- Dollar’s recovery pauses after NFP and ISM data

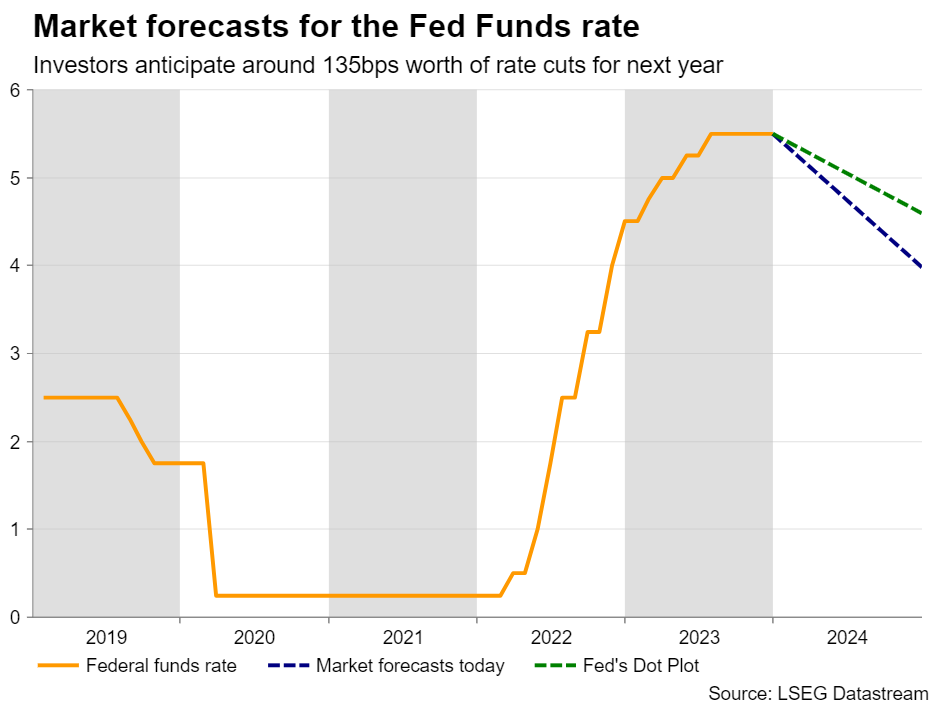

- Investors continue to price in aggressive rate cuts by the Fed

- Attention now turns to CPI inflation on Thursday, at 13:30 GMT

- Will the dollar resume its upside trajectory?

The dollar entered the new year on a strong footing, but soon after the US jobs data was out, its march north came to a halt. The world’s reserve currency extended its rally at the time the better-than-expected headline numbers were out, but after digging into the details of the report, they abandoned their long dollar positions as the story was not as exciting as they initially thought.

The December payrolls may have well beat the consensus, but the October and November numbers were revised down by a combined 71k. On top of that, although the unemployment rate held steady and did not rise as anticipated, the labor force participation rate slid, which means that fewer unemployed Americans are encouraged to start actively looking for a job.

What pushed the greenback even lower was the ISM non-manufacturing PMI for the same month, which fell to the lowest reading since May. More importantly, the survey’s employment sub-index tumbled from 50.7 to 43.3, the lowest since July 2020, when the globe had to deal with the first wave of the coronavirus pandemic.

Investors still see a decent chance for a March rate cut

All these economic numbers allowed market participants to maintain bets of aggressive rate cuts by the Fed, and a nearly 70% probability that the first quarter-point reduction will be delivered in March, despite the Fed pointing to much fewer reductions through its December dot plot and the minutes of that meeting revealing that most policymakers wanted to keep borrowing costs high “for some time.”

