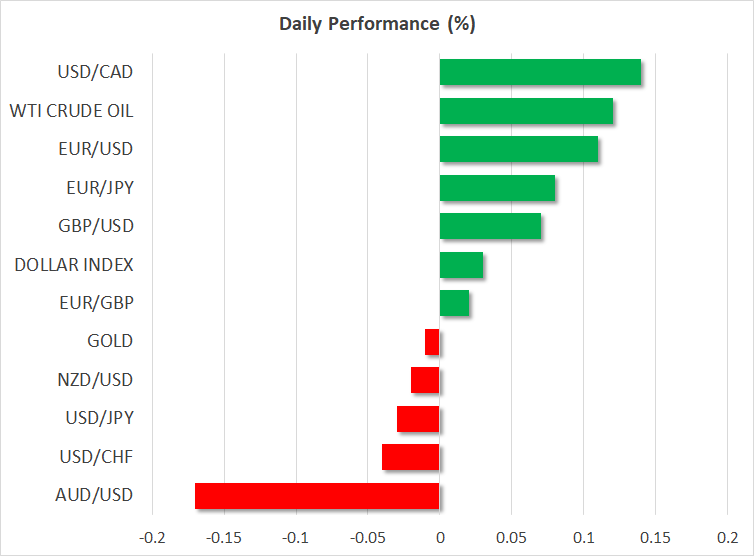

- Yen spikes, but ends Monday as the main loser

- Dollar traders lock gaze on US inflation data

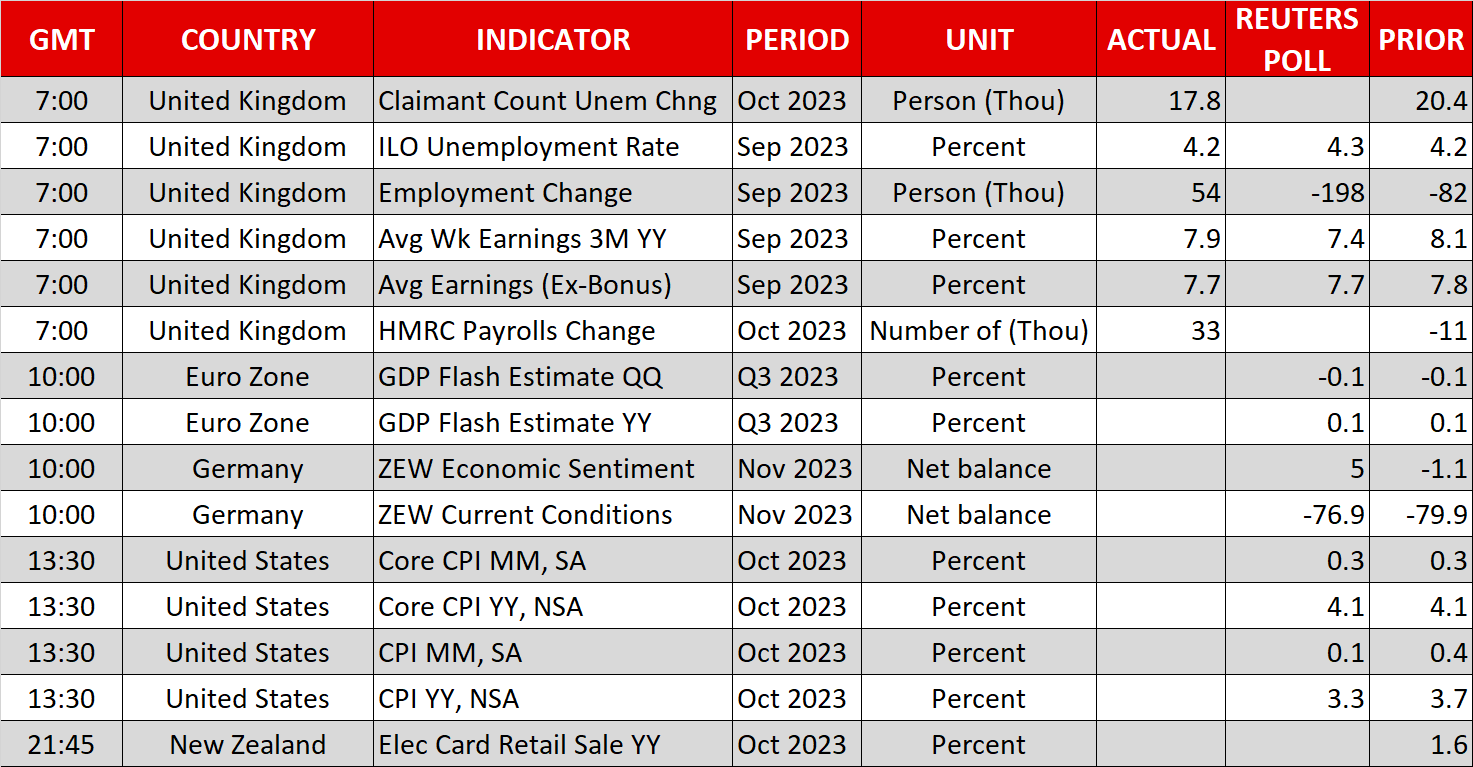

- UK jobs report beats estimates, CPIs the pound’s next test

- Wall Street ends mixed, awaits US CPI figures

Dollar/yen nearly touches October 2022 high

The US dollar traded mixed against its major counterparts on Monday, losing ground against the pound, the aussie, and the euro, while gaining the most against the yen.

Dollar/yen continued drifting north during most of the day, almost touching the October 2022 high of 151.94, the test of which back then invited Japanese authorities to intervene. That said, after testing 151.90 yesterday, the pair slumped around 70 pips without any clear trigger, before recovering a large portion of the slide later in the day.

Although some participants may have thought that this was the result of an intervening hand, there is no credible confirmation of this. It is more likely that the slide was the result of $1.3bn worth of options expiring yesterday with a strike price at around 152.00. More options with the same strike price are due to expire between Wednesday and Friday. It could also be that traders had take-profit or short-selling orders placed near those levels on fears of intervention.

Overall, option strike prices could continue acting as resistance should the pair break 151.94 and form a new 32-year high, but the wide interest-rate differentials between Japan and the rest of the world are likely to continue weighing on the yen. Even if Japanese authorities decide to step in, as long as the BoJ is phasing out its yield curve control (YCC) in piecemeal steps and occasionally stepping into the bond market to keep long-dated yields below 1%, the dollar/yen uptrend may be destined to continue.

A trend reversal may be a story for 2024, when the BoJ abandons its YCC policy and other central banks keep rates steady, with some of them examining the case of rate reductions at some point during the year.

Can US CPI data convince investors about one more Fed hike?

Today, dollar traders are likely to lock their gaze on the US CPI data for October as they try to figure out the path of interest rates moving forward. Recently, Fed Chair Powell and his colleagues pushed against expectations that they are done with raising interest rates, but investors remained largely convinced that the end credits of this tightening crusade have already rolled. They are assigning only a 30% probability for another quarter-point hike by January, while penciling in around 80bps worth of rate reductions by the end of next year.

