Yesterday, the Fed hiked rates by 25bps, and signaled six more lift-offs until the end of this year. Though a much more hawkish stance than in December, the US dollar drifted lower, and equities traded higher, perhaps as this just matched the already hawkish market expectations. Today, it is the turn of the BoE to decide on monetary policy, and it will be interesting to see whether officials of this Bank will also sound hawkish.

Fed Sees 7 Hikes This Year; Will BoE Sound Equally Hawkish?

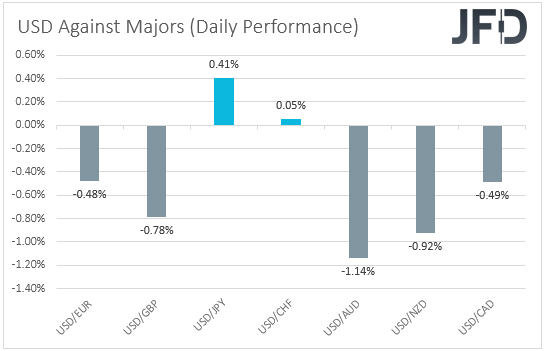

The US dollar traded lower against all but two of the other major currencies on Wednesday and during the Asian session Thursday. It gained only against JPY, while it was found virtually unchanged versus CHF. The main gainers were AUD, NZD, and GBP in that order.

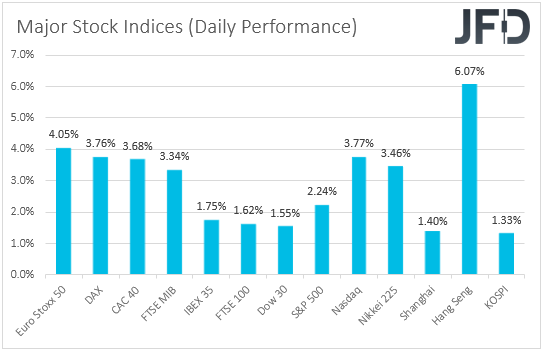

The weakening of the US dollar and the other safe havens, yen and franc, combined with the strengthening of the risk-linked Aussie, Kiwi, and Loonie, but as well as the euro and the pound, suggest that market sentiment continued to improve following headlines and reports with regards to progress in negotiations between Russia and Ukraine. Indeed, turning our gaze to the equity world, we see that major EU and US indices were a sea of green, with the upbeat morale rolling into the Asian session today.

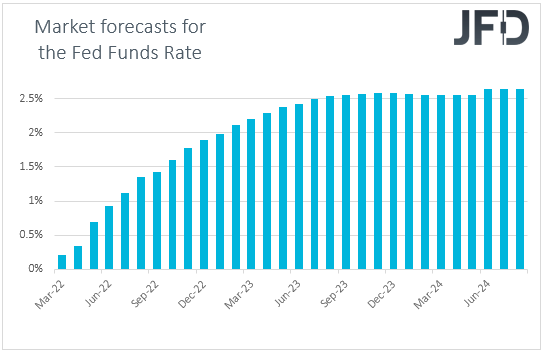

Yesterday, the main event on the economic calendar was the FOMC decision, with the Committee hiking rates by 25bps for the first time since 2018, as it was broadly expected. The highlight though was not the rate hike, rather than the updated "dot plot." Remember that the December one pointed to only three quarter-point hikes throughout 2022, but now, the dots were more aggressive, with the median of this year pointing to 7 liftoffs, including the one delivered. In other words, officials expect 6 more hikes, which means that they are willing to keep pushing the hike button at each of the remaining gatherings of the year.

At the press conference following the decision, Fed Chair Jerome Powell said that the economy was strong enough to weather those rate hikes, while maintaining strong hiring and wage growth, adding that if they concluded that it would be appropriate to move more quickly to remove accommodation, then they will do so.

The US dollar strengthened somewhat at the time the decision was known, but came under selling interest during Powell’s press conference. With the Fed being much more hawkish than in December, this pointed to a sell-the-fact market reaction.

