(Bloomberg) -- A shift in sentiment on Federal Reserve policy is emerging in interest-rate options, where several big wagers on the central bank’s benchmark rate reaching 6% — nearly a percentage point higher than the current consensus — have popped up this week.

The thinking behind them flies in the face of what has been an article of faith over the past two months: that the Fed, after raising rates eight times in the past year, is near the end of its tightening cycle. Already, rates are high enough to cause a recession that will require the central bank to reverse course this year, the thinking goes.

But strong January employment data released Friday challenged that thesis, and comments by Fed officials this week have eroded it further. Now, a pause after just one or two more rate hikes is not looking like such a done deal.

On Tuesday, a trader amassed a large position in options that would make $135 million if the central bank keeps tightening until September. Buying of the same structure continued Wednesday, alongside similar bets expressed in different ways.

Preliminary open-interest data from the Chicago Mercantile Exchange confirmed the $18 million wager placed Tuesday in Secured Overnight Financing Rate options set to expire in September, targeting a 6% benchmark rate. That’s almost a full percentage point more than the 5.1% level for that month currently priced into interest-rate swaps.

Buying of the position was ongoing throughout Tuesday’s session, though it ramped up significantly in the afternoon via block trades after Fed Chair Jerome Powell suggested the latest monthly jobs numbers may necessitate more tightening than previously anticipated. On Wednesday, more piled in.

Read More: Traders Keep Amassing Big Hawkish Fed Options Bet for Second Day

It’s the latest in a series of big wagers that show no signs of letting up even as the Fed has slowed down a tightening cycle that has been the fastest since the early 1980s. Last month, SOFR options bets made CME Group (NASDAQ:CME) history, recording the biggest inflows on record into any product traded on the exchange.

The trade would break even at a policy rate around 5.6%, and make $60 million should the Fed raise it to 5.8%, according to Bloomberg calculations. At the moment, overnight index swaps show the rate peaking around 5.19% in July.

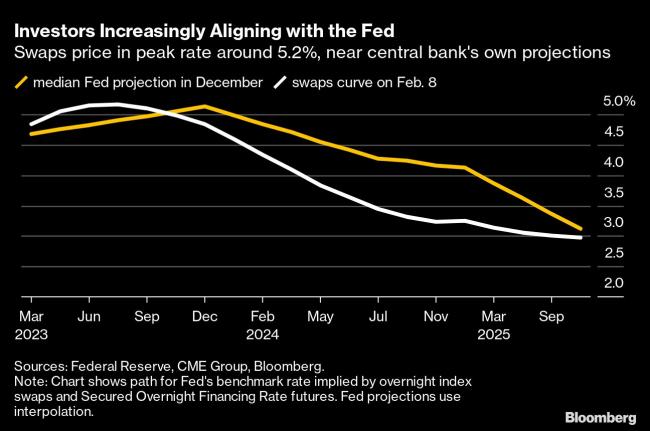

Investors are already looking ahead to what new interest-rate projections — the central bank’s so-called “dot plot,” to be published after its next policy meeting in March — may show, now that markets are aligned with the last set of projections published in December.

Several officials were set to speak Wednesday — including New York Fed President John Williams, who said during a Wall Street Journal event in the morning that the December outlook “still seems a very reasonable view of what we’ll need to do this year.”

Whether that view holds until March will depend on inflation data to be released between now and then, according to Jason England, a global bond portfolio manager at Janus Henderson Investors in Corona Del Mar, California.

“The market has come back in line with where the Fed is right now with their peak, terminal rate. The question is: Do they revise the dots up?” England said.