- Bank of Japan adjusts yield curve control policy again, but yen skids

- Yields edge lower after Treasury Department says will borrow less in Q4

- Dollar mixed, euro extends gains, stocks perk up

Yen not impressed by BoJ’s incremental move

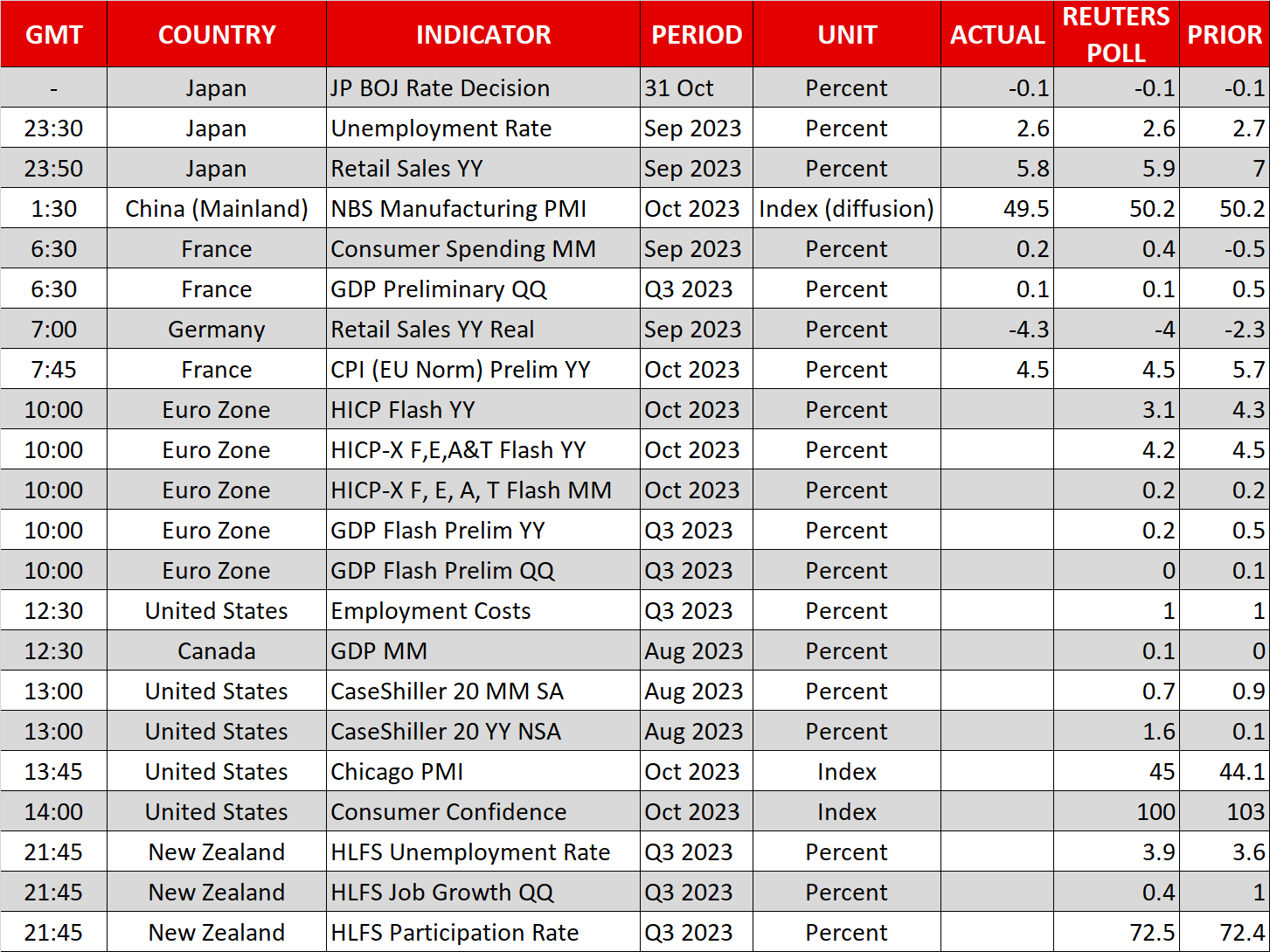

The Bank of Japan took another step towards policy normalization on Tuesday, tweaking its yield curve control policy (YCC) for the second time this year amid signs of broadening inflationary pressures. As expected, the Bank upped its inflation forecasts for the next three fiscal years, with those for 2023 and 2024 seen above 2.0%.

