Recently I was asked a question that I suspect has been on many investors’ minds. Here’s the question: “Is it possible that the bond market will be the market to tumble into 2014, and as it does, the general market decline is mitigated by the rotation of money out of bonds and into stocks?”

Here’s my answer: Anything is possible in today's upside-down world. As my late friend and mentor Bud Kress used to ask, “Does anything surprise you anymore?” But I’d have to say here -- and I firmly believe Bud would echo this sentiment -- if there’s any validity to the 120-year Kress cycle, a sustainable rising interest rate trend isn’t likely until after October 2014.

The 120-year Mega Cycle -- and its 40-year and 60-year components -- is deflationary whenever they’re in the “hard down” phase, as they are between now and then. I make no claims to being an expert in bonds, but isn’t the scenario described above (viz. rising rates) essentially part-and-parcel of an inflationary environment? With deflation still making its presence felt in the global economy, I can’t see rising interest rates on a sustained basis until after 2014.

Deflation

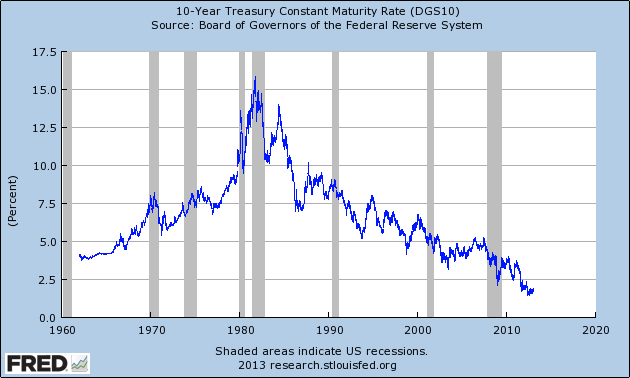

Structural deflation is chiefly characterized by three things: 1.) falling wages, 2.) falling interest rates, 3.) falling money velocity. One of the best illustrations of the deflationary long-term cycle can be seen in the graph of the 10-year Treasury rate shown here.

Note the peak in the interest rate in the early 1980s -- exactly when the 60-year Kress cycle of inflation/deflation peaked. The next scheduled bottom of the 60-year cycle is for late 2014. To date, long-term interest rates have conformed to the deflationary implication of this cycle as you can see in the above graph.

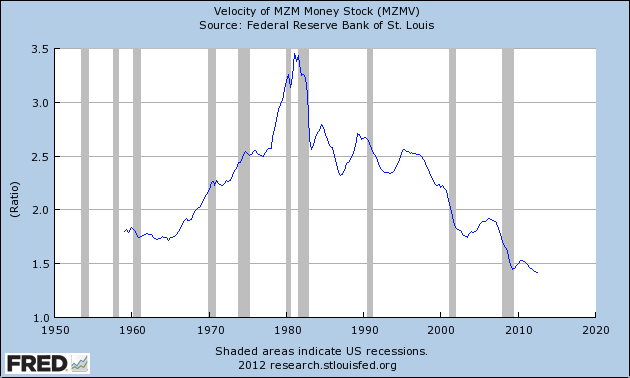

Velocity

Money velocity (that is, the turnover in money within the domestic economy) also peaked around 1980 and has been declining ever since.

Look To 2007

On a short-to-intermediate-term basis it may be possible to see rising interest rates, much as we did in 2007. That was, you may recall, an extremely volatile year and a precursor to the credit crisis of 2008. I strongly suspect 2013 will in some ways mirror 2007. In 2007, Treasury rates rallied in the first half of the year before collapsing heading into the hyper-deflationary year 2008.

Note the firmly established long-term downtrend channel in the interest rate below. Rates have recently fallen below the lower boundary of the channel, which constitutes a “channel buster.” This in turn suggests an “oversold” condition and therefore suggests that rates could rise in the near term to recovery temporarily back inside the channel. I don’t expect the rally (assuming it materializes) to persist for more than a few months.

Now the big question is what happens to all those hundreds of billions of dollars created in recent years -- the record corporate cash pile, bank reserves, etc. -- AFTER 2014? It doesn’t take much imagination to foresee a period of hyper-inflation being stoked once the downside pressure of the 120-year cycle is lifted. Unless I miss my guess, it will be in 2015 and thereafter when we’ll see rising interest rates and the corresponding long-term collapse in bond prices.

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money supply and bank credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving cycles, internal momentum and moving average systems, as well as investor sentiment. He is also the author of numerous books, including most recently “2014: America’s Date With Destiny.” For more information visit www.clifdroke.com.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

When Will Interest Rates Rise?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.