In a landscape punctuated by unforeseen events, Kotak Mahindra Bank (NS:KTKM)'s recent earnings report emerges as a pivotal moment, marked by notable developments such as regulatory actions and leadership transitions. Despite the backdrop of uncertainty, the bank delivered a robust performance, underscoring its resilience and strategic prowess.

Kotak Mahindra Bank showcased a commendable earnings performance, with core Pre-Provision Operating Profit (PPOP) witnessing a 15% year-on-year growth. Adjusting for one-offs, this growth stood at 11% year-on-year, surpassing market expectations by 7%. Profit After Tax (PAT) also exhibited strong growth, increasing by 18% year-on-year, with core PPOP-Return on Assets (ROA) and ROA reaching 3.4% and 2.5% respectively, excluding one-offs. This robust performance was attributed to sequential improvements in Loan-to-Deposit ratio and enhanced cost-to-income ratio, driven by robust fee income growth and resilient lending spreads.

Under the stewardship of the new management, Kotak Mahindra Bank articulated a comprehensive strategy focusing on IT infrastructure enhancement, risk-reward optimization, and accelerated loan growth, while upholding profitability and asset quality. The bank's commitment to deepening customer relationships and streamlining IT expenditures underscores its proactive approach towards addressing emerging challenges.

Goldman Sachs (NYSE:GS) revised its FY25/26 EPS estimates upwards by 8% and 2% respectively, reflecting stronger-than-anticipated Net Interest Margins (NIMs) and fee income. Despite factoring in the potential impacts of recent regulatory actions, Goldman Sachs remains bullish on Kotak Mahindra Bank's medium to long-term prospects, projecting a robust 21% core PPOP Compound Annual Growth Rate (CAGR) over FY24-FY26E. With a strong focus on loan book expansion and a well-diversified retail banking portfolio, Kotak Mahindra Bank is poised to sustain its competitive edge and deliver superior returns.

The bank's performance in the fourth quarter of FY24 showcased several noteworthy achievements, including a marginal decline in calculated margins, robust fee income growth, strong deposit mobilization, and healthy growth in net advances. Despite slight asset quality deterioration, the bank's proactive approach towards IT investments and customer acquisition bodes well for its long-term growth trajectory.

Goldman Sachs maintains a Buy rating on Kotak Mahindra Bank, with a revised 12-month target price of INR 2,170 per share. The target valuation multiple of 19.2x FY25E standalone P/E reflects the bank's resilient earnings potential and strategic positioning. However, downside risks such as continued global investor sell-off, subdued performance in subsidiaries, and regulatory uncertainties warrant vigilance and prudent risk management.

Image Source: InvestingPro+

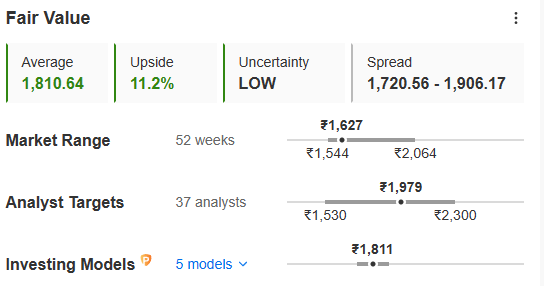

Investors can also look at the fair value of stocks across the globe. In the case of Kotak Mahindra Bank, the fair value is INR 1,810 per share, depicting an 11.2% from the CMP of INR 1,627. This has been calculated after taking 5 different financial models into consideration.

Amid evolving market dynamics and regulatory headwinds, Kotak Mahindra Bank stands as a beacon of stability and resilience in India's banking sector. With a robust earnings trajectory, strategic vision, and prudent risk management practices, the bank is well-positioned to navigate uncertainties and unlock value for its stakeholders in the years ahead.

To get more insights into valuation, financial health, red flags, etc. subscribe to InvestingPro by clicking here, for just INR 216/month! Avail this limited-time offer today and take your investment journey to the next level for a very affordable price!

X (formerly, Twitter) - Aayush Khanna