Aussie eyes RBA and GDP as it pushes against risk tide

The Australian dollar’s steady upward path since late January has come under threat from the heightened geopolitical tensions. But the currency still has substantial support from higher commodity prices as well as strengthening expectations that the Reserve Bank of Australia will raise interest rates later this year, even as traders scale back rate hike bets for the Fed.

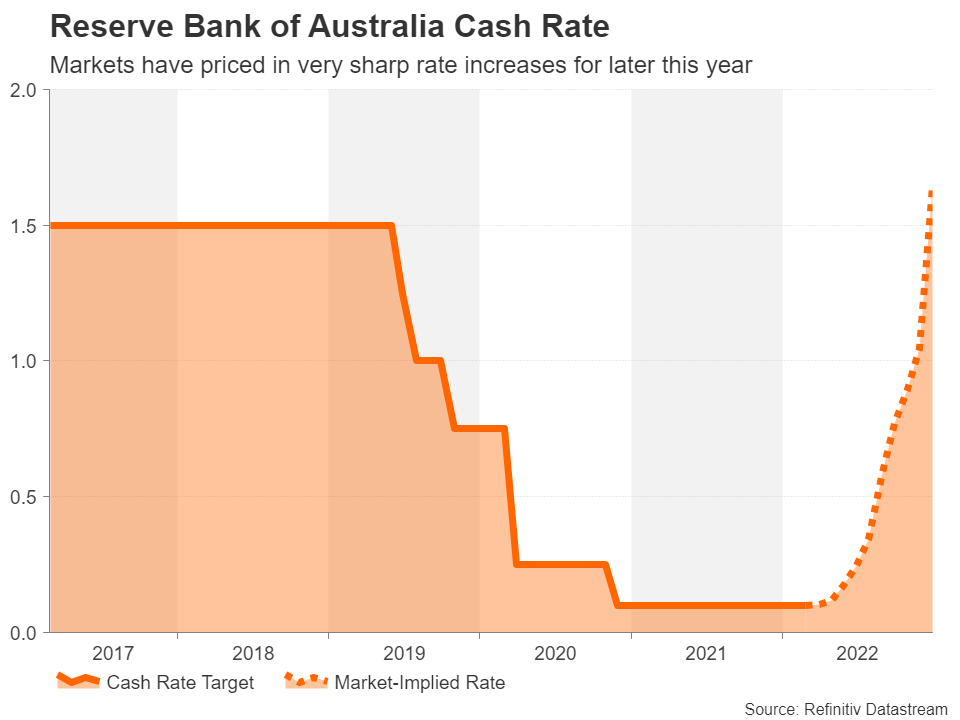

The RBA meets on Tuesday and following the February decision to end bond purchases, no action is anticipated this time. However, investors will be hoping to find clues in the RBA statement about the timing of a rate hike. Wages in Australia grew by a paltry 2.3% year-on-year in Q4, so policymakers aren’t about to suddenly turn hawkish. However, other indicators due next week might not be quite so soft.

Australia’s GDP likely bounced back strongly in the final three months of 2021, data out on Wednesday is expected to show. Ahead of the GDP print, quarterly business inventories are out on Monday along with retail sales and private sector credit for January. Net exports contribution for Q4 will follow on Tuesday. January building approvals on Thursday might attract some attention too.

