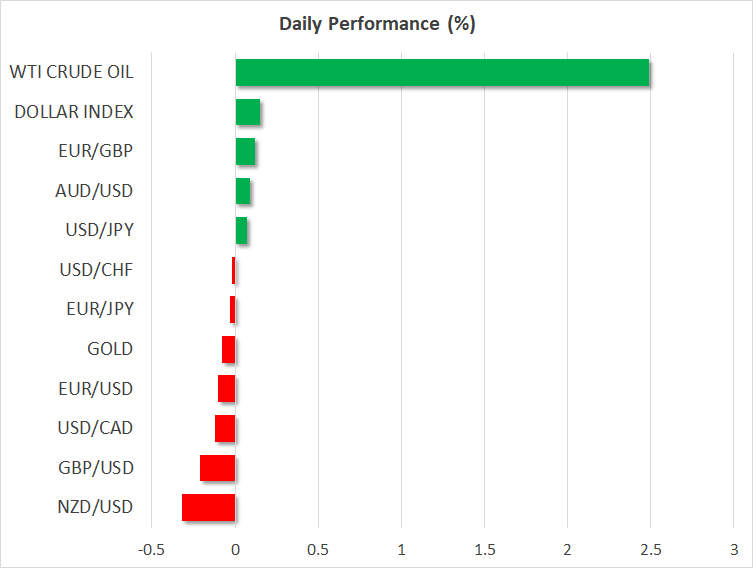

- Japanese yen charges higher on rate hike speculation

- Dollar turns to US employment report - downside risks?

- Stock markets climb as Google (NASDAQ:GOOGL) rekindles AI euphoria

Yen takes the elevator up

The Japanese yen blasted higher on Thursday, gaining 2% against the US dollar after the Governor of the Bank of Japan provided the clearest indications yet that the era of negative interest rates is about to end.

Speaking before parliament, Governor Ueda said that calibrating monetary policy will become “more challenging” heading into next year, adding that his central bank has several options about which policy rates to target once it exits negative interest rates.

His comments lit a fire under the Japanese yen, as traders ramped up bets that the Bank of Japan will be the sole central bank to raise rates next year, flying against a global rate cutting cycle. Market pricing suggests the BoJ will exit negative rates by April, after it evaluates the outcome of the spring wage negotiations.

Beyond FX markets, options traders have also joined the bandwagon of betting on a stronger yen, something reflected in the sharp spike in the implied volatility of USD/JPY options. The yen was up almost 4% against the dollar at one point yesterday, but the advance was halted near the 200-day moving average and the currency ultimately trimmed its gains in half.

All told, the stage seems set for the yen to shine in 2024 as the forces that devastated the currency over the last couple of years go into reverse, with interest rate differentials narrowing once again and lower energy prices supporting the yen through the trade channel. The latest surge may have been the opening act of the yen’s long-awaited trend reversal.

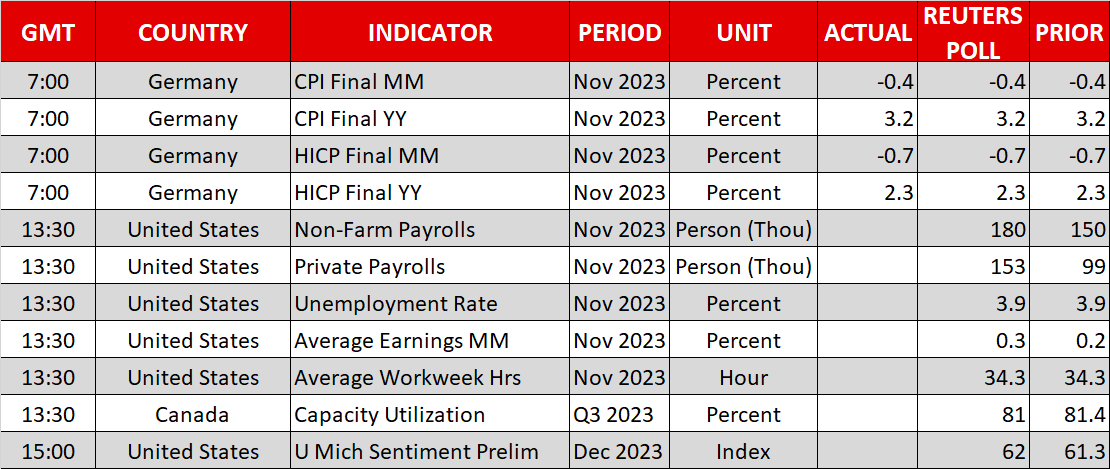

Nonfarm payrolls - disappointment on the cards?

As for today, all eyes will fall on the latest US employment report. Nonfarm payrolls are projected to have risen by 180k in November, more than the 150k last month, while the unemployment rate is seen steady at 3.9%. Meanwhile, wage growth is expected to have lost some steam on an annual basis.

In terms of any potential surprises, the tea leaves point to a disappointment in this employment report, following a streak of underwhelming labor market indicators. Business surveys such as the S&P Global composite PMI signaled the weakest increase in employment since mid-2020, as firms cut back on hiring in an attempt to control costs. Similarly, the ADP report was softer than expected.

That said, the fact that jobless claims remain historically low suggests there were no signs of mass layoffs in the US economy either, limiting the scope for disappointment today. Therefore, the early evidence is consistent with a labor market that is cooling off, although employers are not firing people yet, they are simply hiring less.

An employment report that falls short of forecasts today could reinforce bets of heavy rate cuts by the Fed next year, and by extension inflict some damage on the dollar. Nonetheless, the dollar’s broader trajectory might be decided by next week’s events, which include an inflation report and a Fed policy decision.

Stocks jump, Google leads the way

Shares on Wall Street resumed their AI-powered rally on Thursday, with the tech generals leading the charge after Google unveiled its latest artificial intelligence model, propelling its stock price more than 5% higher.

In general, stock markets are currently priced for perfection. Valuations are stretched and earnings assumptions seem overly optimistic heading into a global economic slowdown next year and a US presidential election that historically dampens market performance in the lead-up. The risk/reward profile for equities does not seem very attractive here.