- CPI numbers due in the UK, Japan, Canada and New Zealand

- China to also come into the spotlight as Q1 GDP eyed

- US retail sales to kickstart the week as earnings season gets underway

CPI figures to headline UK data flurry

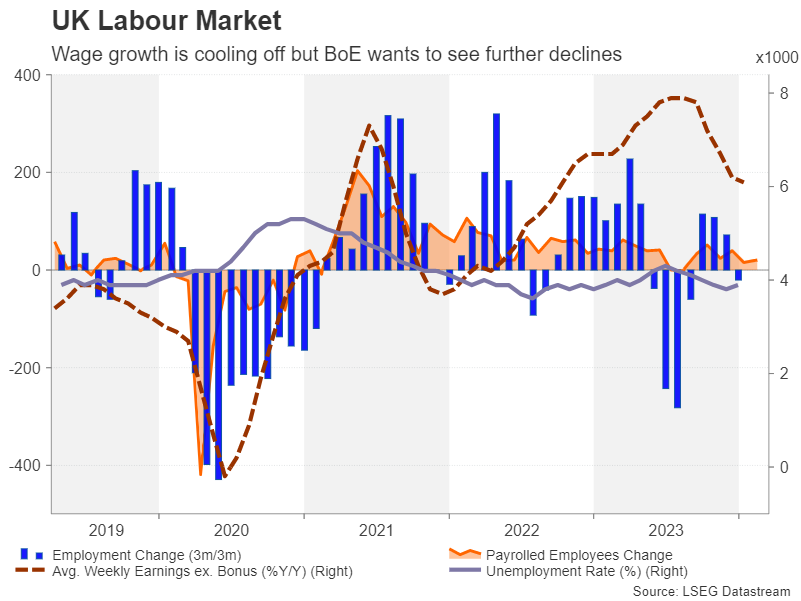

After yet another hot CPI report in the United States, inflation data will remain at the forefront of the upcoming week’s releases, including in the United Kingdom. But first up on the UK agenda will be the February employment report on Tuesday.

Employment declined in the three months to January, pushing up the jobless rate to 3.9%. The UK labour market has slowed down substantially over the past year amid a slight contraction in GDP. The economy appears to be rebounding but jobs growth could remain weak for some time yet. From a wage inflation perspective, a cooling labour market can only be good news.

Growth in average weekly earnings excluding bonuses has moderated from a peak of 8.9% y/y last summer to 6.1% in January. A further deceleration is likely in February – a trend underscored by a Bank of England survey showing that wage growth expectations have fallen to the lowest in two years.

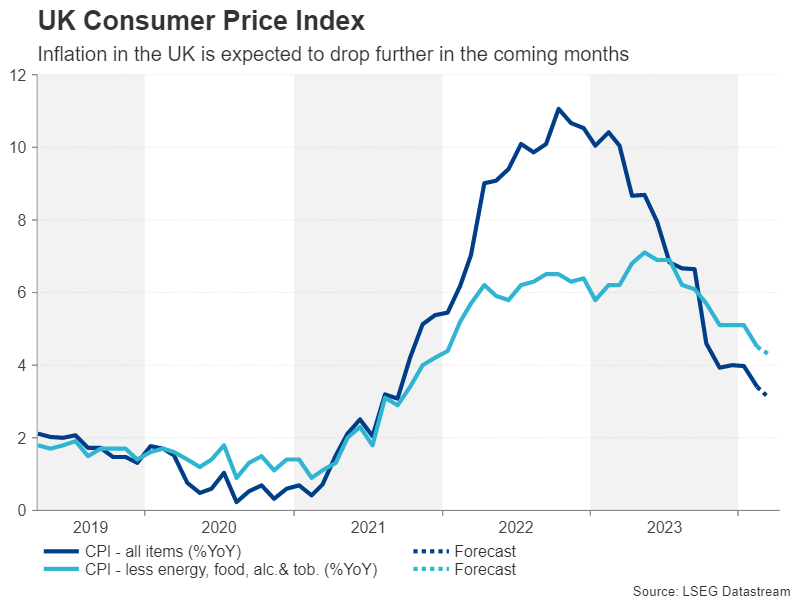

However, softer wage growth won’t be the whole story for sterling next week as investors will also be dissecting the latest CPI readings on Wednesday. UK inflation fell to 3.4% in February and another drop is expected for March to 3.1%. The core figure is also forecast to decline again.