BoC expected to join rate hike club

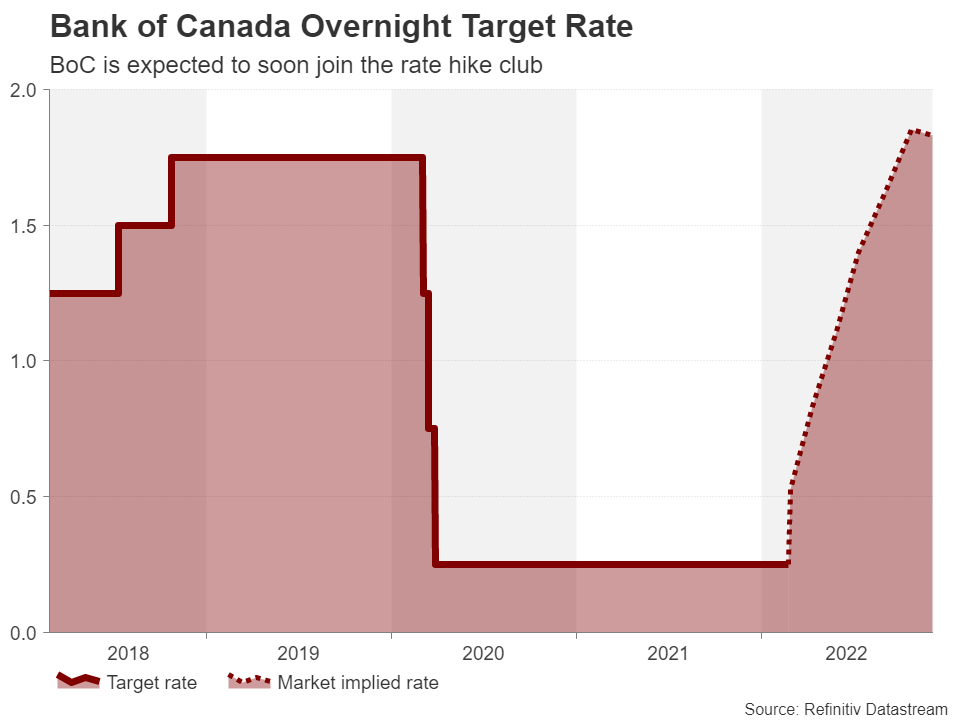

Across the Pacific, the Bank of Canada probably won’t be beating around the bush any longer and will raise interest rates on Wednesday. A 25-basis points increase is fully priced in, and with inflation heating up more than expected in January, a surprise double hike cannot be ruled out.

Though, the chances of a 50-bps move are slim given the recent somewhat disappointing employment report and the ongoing truckers protest that could be having a dampening effect on the economy, not to mention the Ukraine fallout.

The Canadian dollar has slid to two-month lows against its US counterpart so a more hawkish-than-anticipated tone could provide a notable boost. Traders will also be watching January producer prices on Monday, the Q3 GDP print on Tuesday and the Ivey PMI on Friday.

