(Bloomberg) -- US households showed signs of increasing financial stress in the first quarter, with credit card balances not declining in the way they typically do at the start of the year and delinquencies rising for most types of consumer loans.

Households added $148 billion in overall debt, bringing the total to $17.05 trillion, according to a report released by the Federal Reserve Bank of New York on Monday. Balances are now $2.9 trillion higher than just before the pandemic.

Consumers typically build up more credit-card debt at the end of the year, during the holiday season, and then reduce those balances at the start of the following year, sometimes with the help of tax refunds. But for the first time in 20 years, that wasn’t the case this year, suggesting some households are under strain from higher prices and may be relying on credit cards to maintain their spending.

“Credit card balances were flat in the first quarter, at $986 billion, bucking the typical trend of balance declines in first quarters,” researchers wrote in the report.

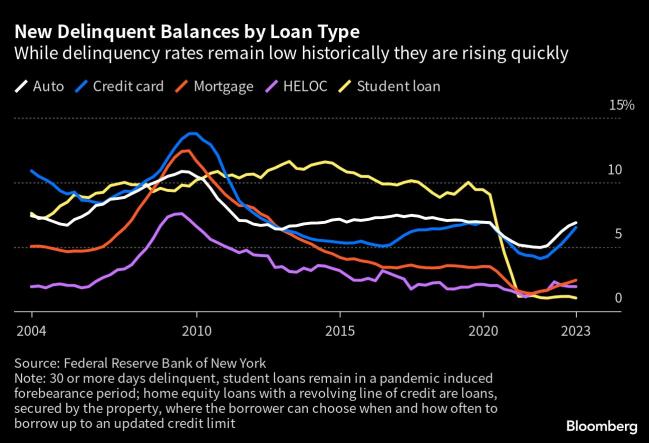

The overall delinquency rate remained low by historical levels, at 2.6%. But the share of debt that became delinquent — meaning it was at least 30 days late — is rising for most loan types, including credit cards and auto debt.

Many households took advantage of federal stimulus payments and forbearance programs for student loans and other debt to build up savings and pay down credit-card debt and other loans during the pandemic. Some of that was reversed as consumers resumed more normal spending patterns, including traveling and going out to restaurants.

Student loan delinquencies, however, have remained flat, with the federal forbearance on payments and interest still in place. Younger borrowers, who have been struggling more to keep up with debt payments, could face even more pressure after student loan payments are resumed, New York Fed researchers said.

Mortgage debt trends

Mortgage originations dropped sharply in the first quarter, to $324 billion, the lowest seen since the second quarter of 2014. That was after a period dubbed the “taper tantrum,” when mortgage rates spiked because investors became concerned the Fed would suddenly end its asset purchases.

In another sign that consumers are tapping into available credit: Balances on home equity lines of credit increased by $3 billion at the start of the year, rising for the fourth straight quarter after declining for nearly 13 years. Some borrowers who locked in lower mortgage rates may prefer to tap into their equity through a line of credit instead of refinancing their mortgages into a higher rate, New York Fed researchers said.

Still, there were some signs that many households became better positioned to withstand financial challenges during the pandemic, especially by refinancing their mortgages to significantly reduce their monthly payments.

In a separate blog post, New York Fed researchers said that 14 million mortgages were refinanced between the second quarter of 2020 and the fourth quarter of 2021, during which $430 billion of home equity was extracted through cash-out refinances.

About 64% of these mortgages were “rate refinances,” where balances increased by less than 5% of the total loan amount. That led to an average payment reduction of $220 monthly for those borrowers.

“The mortgage refinancing boom is over, but its impact will be seen for decades to come,” said Andrew Haughwout, director of household and public policy research at the New York Fed.

©2023 Bloomberg L.P.