Comfort is often the worst enemy of the economy. Recall the Dotcom Bubble in 2001, which threw most investors off after a sustained bull run in tech stocks. In the same century, the world was hit with the Great Recession, which followed after great complacency in the housing market. Most recently, we felt the impact of the Covid-19 recession, when most believed that such worldwide pandemics were a thing of the past.

Today, we see renewed faith in the U.S. economy. After a strong recovery from the Covid-19 crash, and the Fed's predicted rate cuts, most believe that a soft landing is around the corner. In more layman terms, many investors believe we are 'out of the woods' and ready for the market to reach new highs. In my opinion, there are still a few glaring issues before we can come to such a conclusion — one of them being the American debt situation.

From 1970 to 2010, the debt situation has been relatively under control. Nominal GDP far exceeded national debt, which was well under the debt ceiling.

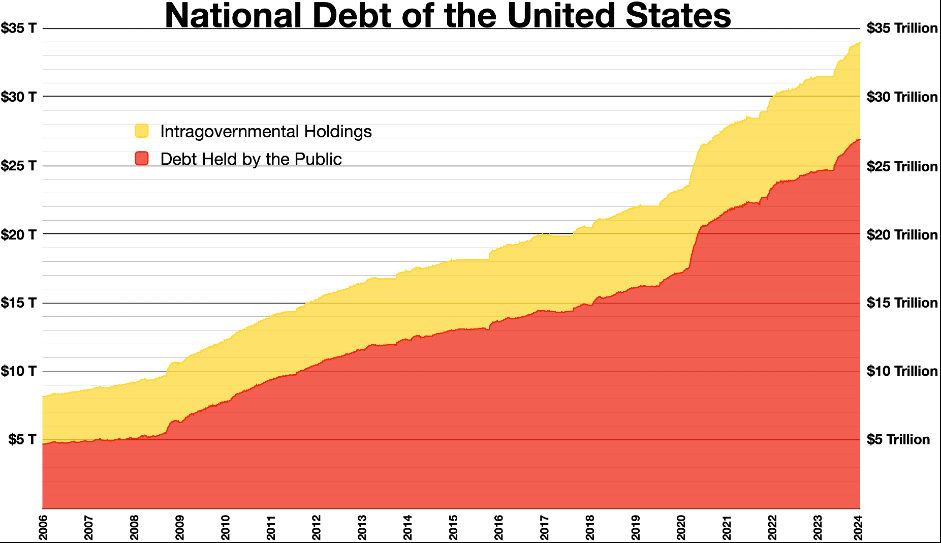

However, things have clearly taken a turn for the worse. In 2011, Standard & Poor downgraded the long-term credit rating of the U.S. federal government from AAA to AA+. We've seen the Congress suspend the debt ceiling 7 times since 2013. Debt-to-GDP ratio has been increasing at alarming rates, reaching levels of about 129% during the Covid-19 recession. There seems to be no sign of cooling when it comes to government expenditure, and national debt has piled up to over $34 trillion. )

)

About 80% of this debt is held by the public — with key holders being corporations, individuals, and of course, the Federal Reserve. We're often more concerned with Federal Debt Held by the Public, which shows how much is borrowed by the U.S. Treasury from outsiders to meet the government's objectives for the country's economy.