Don’t count on OPEC to ease supply pressure

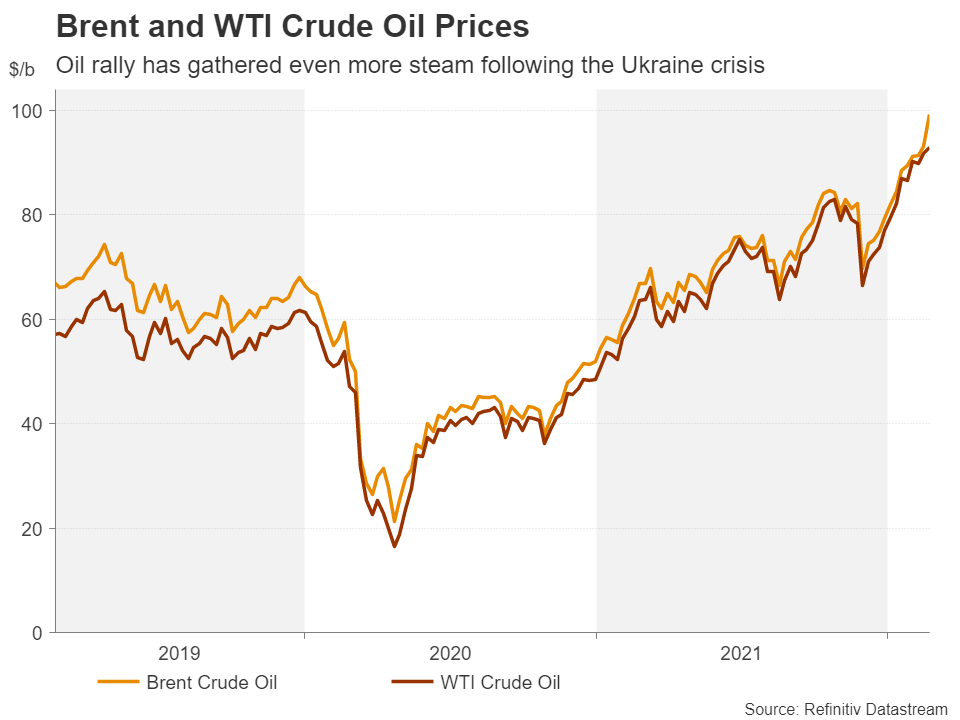

Also important for the loonie will be the outcome of the OPEC+ meeting on Wednesday. The OPEC-led alliance of major producers that includes Russia is not expected to accelerate its plan of gradually undoing the 2020 supply cuts despite oil prices shooting higher.

Oil futures hit $100 a barrel after Russian forces began to invade Ukraine, worsening the energy crisis. But this is unlikely to change leading producer Saudi Arabia’s mind about heeding calls from Washington to pump more oil, at least not yet.

US data may add to dollar’s upside

The US dollar skyrocketed to near 20-month highs as investors sought safety from the eruption of war in Ukraine. Safe-haven demand has more than offset dimming expectations of the Fed raising interest rates aggressively over the coming months.

Futures markets are now pricing in six rate hikes versus 6.5 only a few says ago. However, it’s not certain if the incoming data can make much of a difference to Fed policy speculation now that geopolitical risks have entered the equation.

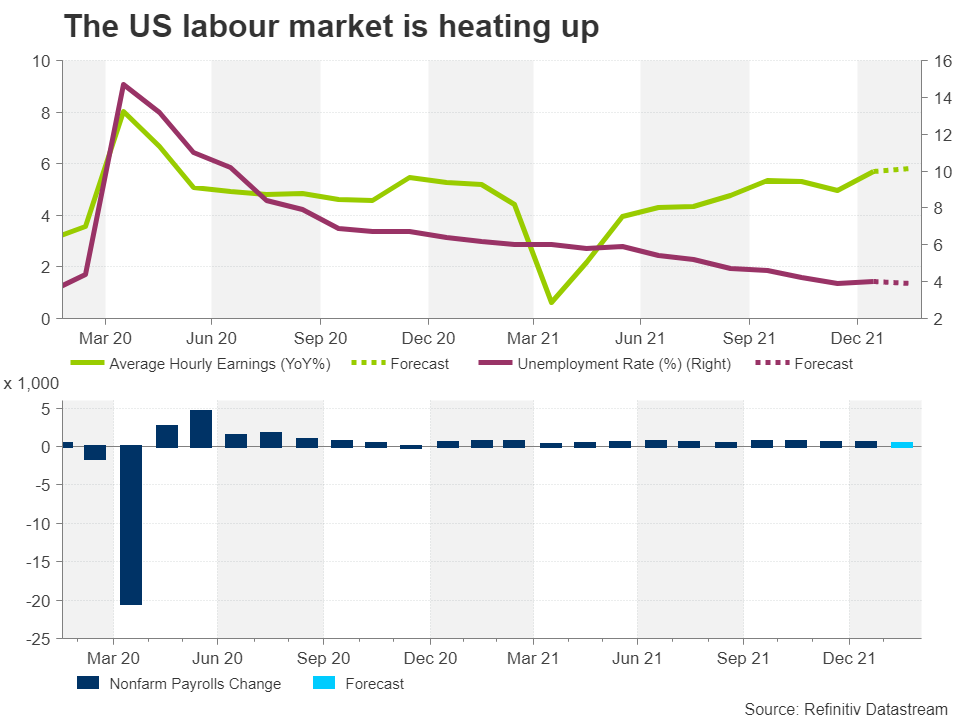

Nevertheless, with another solid jobs report and upbeat ISM PMIs predicted, a further dollar boost is possible.