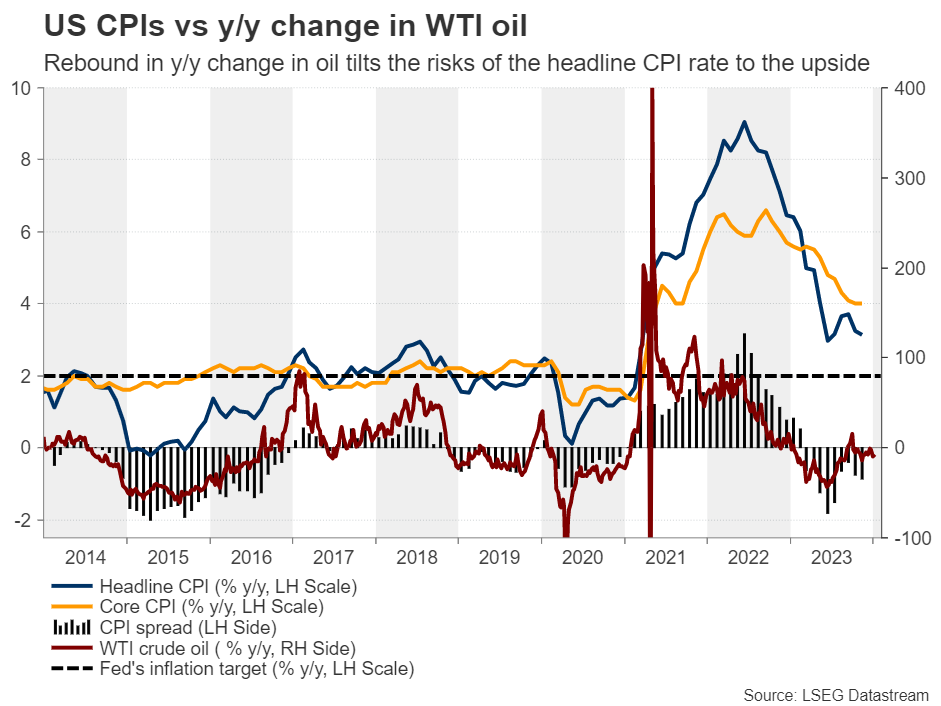

Base effects suggest a rebound in headline inflation

Now, the next release that will lock dollar traders in front of their screens will most likely be the US CPI numbers for December, due out on Thursday. Inflation has come down quickly in recent months due to weaker goods prices and moderating costs of services, including travel, even as rent increases remained elevated. Headline inflation saw a faster slowdown than underlying price pressures as energy prices began drifting south in September, erasing nearly all the gains posted during the summer months.

However, with the 2022 downtrend now dropping out of the year-on-year calculation, oil prices are close to their opening levels for 2023, which means that the y/y change has moved from well into negative territory close to zero. And with the headline CPI rate resting well below the core one, even if the latter softens a bit more, this means that there are risks for a rebound in headline inflation. Indeed, the forecasts support this logic. Although the core rate is expected to have declined to 3.8% y/y from 4.0%, the headline one is seen ticking up to 3.2% y/y from 3.1%.

Will a higher CPI recharge the greenback’s engines?

Ergo, a rebound in the headline CPI rate and a core one still nearly double the Fed’s objective may convince investors to push back their bets regarding a March rate reduction, even if they don’t materially reduce the total amount of basis points expected to be cut by the end of the year. This could allow the dollar to rebound as Treasury yields continue to recover.

From a technical standpoint, the dollar’s comeback at the turn of the year has resulted in a strong downside correction in aussie/dollar, and a rebound in US inflation may allow that retreat to continue for a while longer. However, with the price structure still pointing to higher highs and higher lows above the uptrend line drawn from the low of October 26, and with the RBA expected to cut interest rates by only 40bps by the end of the year, calling for a bearish reversal in this exchange rate may be unwise and premature.

If the setback continues, the bulls may find the 0.6570 zone an attractive entry point for resuming the prevailing near-term uptrend. However, in case the CPI figures miss their forecasts, the correction may come to an end sooner as the bulls become willing to jump into the game at even higher levels.