This prompted policymakers to make a further adjustment to their YCC policy, raising the reference point for targeting the 10-year JGB yield from 0.50% to 1.0%. However, the BoJ did not specify a new upper bound, suggesting that it will intervene in the bond market at its discretion whenever the 10-year yield exceeds 1.0%, effectively removing the hard cap.

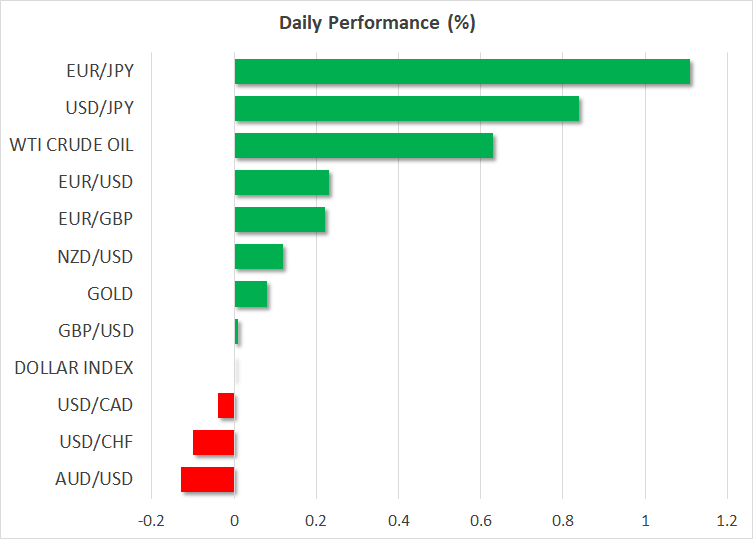

With investors already anticipating some kind of a policy change, there was a sense of disappointment that today’s decision was just another minor tweak. The yen plummeted against the US dollar, which jumped back above the 150 level. Speculation in the run up to the meeting had driven the yen to a two-and-a-half-week high of 148.79 per dollar on Monday. The yen suffered even bigger losses against other majors such as the euro.

There is a danger, though, that markets are missing the bigger picture with today’s announcement by not appreciating the significance of the upper hard cap being abandoned. The fact that the BoJ continues to maintain an easing bias is a major drag on the currency, but there are plenty of subtle hints that Governor Ueda is steering policy towards an eventual exit from stimulus.

Yet, a bolder policy shift is unlikely to come before the 2024 spring wage negotiations as Ueda is pinning his hopes on big wage hikes next year to boost inflation sustainably. So until then, traders may not be too convinced by the BoJ’s incremental policy adjustments.

Dollar weighed by softer US yields as euro climbs

The dollar was either flat or down against its other rivals on Tuesday, as Treasury yields headed lower. There was relief yesterday when the US Treasury said it will borrow less in the fourth quarter than it did in the previous quarter. However, borrowing is expected to rise again in the first quarter of 2024 so the relief on yields might only be temporary.

The 10-year Treasury yield eased to one-week lows today and last stood at 4.835%, while Japan’s 10-year yield jumped to a new 10-year high of 0.962%, making today’s moves in dollar/yen all the more surprising.

The euro was one of the strongest performers today, hitting a high of $1.067 before easing slightly after Eurozone GDP data missed expectations. The Eurozone economy contracted 0.1% in the third quarter according to the flash reading against estimates of flat growth. The flash CPI print also came in below forecasts, falling to 2.9% in October from 4.3% previously.

Softer CPI data might actually be aiding the euro as it would allow the ECB to cut rates sooner rather than later, thereby reducing the odds of a severe downturn.

The pound was modestly higher as traders awaited the Bank of England’s policy decision on Thursday, while the Australian dollar came under pressure following an unexpected drop in China’s manufacturing PMI for October.

Gold consolidates despite ongoing Mideast tensions

Gold prices were attempting to reclaim the $2,000/oz level on Tuesday after failing to close above it yesterday. As the war in Gaza rages on, there are few indications that a major escalation is imminent, even as the situation remains highly volatile. Israel’s prime minister, Benjamin Netanyahu, has ruled out a ceasefire, saying that “this is a time for war”.

Nevertheless, the precious metal appears to be consolidating this week, while the improved risk sentiment is lifting oil prices slightly after sliding sharply yesterday.

European equities extended this week’s recovery, lifted by gains of more than 1% on Wall Street, although shares in Asia were mixed, with Chinese indices closing lower on the back of the weaker-than-expected manufacturing PMI.