Ulta Beauty, Inc. (NASDAQ:ULTA) , a leading beauty retailer in the United States, is slated to announce second-quarter fiscal 2017 earnings on Aug 24. In the preceding quarter, it came up with a positive earnings surprise of 6.7%.

In the trailing four quarters, the company outperformed the Zacks Consensus Estimate by an average of 4.2%. Let’s see how things are shaping up for this announcement.

Ulta Beauty Inc. Price and EPS Surprise

Ulta Beauty Inc. Price and EPS Surprise | Ulta Beauty Inc. Quote

What to Expect?

Investors are keen on finding out whether Ulta Beauty will be able to continue its positive earnings surprise streak in the quarter to be reported. The current Zacks Consensus Estimate for the quarter under review is $1.78, reflecting a 24.1% growth year over year. We note that the Zacks Consensus Estimate has been stable in the last 30 days. Further, analysts polled by Zacks expect revenues of $1.29 billion, reflecting an increase of 20.4% from the year-ago quarter.

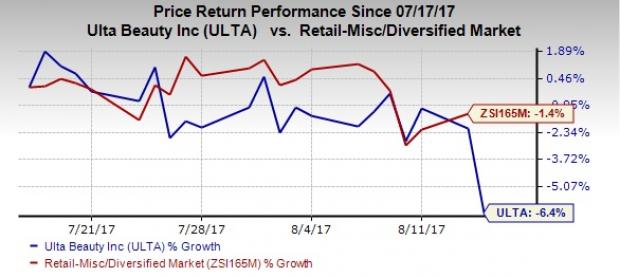

Furthermore, we note that the stock has underperformed the industry in the last one month. The company’s shares have declined 6.4%, while the industry dipped 1.4%.

Factors at Play

Ulta Beauty is lately troubled due to a slowing U.S. beauty market, which has become challenging since January. The mass market and department stores have been put under pressure, which remains a concern for Ulta Beauty. Moreover, the company remains on the backfoot due to limited global brand awareness, alongside challenges related to cheaper alternatives and changing consumer preference.

However, we commend Ulta Beauty’s splendid surprise history. The company has been gaining from constant merchandise innovations, solid marketing initiatives, outstanding e-Commerce improvement and continued progress at the salon operations. Notably, the company recorded a 70.9% growth in e-Commerce sales in first-quarter fiscal 2017. Further, the company’s raised fiscal 2017 view bodes well.

What the Zacks Model Unveils?

Our proven model does not conclusively show that Ulta Beauty is likely to beat estimates this quarter. This is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. American Eagle has an Earnings ESP of 0.00% as both the Most Accurate estimate and the Zacks Consensus Estimate are pegged at $1.78 per share. Further, the company carries a Zacks Rank #4 (Sell), which when combined with an ESP of 0.00% makes surprise prediction difficult. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Stocks Poised to Beat Earnings Estimates

Here are some more companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Burlington Stores Inc. (NYSE:BURL) currently has an Earnings ESP of +4.00% and a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Wal-Mart Stores Inc. (NYSE:WMT) currently has an Earnings ESP of +0.94% and a Zacks Rank #2.

Zumiez Inc. (NASDAQ:ZUMZ) has an Earnings ESP of +16.67% and a Zacks Rank #3.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce ""the world's first trillionaires,"" but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Zumiez Inc. (ZUMZ): Free Stock Analysis Report

Wal-Mart Stores, Inc. (WMT): Free Stock Analysis Report

Burlington Stores, Inc. (BURL): Free Stock Analysis Report

Ulta Beauty Inc. (ULTA): Free Stock Analysis Report

Original post