(Bloomberg) -- Britain is headed for a deep recession, with the Bank of England working to clamp down on inflation in a move that may cost the economy at least half a million jobs.

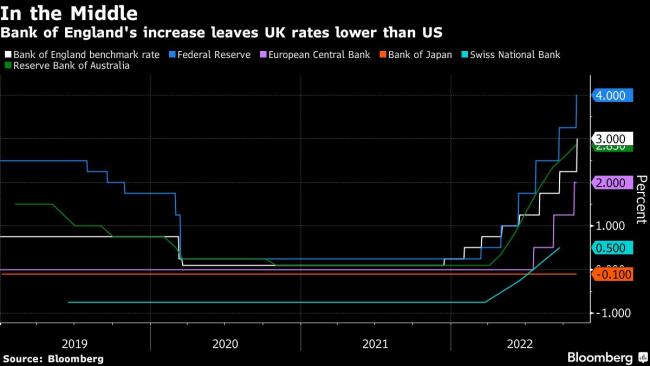

The UK central bank pushed through its biggest interest rate increase in 33 years on Thursday, bringing the benchmark lending rate to a 14-year high of 3%. It estimated unemployment may rise to just above 5% even if borrowing costs remain steady and the economy may shrink 1.7% over 18 months -- not recovering for three years.

The outlook underscores the headwinds Rishi Sunak’s government faces in the runup to the next election, with the Treasury planning a package of spending cuts and tax increases on Nov. 17. While economists are relieved the BOE and Treasury appear to be working together again after an ill-fated stimulus package abruptly ended Liz Truss’s term as prime minister, the result will be bitter medicine for people in the UK.

The BOE’s move is another sign that Britain, is moving further away from the US economically, with the prospect of a soft landing receding. BOE Governor Andrew Bailey struck a dovish note, warning that markets were pricing in too many rate rises for the UK. That marked a sharp contrast with Federal Reserve Chair Jerome Powell, who said Wednesday that US rates will probably go higher than people are thinking.

“The Fed was saying that markets were under-pricing the terminal rate,” said Charles Hepworth, investment director at GAM Investments. “The bank went in the opposite direction and said markets are over-pricing the terminal rate. This is entirely down to the fact that the UK economy is in a much weaker position than the US.”

Bailey has to strike a difficult balance. With inflation at a 40-year high of 10.1% -- five times the BOE’s target -- policy makers are signaling rates will have to rise further to prevent a wage-price spiral. But by pushing back on bets investors have made for rates to peak above 5%, he may help the Treasury stabilize the public finances.

Chancellor of the Exchequer Jeremy Hunt is seeking to fill a £50 billion gap in the government’s budget, and lower interest payments on the government’s burgeoning debt would make a big impact. Every 1 percentage point fall in short-term interest rate projections spares the government about £10 billion.

Ahead of Thursday’s decision, markets expected rates to peak at 4.75%. Bailey suggested in the Monetary Policy Report press conference that the level was too high. The path of rates is likely to be “nearer the constant path than the market rate path” with rates at 3%, he said.

The goal of both the BOE and Treasury is to limit the time that consumers and businesses suffer from high interest rates. After more than a decade of rates below 1%, the BOE has raised borrowing costs eight times since December to contain soaring inflation. That, combined with the market shock caused by Truss’s tax cuts, sent mortgage rates soaring over 6%.

Bailey said homeowners should see an easing in mortgage rates after recent spikes that threatened to add £3,000 a year to the cost of the average home loan.

“The rates on new fixed-term mortgages should not need to rise as they have done,” Bailey said. If traders were in any doubt about how they should respond, Deputy Governor Ben Broadbent spelled it out, adding that “the markets’ job is to follow us, not us to follow them.”

For Andy Burgess, fixed income investment specialist at Insight Investment, the BOE’s stance signaled a welcome return to the period before Truss’s disruptive 44 days as prime minister. In her tenure, she set fiscal and monetary policy against one another -- with one foot on the brake and the other on the accelerator, as the International Monetary Fund put it. The reverse is now happening, Burgess said.

“Taken at face value, a looser monetary policy and tighter fiscal policy seem to be on the cards,” Burgess said.

As bad as the BOE’s forecast seemed, the real picture may be worse. Sunak and Hunt are preparing a fiscal squeeze of around £35 billion on the economy on top of the monetary tightening announced Thursday. None of that was factored into the BOE’s forecasts. Broadbent said it is “likely that further rate rises will be necessary” as well.

What Bloomberg Economics Says ...

An important caveat to the MPC’s projections is that they don’t include the looming fiscal consolidation that is set to be announced by the government on Nov. 17. The scale, timing and, to a lesser extent, composition of that package of spending cuts and tax rises could have a material impact on how far the MPC lifts rates. All else being equal, tighter fiscal policy requires a looser stance from monetary policy.

--Dan Hanson and Ana Andrade, Bloomberg Economics. Click for the REACT.

Yet the BOE’s forecasts suggest rates may not need to rise much further -- if at all. Inflation is expected to peak at 10.9% this year but to be back at 2.16% -- almost bang on target -- in two years’ time assuming rates remain 3%.

The problem is that a weaker trajectory for interest rates weighs on the value of the pound, which continued to fall against the dollar on Thursday after the BOE decision. A weaker currency adds to the cost of imported goods and tends to push up inflation. Broadbent was unapologetic about sterling’s reaction.

“We are in a very, very different position than the US,” the deputy governor said, noting that higher energy prices are hitting Europe harder than the US.

Bailey indicated that having the BOE and Treasury work together will help bring confidence to markets, perhaps reducing the price investors charge to buy UK government debt that cropped up during Truss’s short tenure in office.

“There has been a UK premium on rates,” Bailey said. “There will be some lasting effect. We’ll have to work very hard to put that in the past.”