The headline CPI rate is expected to have pulled back to 3.3% y/y from 3.7%, which appears to be a sound projection given the slide in oil prices during October, while the core rate is forecast to have held steady at 4.1%. That said, bearing in mind that the S&P Global PMIs suggested softer price pressures, a lower core rate cannot be ruled out. Therefore, softer-than-expected inflation could add credence to the market’s belief of no more hikes and several cuts for next year and perhaps hurt the dollar.

Will UK CPI data help the pound recover more?

The pound was yesterday’s main gainer and continued marching north today after the UK employment data for September largely beat expectations, with the unemployment rate holding steady instead of rising, and average weekly earnings including bonuses slowing by less than forecast.

The numbers corroborate comments by BoE Governor Bailey after the latest policy meeting that it is too early to discuss rate cuts, but traders are still pricing in around 65bps worth of rate reductions for next year. Perhaps they are saving some ammunition for tomorrow’s UK inflation data for October. Both the headline and core CPI rates are expected to have slowed but with the UK PMIs for the month revealing that prices charged by companies accelerated to a three-month high, the risks may be tilted to the upside. In other words, even if UK inflation slows, it could slow by less than expected.

This, combined with cooler US inflation today, could help Cable return above the key barrier of 1.2310 and perhaps challenge its 200-day moving average.

Wall Street takes a breather ahead of CPI data

Wall Street traded mixed on Monday, with the Dow Jones gaining some additional ground, but the S&P 500 and the Nasdaq pulling somewhat back. It seems that following Friday’s rally, equity investors are taking a breather ahead of today’s US CPI figures.

Stock traders could decide to increase their risk exposure if indeed the results point to cooler-than-expected inflation, as this will add to expectations that Fed hikes are over and that several rate cuts may be warranted next year. The opposite could be true in the case of inflation proving stickier than expected. With equities already gaining decent ground ahead of the release, and with the risks surrounding the data being tilted to the downside, an upside surprise may result in a substantial setback.