Finally, on Friday, retail sales numbers for March will be watched for clues on whether consumer spending is picking up or not.

Cable is currently testing the floor of the sideways range it’s been trading in since December and the incoming data pose a downside risk should they suggest that the Bank of England is still on track to start cutting rates in August, while the Fed’s timeline has started to shift to September.

If the UK’s inflation outlook continues to improve, the pound might struggle to hold above $1.25 and traders will either want to see Britain’s economy recovering more strongly or US growth losing steam to defend that key level.

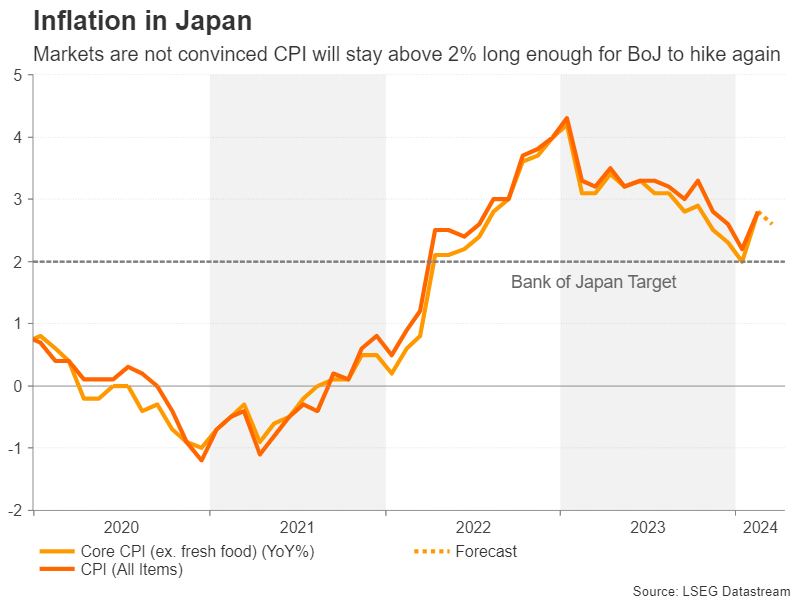

Can Japanese CPI lift the downtrodden yen?

Inflation in Japan edged up sharply in February after a year-long decline. Core CPI that excludes fresh food prices and which the Bank of Japan targets for achieving 2% inflation rose to 2.8% from 2.0%. However, whilst there was probably a further modest uptick in overall CPI, the core figure, out on Friday, is forecast to have eased to 2.6%.

Nevertheless, investors are questioning whether inflationary pressures in Japan can re-accelerate much from hereon and thus, expectations for additional rate hikes remain muted – something that has been weighing heavily on the yen.

Yet, the Bank of Japan seems to be subtly paving the way for a second rate hike towards the end of the year and Governor Ueda has hinted as much. There are also reports that the bank will revise up its inflation forecasts at its next meeting on April 26. Policymakers are hopeful that bumper pay deals in this year’s spring wage negotiations and an end to energy subsidies at the end of May will keep inflation above 2% in the medium-term horizon.

But until this is reflected in the CPI data, the yen is unlikely to find much love.

