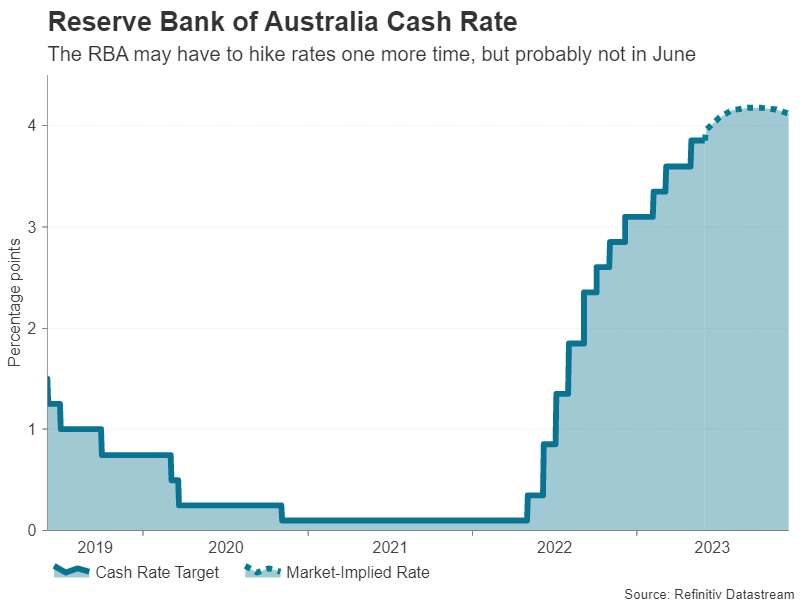

Will the RBA deliver another surprise hike?

The Reserve Bank of Australia caught markets off guard when it hiked rates last month and there’s a risk that policymakers could again lift borrowing costs higher by 25 basis points when they hold their June meeting on Tuesday.

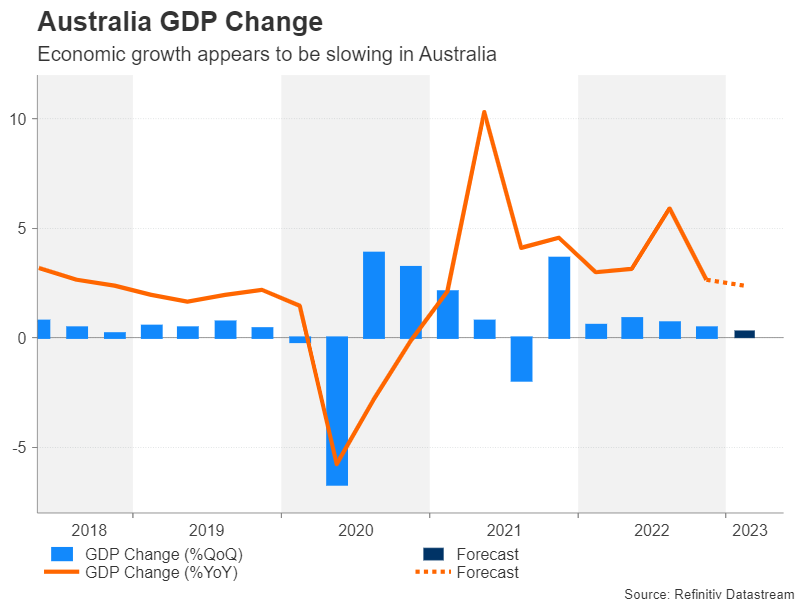

However, the economic data has been somewhat mixed lately so the RBA might decide to pause again to get a better picture of what is happening in the economy. The jobless rate edged up slightly in April and the flash PMIs pointed to a modest softening in economic activity in May. However, monthly inflation readings for April were hotter-than-expected.

First quarter GDP growth figures are due on Wednesday but might come too late for the RBA to fully factor the data into its decision. Also out on Wednesday is the AIG (NYSE:AIG) manufacturing index.

