The dollar show

The US dollar rally went into overdrive this week, leaving a trail of destruction across the FX market. Concerns that the global economy is sleepwalking into a recession as interest rates are raised at full speed and government spending is rolled back are pushing nervous investors into the safety of the reserve currency.

Meanwhile, every other major currency has been dismantled. The euro has been demolished by the energy crisis, which has deprived it of its main weapon - an enormous trade surplus. The yen has been devastated by the Bank of Japan’s refusal to consider higher rates, while the British pound has transformed into a mirror image of stormy stock markets.

Admittedly, it’s been a case of ‘all news is good news’ for the dollar lately. When markets worry about runaway inflation, Fed tightening bets gain momentum and higher Treasury yields propel the dollar higher. And when traders panic about a recession, safe-haven flows eclipse everything else.

There are two elements that can change this dynamic - either more energy supply comes back online and lower prices provide relief to the euro and yen, or US inflation cools down and the Fed can take its foot off the brakes. This puts even more emphasis on the upcoming data on Wednesday.

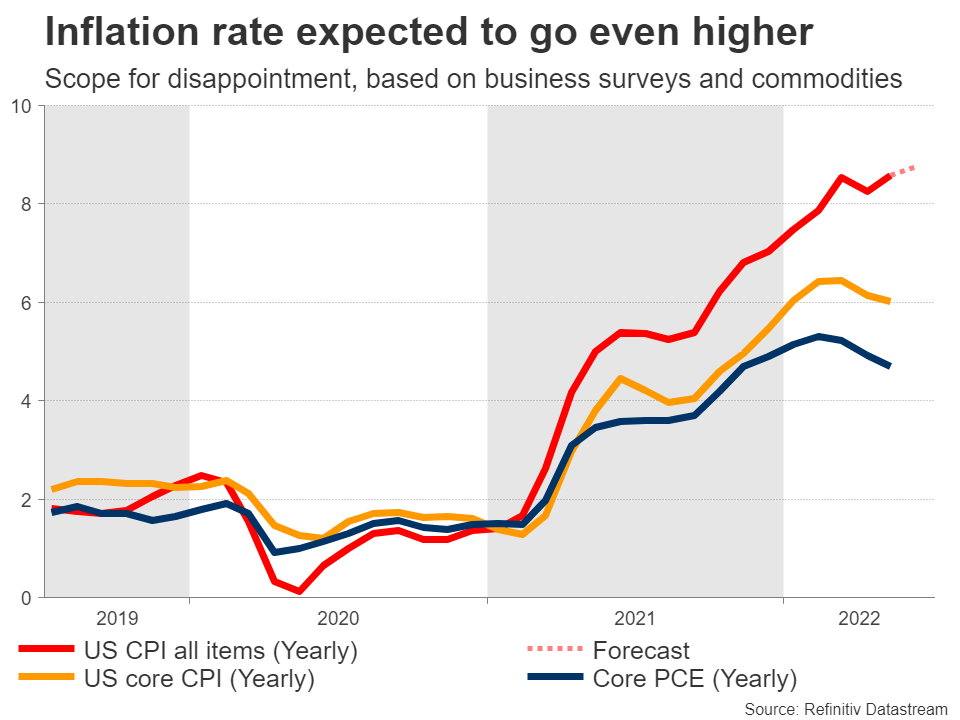

Inflation as measured by the CPI is anticipated to have risen to 8.7% in June from 8.6% previously. However, there is scope for a softer number considering business surveys like the S&P Global PMI, which showed that companies raised their selling prices at the slowest pace in almost a year. The rollover in commodity prices adds credence to this view.

Retail sales for the same month are out on Friday and although they are expected to have bounced back in monthly terms, it is the yearly rate that tells the story. It stands at 8.1%, below the inflation rate, indicating that real consumption has been steamrolled by the cost of living crisis.

BoC - In the Fed’s shadow

In neighboring Canada, the central bank is expected to copy the Fed and raise interest rates by 75 basis points on Wednesday. The move is almost fully priced into money markets, following a string of encouraging labor market data and the BoC’s own business survey that reflected mounting inflation worries.

Since the rate hike is essentially a done deal, the market reaction will mostly boil down to the tone of the press conference and the updated economic forecasts. A rate hike of equal size is already priced in for September, so the stakes are high.

