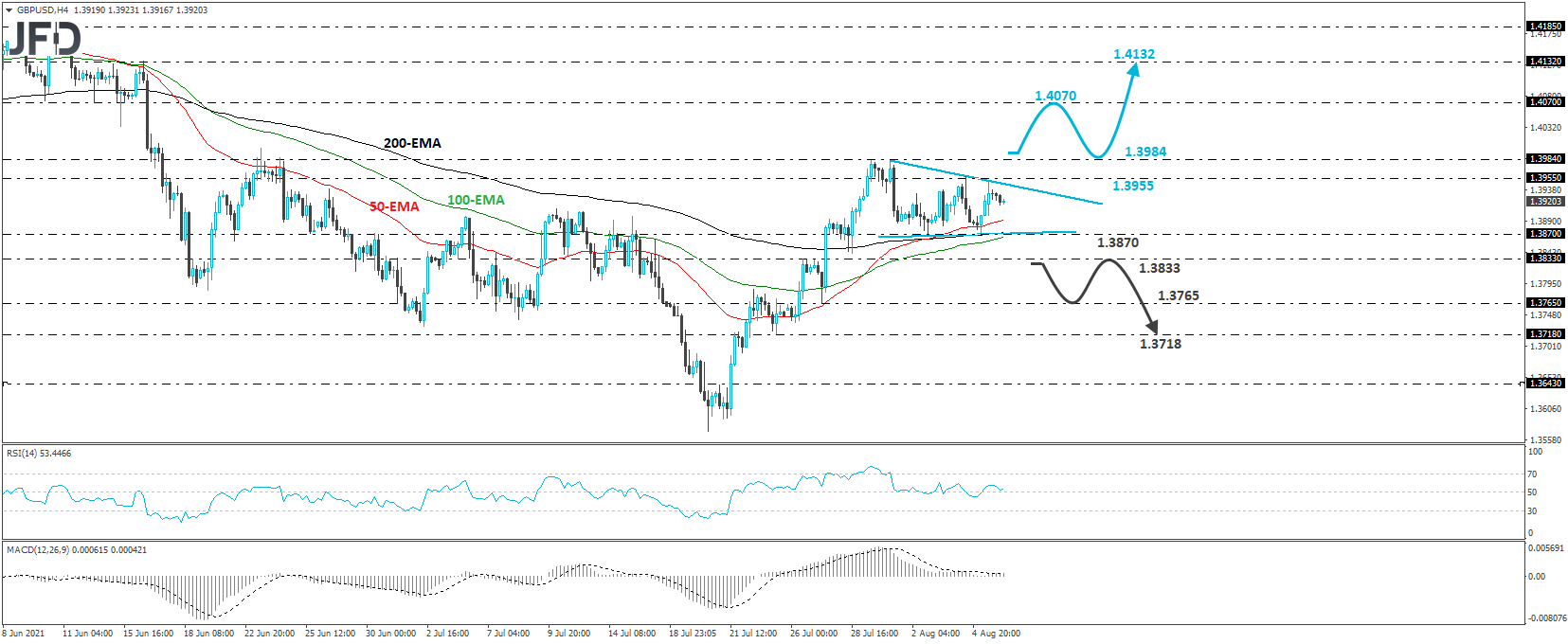

GBP/USD Technical Outlook

GBP/USD traded higher yesterday, after hitting support at 1.3870. However, the advance was stopped by the 1.3855 barrier, and then, the rate retreated somewhat. In the bigger picture, the rate appears to be trading within a small triangle pattern since July 28, and thus, although the prevailing short-term trend is to the upside, we prefer to stand pat for now.

In order to start examining the continuation of the prevailing recovery, we would like to see a break above the 1.3984 barrier, defined as a resistance by the high of July 30. This will confirm a forthcoming higher high on the 4-hour chart and could pave the way towards the 1.4070 territory, which acted as a decent support between June 10 and 16. If that zone is also broken, then we could experience extensions towards the peak of June 16, at 1.4132.