After all, 7 quarter-point liftoffs for 2022 were already priced in by market participants heading into the meeting. In other words, investors were already overly hawkish, and exceeding their expectations was a very hard task for the Fed. Besides hopes around a ceasefire between Russia and Ukraine, this may have been another supportive factor for equities.

Moving ahead, although we switched our stance over equities to neutral, conditional upon a resolution in the crisis in Ukraine, we see decent chances for stock indices to continue drifting north for a while more. Yes, aggressive tightening means higher borrowing costs for companies, as well as lower present values for high-growth firms, but yesterday’s market reaction suggested that the concerns on that front may have already been fully priced in.

For equities to slide again due to monetary policy developments, the Fed needs to appear more aggressive than the market anticipates. After all, according to a Deutsche Bank study, historical data suggests that tighter monetary policy has often been accompanied by solid gains in stocks.

As for today, we have another major central bank deciding on monetary policy and this is the BoE. When they last met, officials of this Bank voted 5-4 for a hike by 25bps, with the 4 dissenters calling for a 50bps increase. Since then, we’ve been highlighting that only one member needed to be convinced for that to happen at this gathering, and the accelerating CPIs for January, indeed, added to speculation on that front.

However, this was the case around a week before Russia invaded Ukraine, with the events unfolding since then, marketwise, raising concerns over the global economic performance, and especially in Europe, something evident by the tumbles in the euro and the pound.

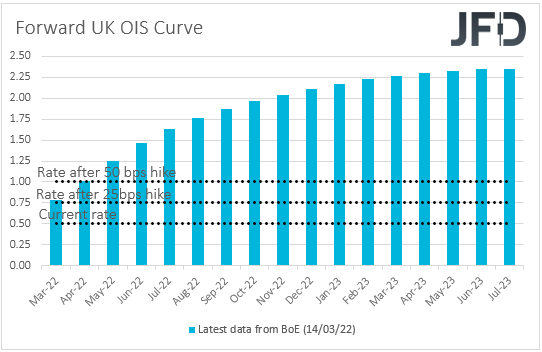

Thus, with all that in mind, we don’t believe that the BoE will now stay willing to hike by 50bps today. According to the UK OIS (Overnight Index Swaps) forward curve, market participants believe that only a quarter-point hike will be delivered. Therefore, if this is the case, we will be eager to see the Bank’s assessment on the war in Ukraine, and how this is affecting their future course of action.

Similarly with the Fed, investors expect the BoE to deliver nearly 7 quarter-point hikes by the end of the year, and it will be interesting to see whether officials’ view and language will match those expectations.