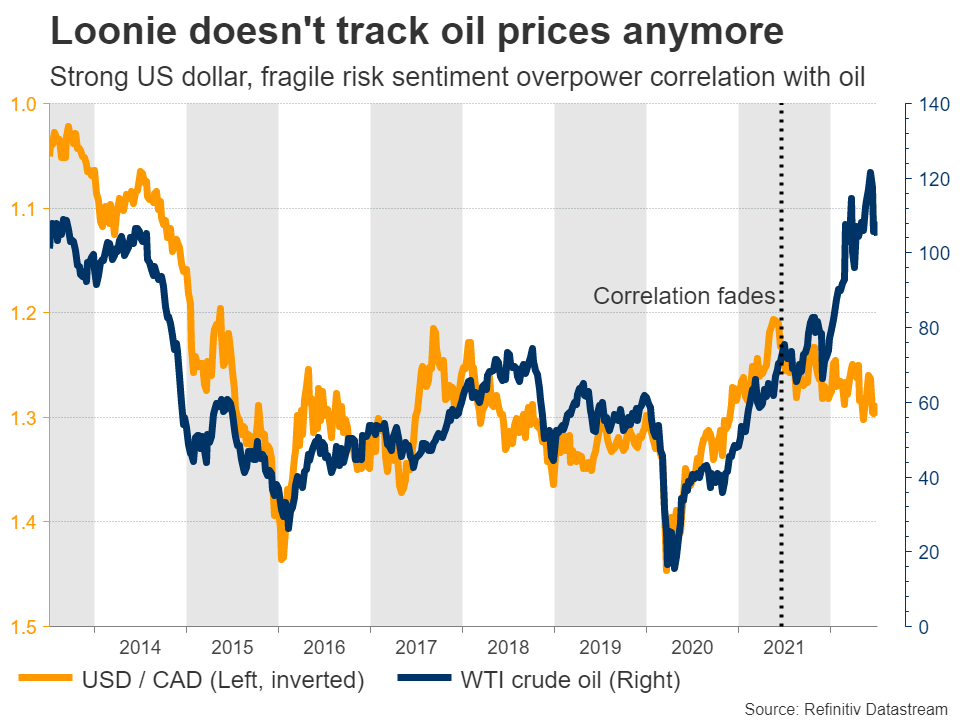

Overall, there’s reason to be cautious on the loonie. Investors assume the BoC will out-hike the Fed this year, which may be unrealistic considering how quickly the air is coming out of the nation’s ‘bubbly’ housing market. Separately, if the currency couldn’t gain ground with oil prices up 35% this year, what happens if prices extend their latest drop?

RBNZ - A steady hand

New Zealand’s economy continues to hum along. The unemployment rate is at a record low, consumption remains healthy, and various surveys suggest inflation is raging.

There are some worrisome spots too. Consumer and business confidence has taken a sharp hit lately while the housing market is cooling. Higher rates have clearly dampened demand, but this is what the RBNZ wanted to achieve in the first place.

Hence, there’s no real reason for the Reserve Bank to deviate from its strategy of raising rates in 50bps increments when it meets on Wednesday, which is also what the market has priced in - both for this meeting and next month. The bar for a hawkish surprise is therefore high, unless the officials want to put a 75bps move on the table.

As for the kiwi, what the RBNZ does is secondary to how global forces evolve. Recession worries are currently dominating, putting pressure on risk sentiment and commodity prices, both negative for the kiwi. Any relief rallies are likely to remain shallow in this regime, until nerves around global growth calm down.

China - Economic contraction?

Over in China, the ball will get rolling with inflation stats for June over the weekend ahead of trade data on Wednesday, culminating with economic growth numbers for the second quarter on Friday.

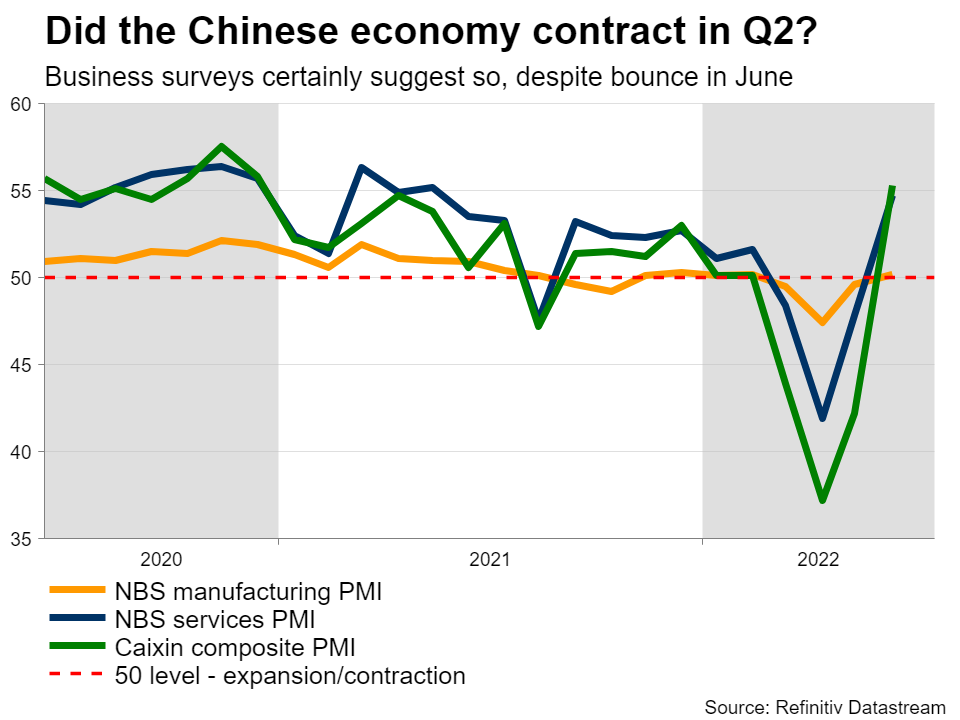

Several cities went into strict lockdowns during this quarter, and the collapse in demand was evident in retail sales, which contracted sharply in April and May. It was a similar story in business surveys and industrial output, thanks to the struggling property sector. This begs the question - did the overall economy contract in Q2?

It’s a close call, because most of the evidence for June points to a solid recovery as the lockdowns were lifted to close the quarter. This could be a key piece of the puzzle for global risk sentiment, with the capacity to impact equity markets and commodity currencies such as the Australian dollar.

Speaking of the aussie, Australia’s jobs report for June will be released on Thursday.

Finally in the UK, monthly GDP stats for May are out on Wednesday. That said, sterling pays more attention to stock markets these days. Politics will be in the spotlight too as the ruling Conservative party scrambles to select a replacement for outgoing Prime Minister Johnson.