On the downside, we would like to see a dip below 1.3833 before we consider a bearish bias. The rate would already be below the lower end of the aforementioned triangle and may dive towards the 1.3765 obstacle, marked by the low of July 27, the break of which could extend the fall towards the low of July 23, at 1.3718.

US And Canadian Employment Reports On Today's Agenda

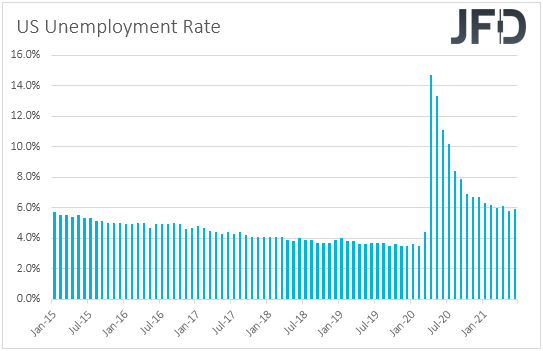

As for today, the spotlight is likely to fall on the US employment report for July. Nonfarm payrolls are expected to have accelerated to 870k from 850k, while the unemployment rate is anticipated to have declined to 5.7% from 5.9%. That said, on Wednesday, the ADP report revealed that the private sector has gained less-than-expected jobs, actually less than half the forecasted number, which tilts the risks surrounding the NFP number to the downside. Average hourly earnings are forecast to have grown 0.3% mom, the same pace as in June, but this will take the yoy rate up to +3.8% from +3.6%.

At last week’s gathering, the FOMC kept its policy unchanged, but although officials repeated that they will keep the pace of their QE purchases unchanged until “substantial further progress has been made” towards their goals, they added that the economy has made such progress, and that they will continue to assess the progress in coming meetings. Having said all that though, at the press conference following the decision, Fed Chief Powell said that the labor market has still a long way to go, and that inflation is still expected to fall back to their longer-run goals. He also added that the timing of taper will depend on incoming data and that they will provide advance notice before any changes, something that may have poured cold water on expectations of an early tightening. However, after that, several other policymakers, and most recently, Fed Vice Chair Richard Clarida, appeared more hawkish than Powell, arguing that it will be appropriate for interest rates to start rising in 2022. Remember the latest dot plot suggests that this could start happening in 2023.

In any case, a downside surprise will be more inline with Powell’s remarks and may result in some USD selling. At the same time, equities are likely to gain more on expectations that with QE tapering not in sight soon, borrowing costs will stay cheap for longer. On the other hand, a strong report could undermine Powell’s view and may revive speculation over early tapering, and thereby earlier rate hikes. The US dollar could gain in this case, while equities could correct lower, even if a strong report means that the economic recovery remains robust.

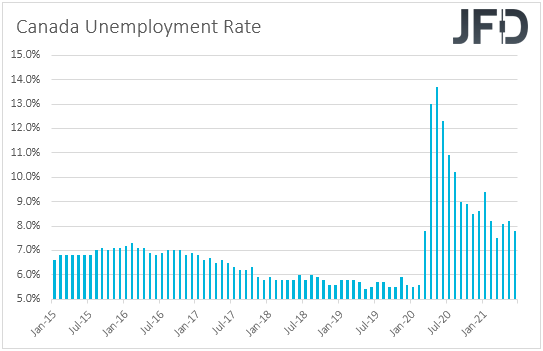

At the same time with the US employment report, we get jobs data for July from Canada as well. The unemployment rate is forecast to have declined to 7.4% from 7.8%, while the employment change is expected to reveal a slowdown to 177.5k from 230.7k. That said, a 177.5k jobs growth still appears decent to us.

At its prior gathering, the BoC appeared less hawkish than expected, saying that they continue to see the output gap closing in H2 2022, which suggests that their expectations over when they may start raising interest rates have not come forth. What’s more, last week, both headline and core Canadian inflation rates declined, which may have added credence to that view. However, a strong employment report may raise some speculation over a somewhat earlier action by the BoC, and perhaps support the Canadian dollar.

