Today is another day of headline watching for the latest spin on the fiscal cliff negotiations, as risk and the USD continue to pivot on this issue in an environment of extremely low volatility. Aussie crosses looking a bit weak on gold rout.

Fiscal ramp

Today is about whether yesterday’s “developments” on the fiscal cliff – president Obama also chimed in to express optimism that a deal could be reached before Christmas – are enough to boost sentiment and risk correlated trades beyond the knee jerk reaction to the rhetoric in the US yesterday. But isn’t a fairly optimistic scenario already priced in at this point now that we’ve bounced so enthusiastically off the lows?

Whatever Congress comes up with, fiscal spending will likely shrink slightly and wage earners are going to lose 2% of their income as the payroll tax cut expires. And the Republican anti-tax core (http://www.bloomberg.com/news/2012-11-29/boehner-s-anti-tax-caucus-leaves-little-room-on-cliff.html) will have a bad case of egg in the face if they allow the tax cut expiries to go through – I still think there is room for gridlock shenanigans rather than bipartisanship.

There was also a big miss in the US October New Home Sales figure to deal with yesterday, as this is an area that is supposed to be gaining momentum in the US, not suddenly showing a large downside surprise and a large downward revision of the previous month’s data – but of course – it was all about superstorm Sandy, right? The September downward revision certainly wasn’t, but that storm’s effects will mean it is difficult to get a proper read on many of the US numbers for another couple of months (and the data on the other side could get a boost on rebuilding efforts).

Abe talks down the JPY again

Shinzo Abe was out fighting on all fronts on the bluster aimed at weakening the JPY, claiming that BoJ policy should only be tightened once an inflation target of 2% has been met, talking up stimulus plans (a JPY 200 trillion (around 40% of GDP) stimulus package has been circulated previously) and lashing out at China on its treatment of the islands dispute. The JPY responded strongly, but at some point here, we’re going to need to see the reality of the easing and not just tough talk. Elections on December 16th are the next major pivot point.

Aussie cross observations

The Aussie looked quite weak overnight, as AUD/NZD appears to be giving up its recent rally attempt with the swoon well back through the 1.2700 level today could reinvigorate the strategic bearish picture as the 200-day moving average up near 1.2775 proved strong resistance. A bigger move through 1.2630 provides better confirmation. AUD/CAD also looks ready to sell-off again now that the momentum has come out of the throwback rally.

The 1.0300 200-day moving average is the next focus lower. AUD/USD’s sickly advance also appears in danger of foundering in this low momentum environment, though bears really need a move below 1.0400 to get firmer traction. The aussie should have a hard time getting much upside traction after the gold rally turned to a rout yesterday.

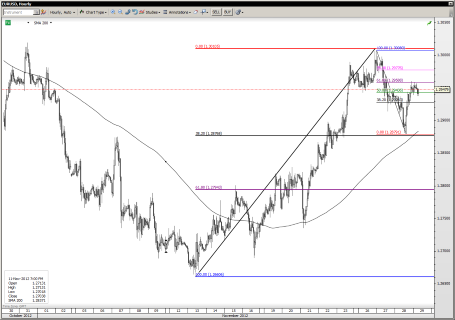

Chart: EUR/USD

EUR/USD touched a perfect 0.618 retracement level of the sell-off at 1.2960 late yesterday, putting today’s support level around the 1.2930 area daily pivot and the bigger pivot lower is yesterday’s 1.2880 low, a break of which could open up for a test of the recent support. Again, the wide range lens suggests we are waiting for something to happen beyond the 1.300 resistance and 1.2800 support before a bigger getting a directional indication.

EUR/USD" title="EUR/USD" width="455" height="320" />

EUR/USD" title="EUR/USD" width="455" height="320" />

Looking ahead

Today is another day of headline watching, as we don’t have much in the way of economic data. Euro peripheral spreads have been collapsing in the wake of the Greek deal, but this doesn’t seem to be the focus for the moment, as yesterday’s rally in EUR/USD was merely timed with the fiscal cliff rhetoric and bump in risk appetite.

