(Bloomberg) -- When China’s securities regulator vowed to reduce market volatility in January, few predicted that this year would be one of the most turbulent in recent memory.

The drama has only increased this quarter, setting the scene for more upheaval in 2023.

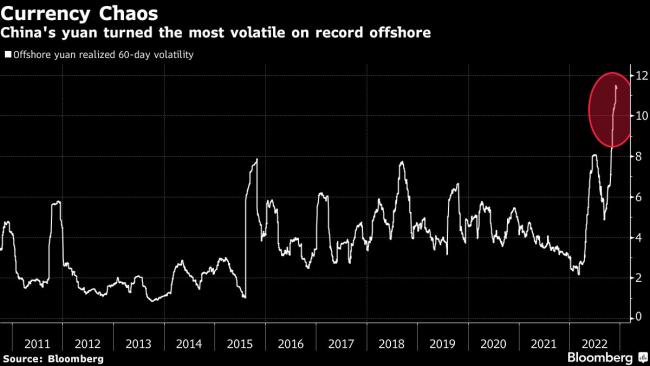

Chinese stocks are now moving by 5% a day more frequently than anytime since the global market meltdown of 2008. Volatility in the offshore yuan is near a record. And the cost of insuring Chinese government debt against default has been at multi-year highs.

While market consensus is that Chinese assets will rise over the next 12 months, catalysts for extreme shifts in sentiment remain everywhere: from the risk of overwhelming infections as Covid Zero rolls back, to the lingering property crisis and a regulatory culture that never ceases to spring surprises. China’s relations with the US are still fraught, and the economic outlook at home and abroad is more uncertain than ever.

Traders who were burned after placing bets on a China rally this time last year are back. But they are far more cautious.

“It’s not going to be a one-way smooth ride,” said Keiko Kondo, head of multi-asset investments for Asia at Schroder Investment Management in Hong Kong. “Investor sentiment is still quite fragile — one thing people don’t want to have is too much volatility. That is why we haven’t gone all the way to overweight on Hong Kong and mainland shares.”

Traders are expressing their caution by piling into derivatives that will pay out if stocks and the yuan come crashing down, while building a hoard of those that should profit if these assets soar.

The HSCEI Volatility Index, which serves as a barometer of fear for the Hong Kong stock market, is up 50% this year and far above its average over the last decade, even after sliding from its October high. While all global markets have seen volatility, the equivalent VIX gauge for US equities is well behind with a 33% increase since the start of 2022.

“2023 is not going to be easy,” Kieran Calder, head of equity research for Asia at Union Bancaire Privee, said on Bloomberg Television. “We’re cautiously optimistic on reopening in China. The big swing factor is how China gets out of Covid and how fast.”

Bulls are building their case on Beijing’s refocus on the economy as officials consider a 5% growth target for 2023. Achieving that goal would likely require a well-executed exit from Covid Zero and the scrapping of further deleveraging in the property market — two policies that have depressed the valuations of Chinese assets for almost two years.

Because valuations are so low and positioning by global investors is light after steep outflows, it won’t take much for the recovery in asset prices to continue. But it won’t take much to generate volatility with these ingredients either.

The language that accompanies the current chorus of buy calls on Chinese assets reflects a degree of caution that wasn’t present a year ago.

“The path will be bumpy,” Morgan Stanley (NYSE:MS) strategists including Laura Wang wrote in a recent note upgrading Chinese stocks.

“Activity is restarting, but we see China on a path to lower growth,” wrote the team at BlackRock (NYSE:BLK) Investment Institute.

“Things could remain volatile,” said abrdn plc’s Christina Woon.

The case from bears heaps pessimism on top of the same warnings on volatility that come from the bulls.

For them, the confirmation of Xi Jinping’s third term atop the Communist Party means continued risk for China’s financial markets rather than policy stability.

There is little indication that policy making will become more transparent and predictable. A case in point was health officials vowing “unswerving” adherence to Covid Zero as recently as November, only for state media to claim near victory over the virus this month, whipsawing markets along the way rather than calming them.

“Although some stock promoters continue to recommend China as a recovery trade for 2023, this narrative has been around since the spring and many are giving up,” said Simon Edelsten at Artemis Investment Management LLP in London.

For investors who target growth and a market-friendly governance framework, the arguments to avoid China over the longer term have become stronger, he said. Edelsten’s team has cut the exposure to Chinese assets in the two products they manage to a 1% holding in Hong Kong insurer AIA Group (OTC:AAGIY) Ltd.

Still, volatility may be worth the risk for shorter-term tactical traders as beaten-down assets jump back up. Consider returns of 500%-plus for Country Garden Holdings Co. bonds, or the rally of more than 200% in shares of Alibaba (NYSE:BABA) Health Information Technology Ltd. since late October.

“The market is likely to be volatile amid a bumpy transition period ahead,” wrote Mark Haefele, chief investment officer at UBS Global Wealth Management. “But we also see opportunities in sectors that will directly benefit from China’s shift to eventual reopening, including pharma and medical equipment, consumer, internet, transportation, capital goods, and materials.”

©2022 Bloomberg L.P.