Morgan Stanley (NYSE:MS)'s latest analysis paints a nuanced picture of India's consumer industry, leading to a revision of their view from "Attractive" to "In-Line." Despite a favorable GDP growth outlook, driven by cyclical businesses, the defensive consumer sector is anticipated to lag behind due to intensified competition and changing consumer behavior.

The report underscores several key factors contributing to this shift. Heightened competition in the household and personal care (HPC) segment, driven by pricing, product, and distribution strategies, is expected to persist. This, coupled with lower growth expectations and rich valuations, is likely to lead to a de-rating of the consumer sector.

Offer: Unlock the true value of stocks with InvestingPro by clicking here – your ultimate stock analysis tool! Say goodbye to inaccurate valuations and make informed investment decisions with accurate intrinsic value calculations. Get it now at a limited-time discount of 69%, only INR 216/month!

Morgan Stanley's India equity market strategist, Ridham Desai, highlights the ongoing upcycle in India's economy. However, this upcycle poses challenges for staple stocks, with cyclical consumption outperforming defensives. Projections indicate GDP growth rates of 6.8% and 6.5% in FY25 and FY26 respectively, supported by a rebound in capital expenditure.

In the context of this cyclical uplift, consumer staple businesses are expected to underperform due to their defensive nature. Similar trends were observed in the 2003-07 cycle, where staple stocks significantly lagged behind as the economy picked up momentum.

While consumption remains a pillar of India's economic growth, post-pandemic recovery has been uneven, particularly in rural areas. Factors such as a shift towards services, slower rural demand recovery, and ongoing adjustments in household budgets contribute to this mixed growth outlook.

However, there's optimism for a gradual recovery in consumption growth, supported by factors like inflation moderation, rural sector resilience, and improving labor market conditions. This aligns with India's long-term consumption story, as outlined in Morgan Stanley's BluePaper, projecting sustained consumption growth and a shift towards discretionary spending as income levels rise.

While challenges persist in the consumer sector, India's consumption narrative remains intact, poised for growth as the economy evolves and consumer preferences shift. Morgan Stanley's analysis provides valuable insights for investors navigating the dynamic landscape of India's consumer industry.

Some of the consumer stocks that investors need to stay cautious of due to their overvaluation are:

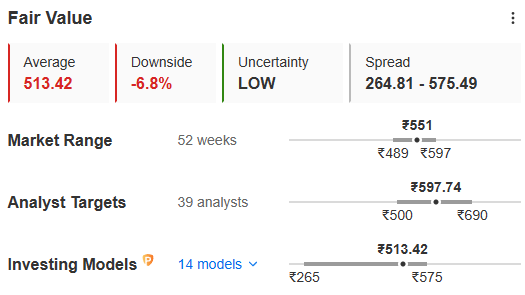

Image Source: InvestingPro+

Dabur India (NS:DABU) - The stock has delivered a meager return of 7.3% in the last one year, despite which it seems overvalued by 6.8%. Even 39 analysts covering this counter are not too bullish, giving a minor upside till INR 597.

Image Source: InvestingPro+

Hindustan Unilever (LON:ULVR) (NS:HLL) is another underperformer with a one-year return of -8.43%. ProTips is throwing a plethora of red flags on the valuation front and the fair value after analyzing the stock from 14 different financial models is INR 2,214, overvalued by 6.4%.

InvestingPro, the ultimate stock analysis tool, is now within reach at a discount of up to 69%, offering unparalleled insights for just INR 216 per month, but hurry, this offer won't last long! Click here to grab your offer

Also Read: Driving Growth: Insights into India's Auto Dealership Landscape

X (formerly, Twitter) - Aayush Khanna