Today offers a fairly light economic calendar, with a few eurozone confidence surveys up at 1000 GMT, the BoE’s King is out with a financial stability report at 1030 and the US GDP Revision is up at 1330, together with jobless claims.

Be careful out there.

Fiscal ramp

Today is about whether yesterday’s “developments” on the fiscal cliff – president Obama also chimed in to express optimism that a deal could be reached before Christmas – are enough to boost sentiment and risk correlated trades beyond the knee jerk reaction to the rhetoric in the US yesterday. But isn’t a fairly optimistic scenario already priced in at this point now that we’ve bounced so enthusiastically off the lows?

Whatever Congress comes up with, fiscal spending will likely shrink slightly and wage earners are going to lose 2% of their income as the payroll tax cut expires. And the Republican anti-tax core (http://www.bloomberg.com/news/2012-11-29/boehner-s-anti-tax-caucus-leaves-little-room-on-cliff.html) will have a bad case of egg in the face if they allow the tax cut expiries to go through – I still think there is room for gridlock shenanigans rather than bipartisanship.

There was also a big miss in the US October New Home Sales figure to deal with yesterday, as this is an area that is supposed to be gaining momentum in the US, not suddenly showing a large downside surprise and a large downward revision of the previous month’s data – but of course – it was all about superstorm Sandy, right? The September downward revision certainly wasn’t, but that storm’s effects will mean it is difficult to get a proper read on many of the US numbers for another couple of months (and the data on the other side could get a boost on rebuilding efforts).

Abe talks down the JPY again

Shinzo Abe was out fighting on all fronts on the bluster aimed at weakening the JPY, claiming that BoJ policy should only be tightened once an inflation target of 2% has been met, talking up stimulus plans (a JPY 200 trillion (around 40% of GDP) stimulus package has been circulated previously) and lashing out at China on its treatment of the islands dispute. The JPY responded strongly, but at some point here, we’re going to need to see the reality of the easing and not just tough talk. Elections on December 16th are the next major pivot point.

Aussie cross observations

The Aussie looked quite weak overnight, as AUD/NZD appears to be giving up its recent rally attempt with the swoon well back through the 1.2700 level today could reinvigorate the strategic bearish picture as the 200-day moving average up near 1.2775 proved strong resistance. A bigger move through 1.2630 provides better confirmation. AUD/CAD also looks ready to sell-off again now that the momentum has come out of the throwback rally.

The 1.0300 200-day moving average is the next focus lower. AUD/USD’s sickly advance also appears in danger of foundering in this low momentum environment, though bears really need a move below 1.0400 to get firmer traction. The aussie should have a hard time getting much upside traction after the gold rally turned to a rout yesterday.

Chart: EUR/USD

EUR/USD touched a perfect 0.618 retracement level of the sell-off at 1.2960 late yesterday, putting today’s support level around the 1.2930 area daily pivot and the bigger pivot lower is yesterday’s 1.2880 low, a break of which could open up for a test of the recent support. Again, the wide range lens suggests we are waiting for something to happen beyond the 1.300 resistance and 1.2800 support before a bigger getting a directional indication.

EUR/USD" title="EUR/USD" width="455" height="320" />Looking ahead

Today is another day of headline watching, as we don’t have much in the way of economic data. Euro peripheral spreads have been collapsing in the wake of the Greek deal, but this doesn’t seem to be the focus for the moment, as yesterday’s rally in EUR/USD was merely timed with the fiscal cliff rhetoric and bump in risk appetite.

Today offers a fairly light economic calendar, with a few eurozone confidence surveys up at 1000 GMT, the BoE’s King is out with a financial stability report at 1030 and the US GDP Revision is up at 1330, together with jobless claims.

Be careful out there.