(Bloomberg) -- The dollar’s rise over the past year is leaving some emerging markets increasingly exposed to capital outflow. The most vulnerable are beginning to falter, sending a warning signal to EM as whole.

In a dollar-based system, countries have dollar liabilities but local-currency assets. When the US currency rises, it eventually puts intolerable strain on national balance sheets, weighs on the local currency, stokes inflation pressures and squeezes domestic growth. Just when such countries are in need of capital, higher US yields act as a magnet for international flows, sucking capital away from them.

EMs are the weakest hands. Often being unable to issue credit in their own currency leads to the “original sin” of borrowing in a hard currency, mainly the dollar. Such transgressions have been wildly popular in recent years, with the amount of cross-border dollar-denominated credit outstanding in EMs rising fourfold since 2006 to over $4 trillion.

EM capital outflow has been relatively contained so far, but the pressure is mounting as US yields are at over decade highs, while the dollar is the strongest in 20 years. This is tightening global liquidity, which points to EM capital outflow accelerating.

Reserves are the first line of defense when a country’s capital flow situation becomes fragile. But not all EMs are equally at risk.

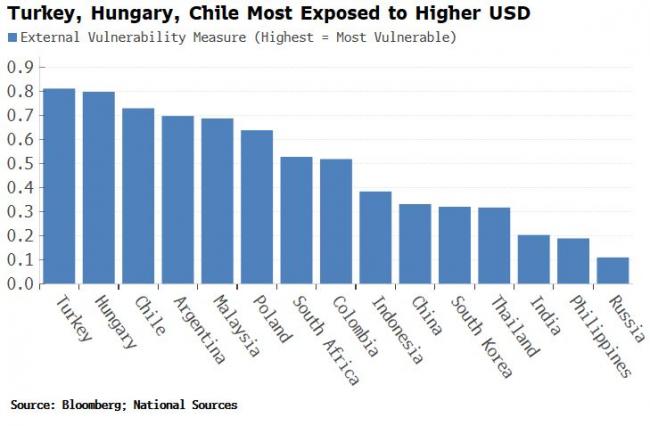

I created an External Vulnerability Measure based on the IMF’s reserve adequacy score. This version has three inputs: reserve adequacy with respect to exports, short-term debt (the latter is the Greenspan-Guidotti ratio), and the current account.

The measure has Turkey, Chile, Hungary and Argentina as the most vulnerable to capital outflow.

Nevertheless, Turkey and Chile have seen the highest equity returns so far this year (even in USD terms).

This might seem paradoxical, but Chile and especially Turkey have among the highest and fastest rising levels of inflation. Equities are generally seen as an inflation hedge (an erroneous assumption to make, certainly in DM markets) -- leading to supportive flows.

This has certainly been the case in Turkey where President Erdogan has favored rate decreases as the response to inflation now running at over 80%. With bond yields stuck around the 10% mark, the 100%-150% returns on offer on the stock market are almost irresistible.

Now both equity markets are facing rising headwinds. There are reasons specific to each country that might explain this -- a rout in Turkish bank stocks, political and social unrest in Chile.

But both countries are facing an increasingly intolerable reversal in capital flows, compounded by rising energy prices and, in Chile’s case, falling copper prices.

As two of the very few EM or DM equity markets with a positive YTD return, their recent travails are a harbinger for other EMs, principally those highly reliant on foreign financing and a stronger dollar.

- NOTE: Simon White is a macro strategist for Bloomberg’s Markets Live blog. The observations he makes are his own and not intended as investment advice. For more markets commentary, see the MLIV blog

©2022 Bloomberg L.P.