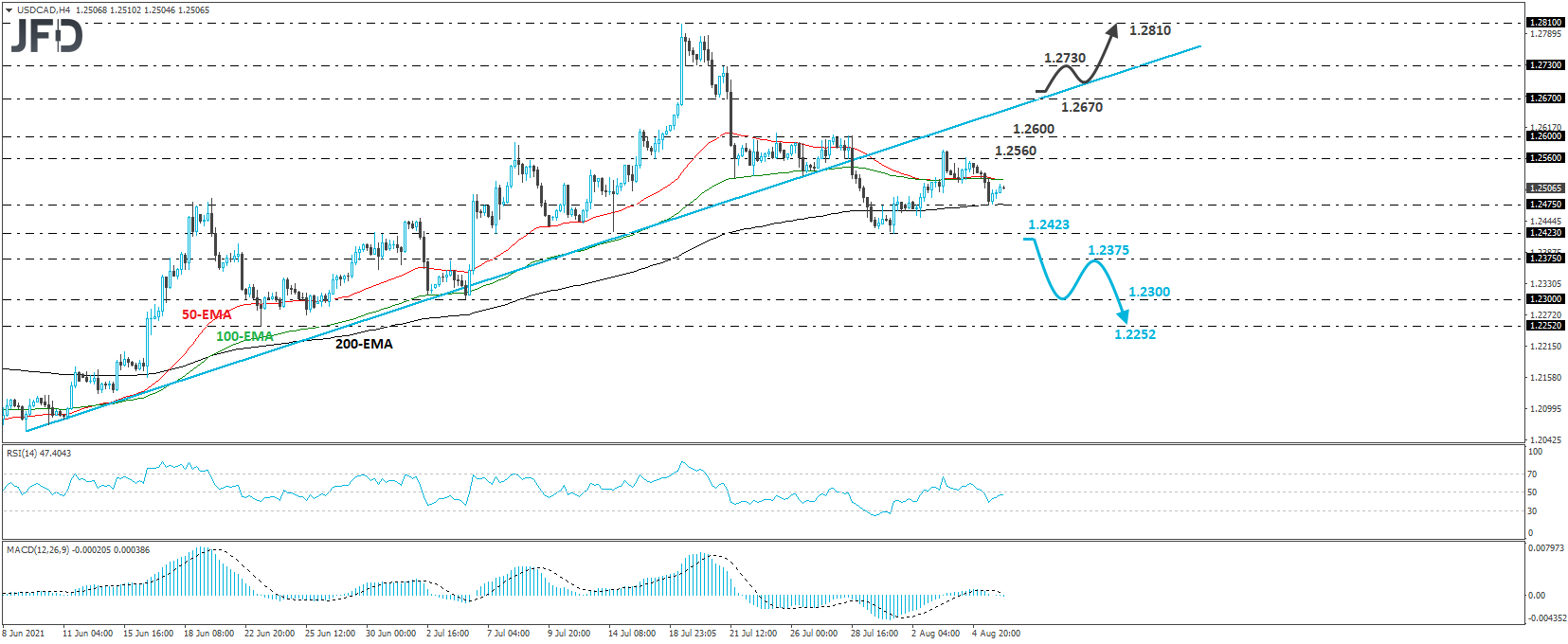

USD/CAD Technical Outlook

USD/CAD traded lower on Thursday morning, but hit support near 1.2475, and then, it rebounded somewhat. Overall, the pair remains below the prior upside support line drawn from the low of June 9, and thus, we would see decent chances for the bears to take charge again soon and push the rate lower.

That said, we will get confident on more declines only if we see a dip below 1.2423. Such a move will confirm a forthcoming lower low on the 4-hour chart and could initially target the inside swing high of July 5, at 1.2375. If the bears are not willing to stop there, then we could see them pushing the action down to the 1.2300 zone, marked by the low of July 6, or the 1.2252 barrier, defined as a support by the low of June 23.

On the upside, the move that would make us start reexamining the bullish case is a recovery above 1.2670. This may also signal the rate’s return above the upside support line drawn from the low of June 9, and may firstly target the 1.2730 barrier, marked by the high of July 21. Another break, above 1.2730, could see scope for extensions towards the peak of July 19, at around 1.2810.