This week’s calendar appears lighter than last week’s, but investors’ eyes will continue being locked on the developments surrounding Ukraine. Besides that, the most important items on the agenda for this week are speeches by ECB President Lagarde and Fed Chair Powell, as well as the UK CPIs for February, the preliminary PMIs for March from the Eurozone, the UK and the US, as well as the SNB monetary policy decision.

On Monday, there are no top tier data releases on the agenda, but we have speeches from ECB President Christine Lagarde and Fed Chair Jerome Powell. Getting the ball rolling with Lagarde, at the latest ECB gathering, she and her colleagues decided to end their APP program in Q3, without hinting that any interest-rate hikes will be delayed due to the war in Ukraine. Lagarde said that the risks to the economic outlook have increased substantially, but she also added that inflation could be considerably higher than forecast.

In our view, this suggests that she believes the risk of high inflation outweighs concerns over how geopolitics could affect economic growth. However, this was 10 days ago, and with the war in Ukraine still raging, it will be interesting to hear what she has to say now. Even if she reiterates a similar message to the one we got from the latest ECB decision, expectations around the Bank’s future plans could well be altered by the Euro-area PMIs scheduled to be released on Thursday.

Now, passing the ball to Fed Chair Jerome Powell, we expect him to reiterate the hawkish message we got at the latest FOMC gathering. After all, the meeting took place just last week, and we don’t believe that Powell will deviate from that view so quickly. Remember that the Committee decided to lift interest rates by 25bps, while the new dot plot pointed to 6 more liftoffs by the end of the year. At the press conference following the decision, Powell himself said that the economy is strong enough to weather those rate hikes, while maintaining strong hiring and wage growth, adding that if they conclude that it would be appropriate to move more quickly to remove accommodation, then they will do so.

On Tuesday, we will get to hear from more Fed officials. Having in mind that as group, they anticipated 6 more quarter-point rate hikes by the end of the year, it will be interesting to hear some individual views, so we can put faces to some of the dots on the updated rate-projections plot. This could help us have a clearer picture on how the Fed’s plans may be affected in case someone changes their mind in the future.

Besides speeches by monetary policy officials, we will continue monitoring developments surrounding the war in Ukraine. Remember that last week, we got headlines that there has been some progress in the negotiations between Russian and Ukrainian diplomats, but with both sides adding that they are still far apart.

Today, Ukraine rejected Russian calls to surrender the port city of Mariupol in exchange for safe passage out of the city, and it remains to be seen how this will affect diplomacy efforts moving forwards.

With regards to the financial markets, most equity indices remained supported on Friday, with Asia pulling back only slightly today, despite the fact that the war is still raging. Maybe some participants remain optimistic that some further progress could be made given the willingness of both sides to continue negotiating, or maybe they believe that no other nation will need to get involved militarily, and that a conflict at a two-nation level has been already priced in.

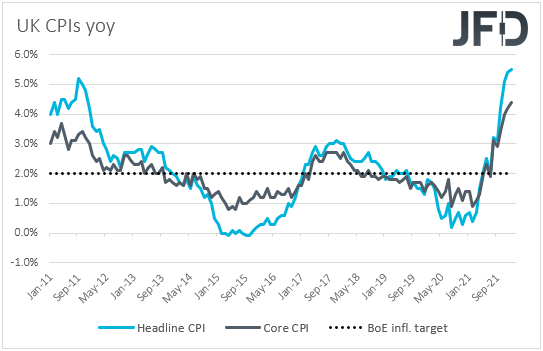

On Wednesday, during the early European morning, we get the UK CPIs for February, with both the headline and core rates expected to have continued rising. Specifically, the headline rate is forecast to have inched up to +5.9% yoy from +5.5%, while the core one is forecast to have risen to +4.8% yoy from +4.4%.

At last week’s meeting, BoE officials decided to hike interest rates by another 25bps via an 8-1 voting, with the dissenter calling for no increase at all. Remember that at the February gathering, officials lifted rates by 25 bps as well, but the vote was 5-4, with the dissenters calling for a 50bps increase. Compared to that, last week’s decision reveals a more cautious approach by policymakers and raises questions as to whether they will indeed proceed as aggressive as the market has been pricing in heading into the gathering.

That said, accelerating inflation further above the Bank’s target of 2%, could revive expectations that the Bank may need to act more quickly, something that could prove supportive for the pound.

The pound could receive extra support by Chancellor Rishi Sunak on Wednesday, as, when making his Spring Budget Statement, he could announce more measures to help households and small businesses in the midst of surging fuel and other prices.

As for the rest of Wednesday’s data, the only worth mentioning is the US new home sales for February, with the forecast pointing to a small increase compared to January.

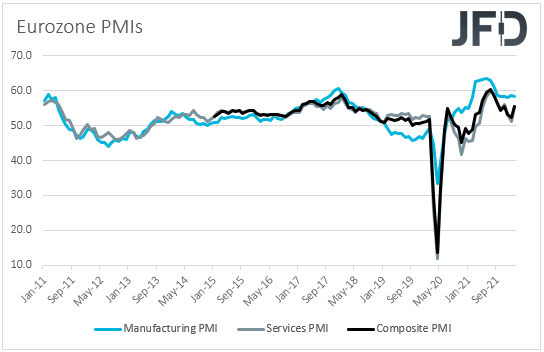

On Thursday, the spotlight is likely to fall on the preliminary Markit PMIs for March. We get the manufacturing, services and composite indices from the Eurozone, the UK and the US, and they may provide a first glimpse as to how those major economies have been affected by the war in Ukraine.

Expectations are for small declines in all indices, but we see the case for negative surprises as more likely in the EU and UK indices. Big disappointments could raise questions again as to whether the ECB and the BoE should prioritize stopping accelerating inflation instead of supporting economic growth. This could add selling pressure to the euro and the pound, while the opposite may be true in case the numbers come close or above their forecasts.

We also have a central bank deciding on monetary policy on Thursday, and this is the SNB. Although inflation in Switzerland is slightly above 2%, at +2.2% yoy specifically, that rate is well behind other major economies, like the Eurozone, the UK, and the US, and thus, we don’t believe that Swiss policymakers will signal willingness to lift interest rates soon.

Also, with the EUR/CHF staying in a downtrend mode since January last year, despite the latest recovery started on Mar. 8, we believe that officials will maintain extra-loose monetary policy, reiterating their willingness to intervene in the FX market if deemed necessary.

Finally, on Friday, the main items on the agenda are the UK retail sales for February, and the German Ifo survey for March. In the UK, both the headline and core sales are forecast to have slowed, to +0.8% mom and +1.0% mom, from +1.9% and +1.7% respectively, while in Germany, both the current assessment and expectations indices are forecast to decline, taking the business climate one down to 94.0 from 98.9.