Another consideration for policymakers is the faltering recovery in China. The slowing demand for industrial metals and other resources from the world’s largest consumer of such commodities is bad news for Australian exporters whose number one market is China.

Hence, the RBA has more incentive to skip a hike, while maintaining a tightening bias and investors appear to be converging with this view as they’ve currently assigned around 55% probability of no change in June but a 25-bps hike is fully priced in for August.

The Australian dollar has tumbled to more than six-month lows versus its US counterpart but could receive support from a hawkish RBA. Aussie traders will also be keeping an eye on some Chinese indicators coming up next week.

The trade balance will be important on Wednesday to see how exports and imports fared in May, and on Friday, the latest consumer and producer price indices will provide fresh clues on the strength of domestic demand.

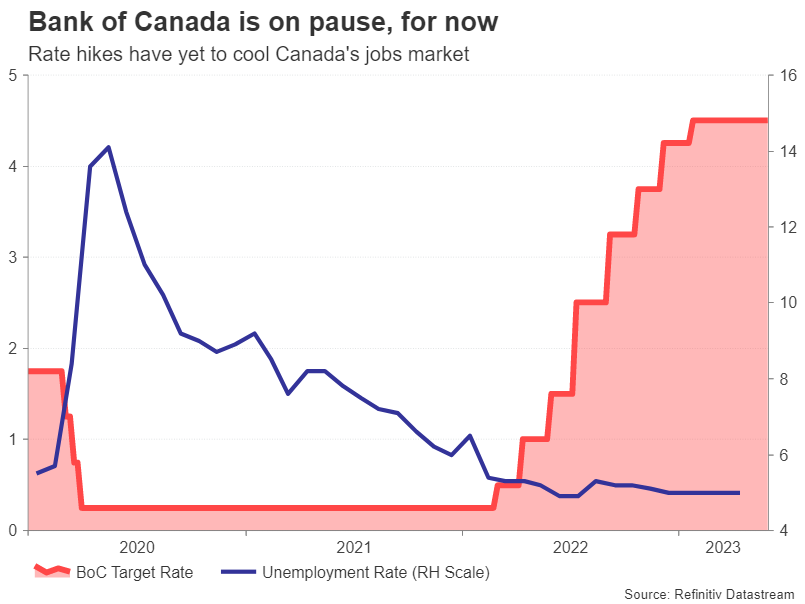

BoC may not be done with rate hikes

The Bank of Canada has been on pause since March but like the RBA, a rate hike is back on the table. The Canadian economy enjoyed a strong rebound in GDP growth in the first quarter, expanding by 0.8% q/q. The labour market is heating up again, while headline inflation unexpectedly accelerated in April.

However, underlying measures of inflation continued to decline and this may convince enough policymakers to stay on pause for another meeting in case the increase in headline CPI was a blip.

Markets are expecting the BoC to remain on hold at least until September before resuming its tightening cycle. But should policymakers display a strong inclination to hike soon, this would likely increase the focus on Friday’s employment report for May.

Another strong set of jobs numbers could bring rate hike bets forward, boosting the Canadian dollar.