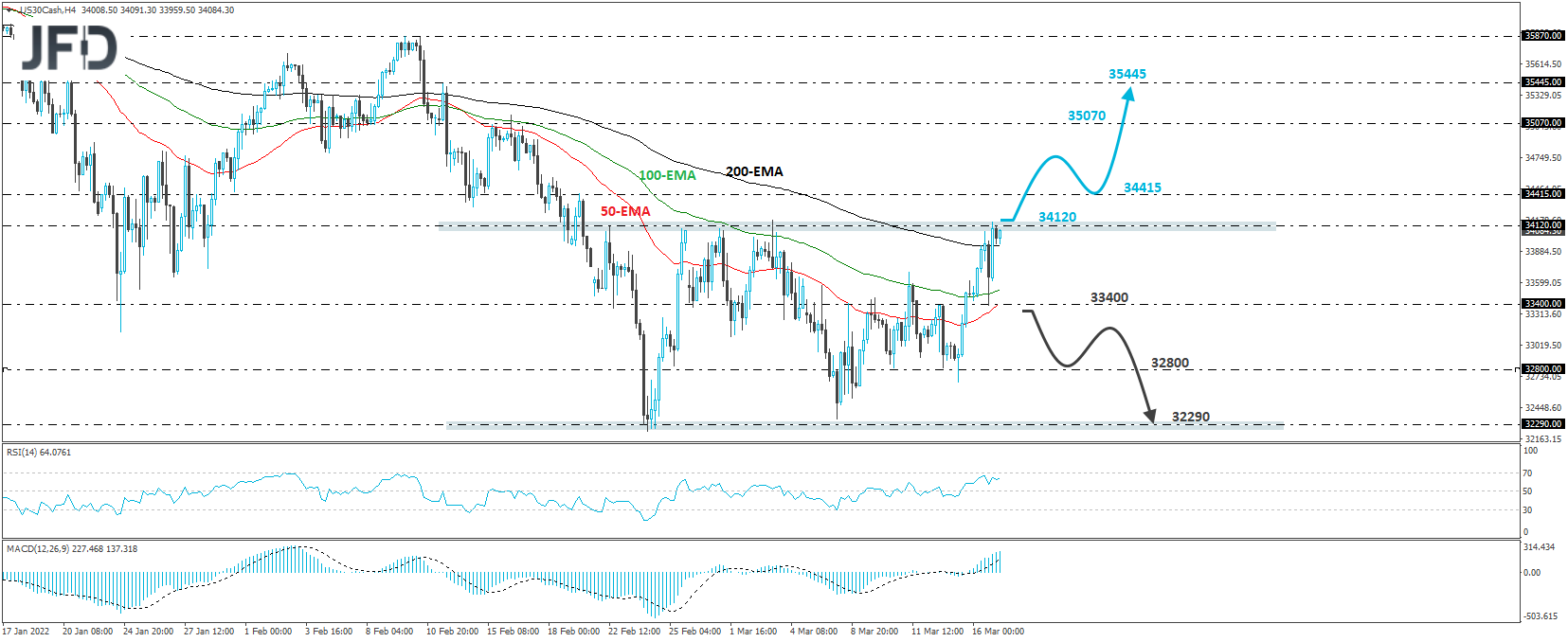

Dow Jones Industrial Average – Technical Outlook

The Dow Jones Industrial Average cash index traded higher yesterday, after it hit support at 33400. However, the advance stayed limited near the key resistance obstacle of 34120, which has been preventing further advances since Feb. 22. Since then, the index has been trading in a range pattern, between that barrier and the 32290, and thus, as long as it stays between those boundaries, we will maintain a neutral stance.

In order to start examining further advances, we would like to see a clear break above 34120, a move that could initially target the peak of Feb. 21, at 34415. Another break, above 34415 could carry larger bullish implications, perhaps paving the way towards the 35070 zone, which if doesn’t hold, could allow extensions towards the high of Feb. 11, at 35445.

On the downside, a dip below 33400 could signal further declines within the existing range. The bears could initially target the 32800 area, which provided decent support between Mar. 10 and 15, the break of which may see scope for extensions towards the lower bound of the aforementioned range, at around 32290.