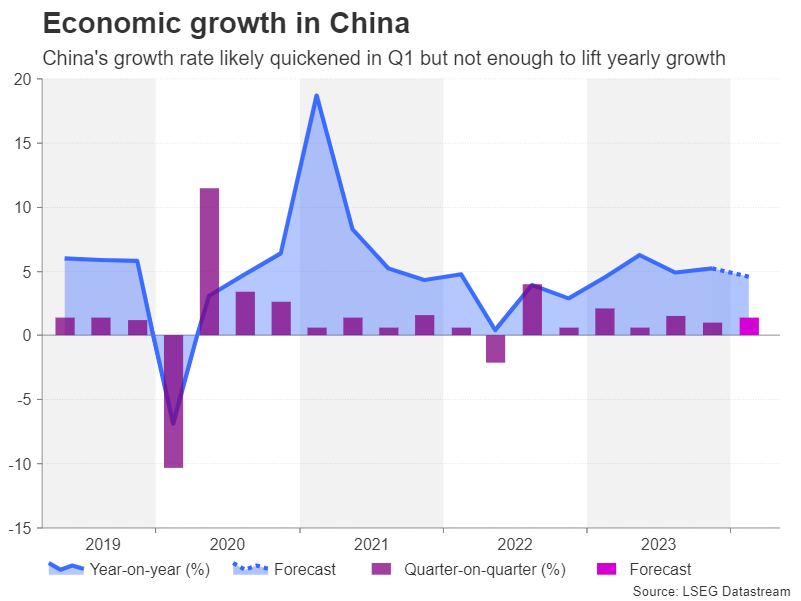

A mixed picture for China’s economy

China is set to publish GDP estimates on Tuesday as optimism about its economic recovery improves. The world’s second largest economy probably expanded by 1.4% quarter-on-quarter in the three months to March, quickening from a 1% pace in the prior quarter. However, markets might focus more on the annual rate that’s expected to have slowed from 5.2% to 4.6%.

The March figures for industrial output and retail sales could also leave investors unimpressed as both are anticipated to have eased year-on-year compared to February.

Any disappointment from the GDP stats could add to the aussie’s and kiwi’s woes, which have been swimming in choppy waters lately amid the constant swings in Fed rate cut bets. For the Australian dollar, traders will also be keeping an eye on domestic jobs numbers on Thursday, while for the New Zealand dollar, Wednesday’s CPI prints will be crucial.

The Reserve Bank of New Zealand maintained a very neutral stance at its April policy meeting, signalling that a rate cut is some time away. But should CPI rise by less than the expected rate of 4.1% y/y in the first quarter, investors might become more confident about an August cut.

Canadian inflation eyed

Another country reporting CPI data next week is Canada, due Tuesday. A June rate cut is still in play for the Bank of Canada despite heightened caution globally about sticky inflation. Canada’s headline CPI rate eased to 2.8% in February and underlying measures fell too.

A continuation of that trend in March could boost the odds of a rate cut in June, which currently stand at less than 50%, piling more pressure on the Canadian dollar.

The loonie has already shed about 3.5% against the US dollar this year so any further signs of a possible divergence in monetary policy between the Fed and the BoC could increase those losses.

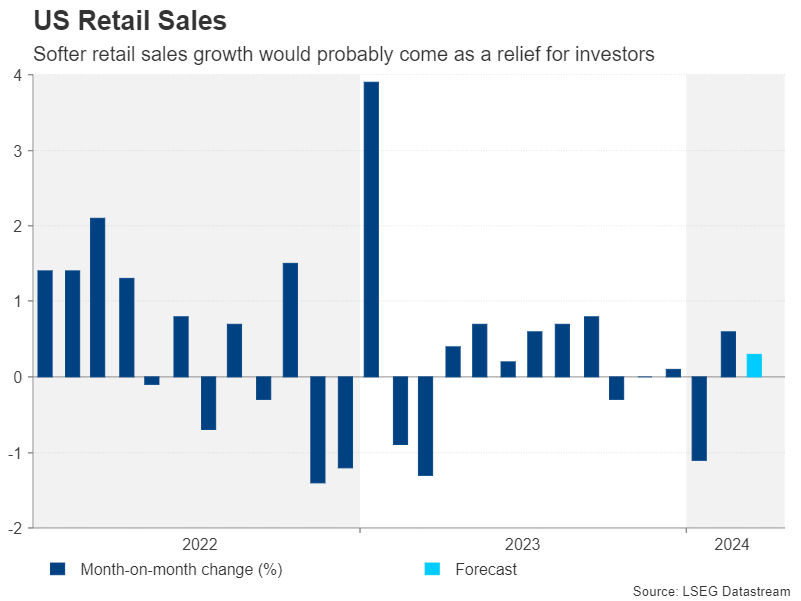

Retail sales only threat for dollar bulls

South of the border, the US schedule is looking relatively light, with Monday’s retail sales numbers being the top release.

The latest NFP and CPI reports both dented expectations of a summer rate cut by the Fed so investors will be hoping for some softer data next, and they could well get that.

Retail sales are forecast to have risen by 0.3% m/m in March, slowing from the prior 0.6% rate. Other indicators to watch out of the US are the Empire State Manufacturing index, also on Monday, building permits and housing starts along with industrial production on Tuesday, to be followed by the Philly Fed manufacturing index and existing home sales on Thursday.

With markets still reeling from the setback to early rate cut hopes, the dollar will likely hold firm. But shares on Wall Street stand a chance of staging a rebound if the Q1 earnings season gets off to a strong start. The spotlight next week will fall on Netflix (NASDAQ:NFLX), which announces its results on Thursday.