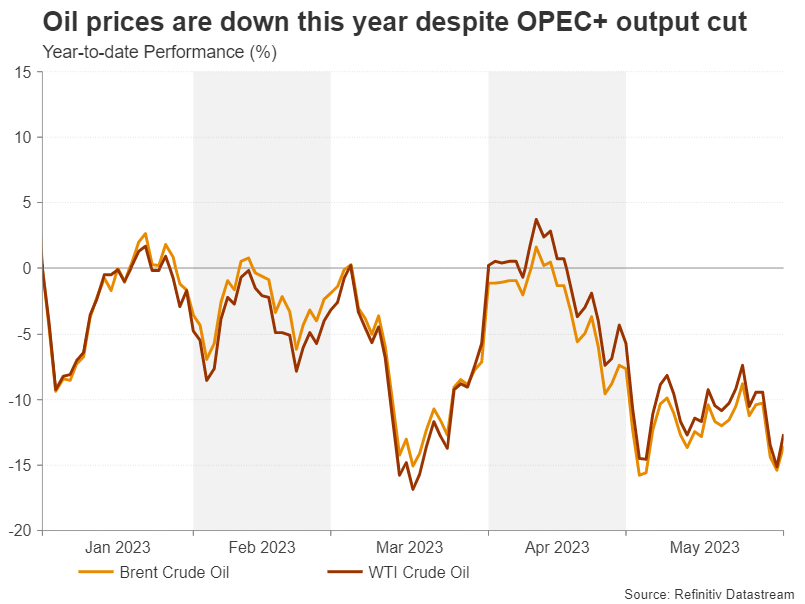

OPEC+ has a tough balance to strike

The oil-sensitive loonie will also be watching developments with OPEC+. The oil cartel will gather on Sunday to decide whether to follow up April’s surprise cut with a further reduction in output quotas. Russia has signalled it does not favour more cuts but the de-facto leader of the pact, Saudi Arabia, is more mindful about the lacklustre performance of oil prices over the last couple of months.

Indeed, Saudi Arabia is in a difficult position. By slashing production yet again it could end up conceding more market share to Russia, who is selling oil on the cheap to Asian countries that are able to evade Western sanctions slapped on Moscow over the war in Ukraine.

The other problem for the Saudis is that another output cut might send the message that oil producers are becoming more worried about the weakening outlook for oil prices and this could trigger the opposite reaction in oil futures, unless they decide on a very large reduction.

Quieter week looms for the dollar

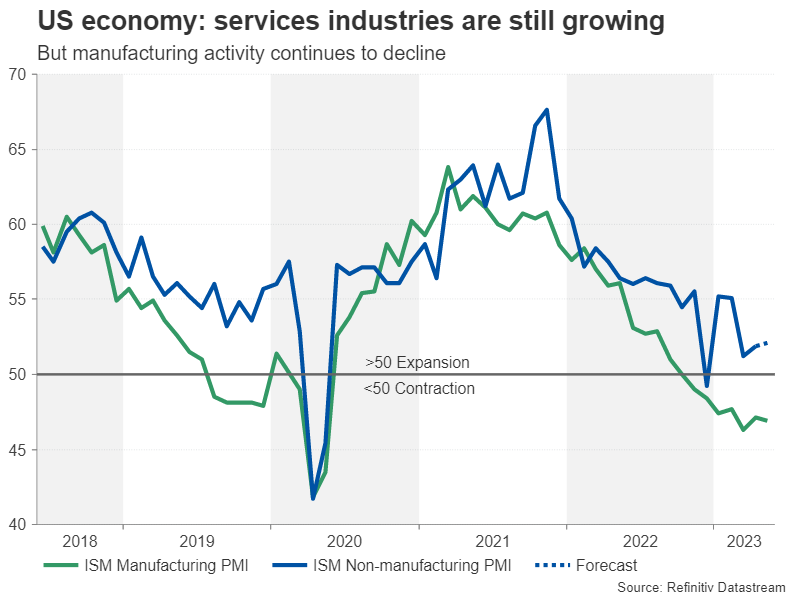

In the United States, the main highlight is the ISM non-manufacturing PMI on Monday, and April factory orders due the same day might attract some interest too.

Although the American economy has lost some steam lately, it is far from being out of momentum and the ISM survey should offer a glance as to how things stood in May in the services sector.

Communication from the Fed has been rather conflicting heading into the June 14 FOMC decision, but more recently, it appears that the doves, likely led by Chair Powell himself, are building a case to sit out the next meeting.

There is still one more CPI report on the way before then, but the ISM PMI will have some significance given the growing divisions within the Fed.

If the odds start to shift again in favour of a June hike, the US dollar could find itself back on the front foot.