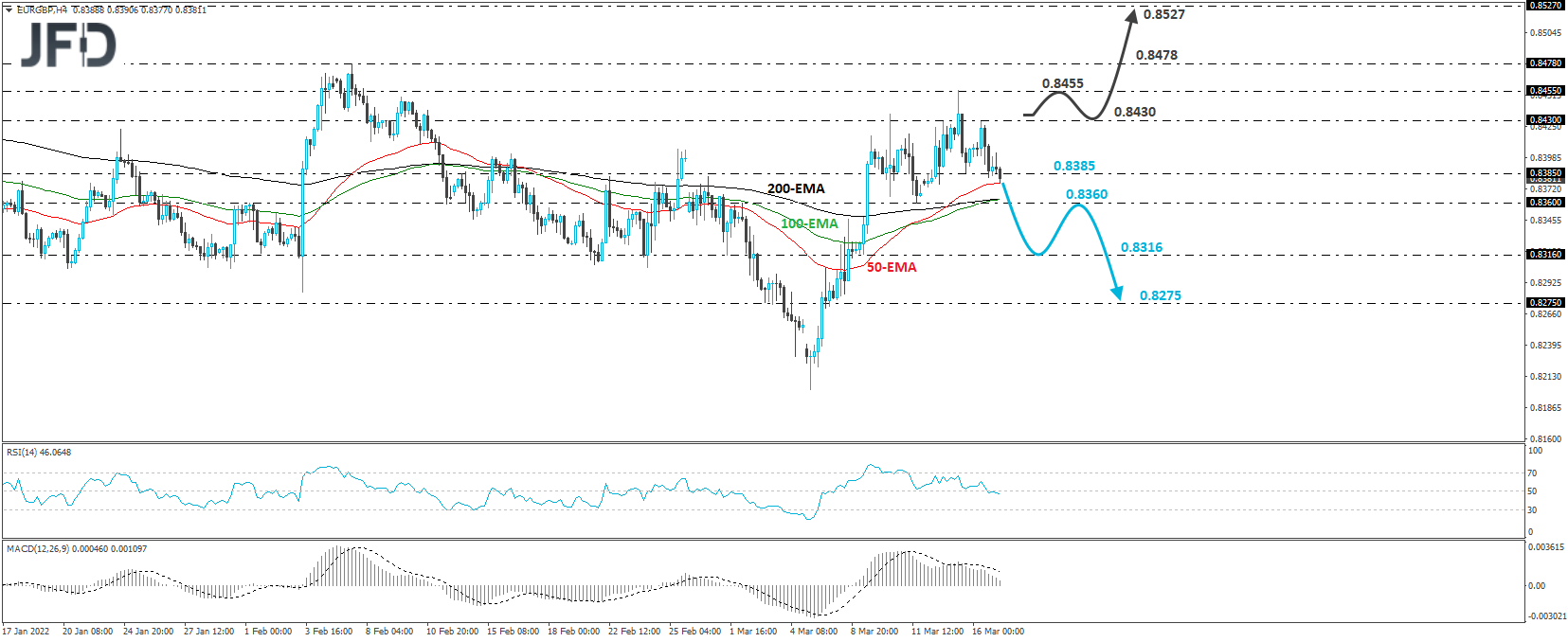

EUR/GBP – Technical Outlook

EUR/GBP traded lower yesterday, after hitting resistance at 0.8430. Although the prevailing short-term path was to the upside, the latest slide, combined with the negative divergence between the price action and both our short-term oscillators, suggests that the prior advance has run out of steam. Today, the rate fell below Tuesday’s low of 0.8305, and a dip below 0.8360, the low of Mar. 11, may be the reversal confirmation.

Such a break could wake up more bears, who may decide to push towards the low of Mar. 9, at 0.8316. If they are not willing to stop there either, then a break lower could carry more bearish implications, perhaps seeing scope for declines towards the 0.8275 area, marked by the low of Mar. 3, and near the low of Mar. 8.

The outlook could brighten again upon a break above yesterday’s peak of 0.8430. The next key resistance is Tuesday’s high, at 0.8455, the break of which could aim for the peak of Feb. 7, at 0.8478. Should the bulls manage to overcome that hurdle as well, we may see them climbing towards the 0.8527 area, marked by the highs of Dec. 16 and 17.

As For The Rest Of Today's Events

During the Asian session today, we already got Australia’s employment report for February, which came in better than expected, allowing Aussie traders to maintain bets over several rate hikes by the RBA this year.

Later in the day, Eurozone’s final CPIs for February are coming out, and as it is usually the case, they are expected to confirm their preliminary estimates, while from the US, we have the housing starts for the same month, which are forecast to have increased somewhat.

Tonight, during the Asian session Friday, we have another major central bank deciding on monetary policy, and this is the BoJ. However, with Japanese inflation still running well behind the rest of the world, we don’t expect any material changes. Once again, any reaction to the yen is likely to be insignificant. Japan’s CPIs for February are also coming out, with the core rate expected to inch up to +0.6% yoy, confirming the aforementioned statement.

From New Zealand, we get the GDP data for Q4, with the qoq rate expected to have rebounded to +3.4% from -4.7%, something that will take the yoy one up to +3.3% from -0.3%. At its latest gathering, the RBNZ lifted interest rates by another 25bps, to 1%, and also steepened its rate-path projections. So, with that in mind, a rebound in economic activity during the last quarter of 2021 may add credence to officials’ view and perhaps encourage Kiwi traders to add to their long positions.