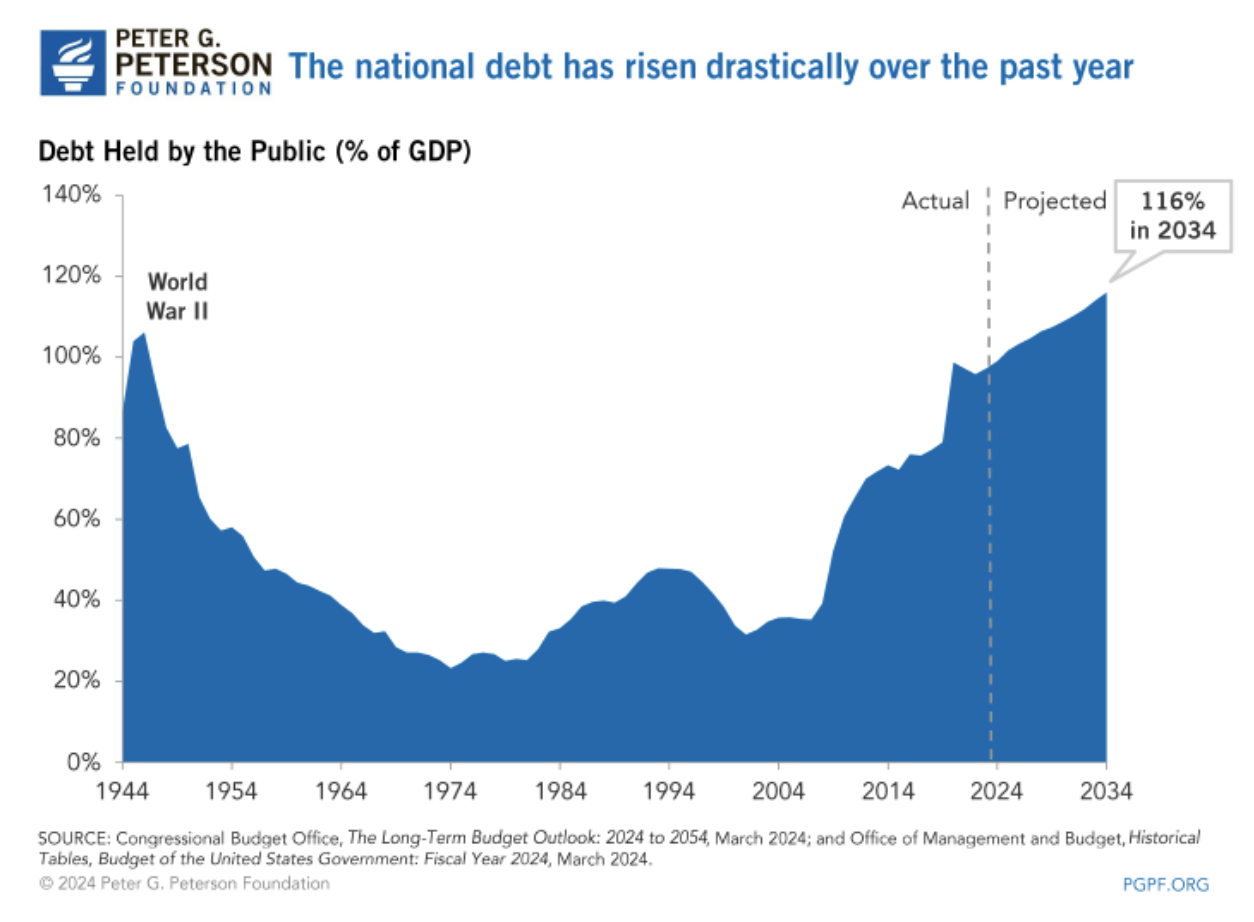

As we observe the Debt Held by the Public as a percentage of GDP, we see a concerning U-shaped trend from the mid 1900s to the present, and this metric is projected to be a concerning 116% in 2034. The ratio is often a decent barometer of the U.S.'s ability to fulfil these obligations, and projections are generally pessimistic.

Economic experts have expressed concern over the matter. According to the Council on Foreign Relations, Goldman Sachs economists predict that a default on debt would cease at least 10% of American economic activity. Current Treasury Secretary and former Federal Reserve Chair Janet Yellen adds that the economic impact of a default would be irreversible, sending seismic effects across global markets and the living standards of Americans.

Indeed, a default on debt would create major domino effects in the economy. Further downgrades in credit ratings would cause interest rates to skyrocket. Consumption would contract due to increased borrowing cost and loss in consumer confidence. The U.S. dollar's position as the world's reserve currency would also be threatened with the potential dumping of treasuries due to decreased credit-worthiness. A depreciation of the dollar would largely impact global markets, as over 50% of global foreign currency reserves are in U.S. dollars. The debt issue could escalate to a global recession if not dealt with in the near future.

No amount of easing or government intervention seems to be sufficiently adequate in solving the American debt situation at the current moment, which is why I remain pessimistic in this, otherwise, rejuvenated economy.