Starting the week, though, is the Chicago PMI on Monday, with the ISM equivalent coming up on Tuesday. The ISM non-manufacturing PMI and factory orders will follow on Thursday before the focus turns to the NFP numbers on Friday.

Both ISM PMIs are forecast to edge slightly higher in February, but nonfarm payrolls are expected to have risen at a slightly lower pace, moderating to a gain of 438k versus 467k in January.

The unemployment rate is projected to tick lower by 0.1 percentage points to 3.9% and average hourly earnings are forecast to pick up slightly to 5.8% year-on-year.

Hotter-than-expected readings could push bets of Fed rate hikes higher, but ultimately, investors will mainly be paying attention to whether the Ukraine crisis is prompting any change in tone among Fed policymakers.

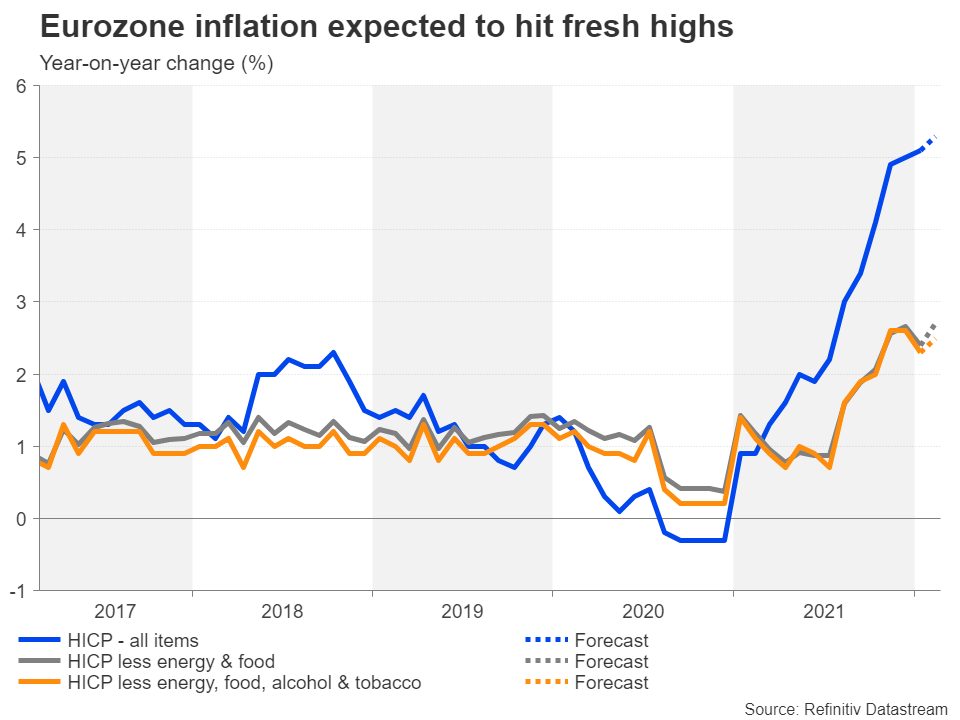

Can Eurozone inflation shore up sinking euro?

The flash estimate of euro area inflation for February is due on Wednesday. The harmonized index of consumer prices is forecast to rise to another record, reaching 5.3% y/y, adding pressure on the European Central Bank to withdraw monetary stimulus more quickly.

But like the Fed, the new focus in the run up to the March meeting is whether the ECB will tread more cautiously now that dark clouds are forming over Europe.

Other releases will include the final PMI prints on Tuesday and Thursday, producer prices and the jobless rate for January on Thursday, as well as retail sales on Friday.

The euro has nosedived, testing the $1.11 level, on mounting worries that the Eurozone economy will take a significant hit from sanctions against Russia that could potentially hurt oil and gas flows to Europe. Given that Russian President Vladimir Putin is unlikely to go down the path of diplomacy, the euro is at risk for further slides.