Dollar ticks down ahead of all-important US inflation data

Yen sinks, hits its lowest levels since 2008 against the euro

Energy prices go ballistic, stock markets and gold retreat

US inflation to disturb the waters

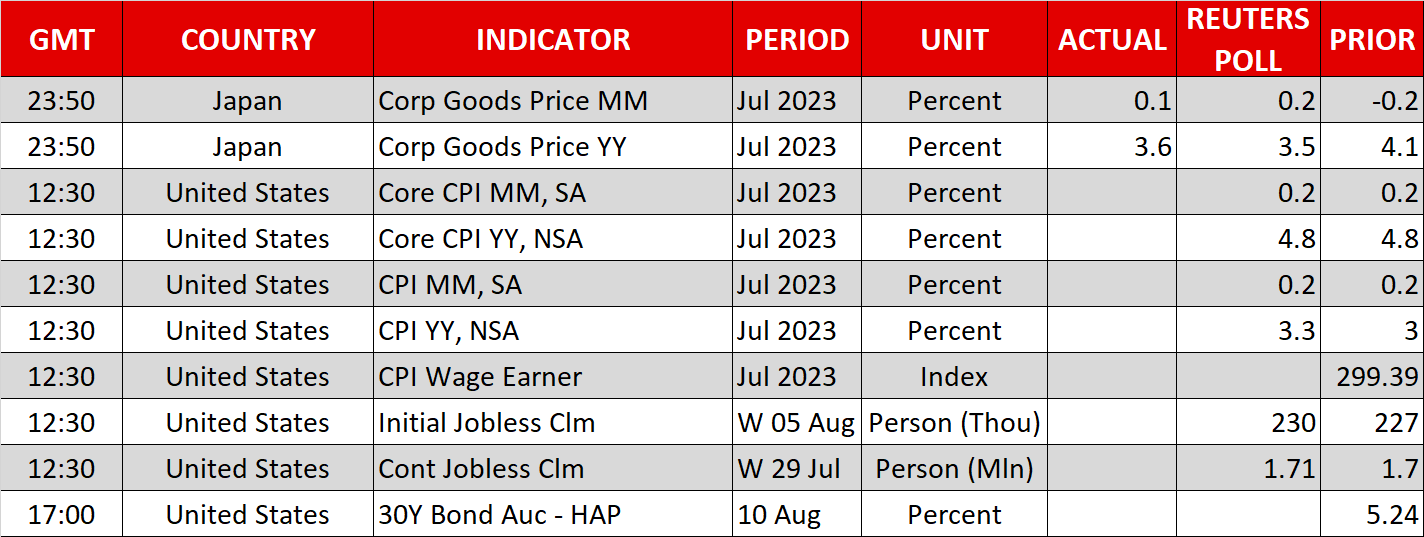

Global markets are holding their breath in anticipation of today’s US CPI inflation release. The stakes are high as this dataset will be critical in shaping expectations about the trajectory of interest rates. It could either cement the view that the Fed has already concluded its tightening cycle or bring this notion into doubt, driving the dollar and risk assets accordingly.

In July, forecasts suggest both the headline and core CPI rose by 0.2% in monthly terms. On a yearly basis, that would translate into an increase in the headline CPI to 3.3% from 3.0% previously, while the core rate is projected to hold steady at 4.8%.

As for any surprises, there is some scope for a hotter-than-expected CPI report. Gasoline and broad commodity prices shot higher in July, business surveys pointed to a reacceleration in price pressures, and rents are unlikely to cool materially with home prices hitting new record highs in much of the country.

Encapsulating these upside risks is the Cleveland Fed’s Inflation Nowcast model, which points to a monthly increase of 0.4% for both headline and core in July, far above the consensus of 0.2%. Even more worrisome is this model’s early estimate for August, which is currently tracking at 0.8% following a steep rise in energy prices.

Markets will likely react to a hot inflation report by pushing US yields higher, which would be a blessing for the dollar but a curse for assets such as stocks and gold that become less attractive as yields rise. On the flipside, colder-than-expected CPI readings could elicit the opposite responses, hurting the dollar while boosting equities and bullion.

Yen takes another beating, gold extends retreat

The Japanese yen has fallen victim to another selling wave, sinking to its lowest levels since 2008 against the euro. It’s been one-way traffic all week for the yen despite the nervous atmosphere in risk assets.

At the core of the yen’s troubles lie rising energy costs. Since Japan is a net-importer of oil and gas, the yen absorbs damage through the trade channel when energy prices rise. In addition, the slowdown in the nation’s wage growth seems to have dimmed the prospect of any further BoJ tightening, pushing Japanese yields down and dealing a secondary blow to the yen via rate differentials.

Gold also encountered some heavy selling this week, but the CPI report will be the deciding factor for the precious metal, which tends to move in the opposite direction of the dollar and yields. Hence, a hot inflation report could push bullion lower, turning the spotlight on the crucial $1,900 region, whereas lower-than-anticipated CPI readings could propel the metal higher towards the $1,935 resistance zone.

Oil storms higher, stocks remain shaky

Energy costs are going ballistic again. Oil prices are on the rise for a seventh consecutive week, hitting new multi-month highs in the process, while futures tracking European natural gas prices rose 28% yesterday amid concerns of supply disruptions.

While the demand outlook remains bleak as the world’s largest energy consumer - China - continues to lose steam, it appears supply conditions have gotten so tight after a series of production cuts from Saudi Arabia and Russia that prices have managed to find support. Whether this trend persists will have repercussions not just for energy markets but also for inflationary pressures, and therefore riskier trades as well.

Speaking of riskier trades, Wall Street pulled back yesterday, with the tech-heavy Nasdaq leading the decline as some air came out of Nvidia (NASDAQ:NVDA) shares (-4.7%). This year’s equity rally has been stunning because it has defied rising yields and declining earnings, resulting in valuations becoming increasingly expensive. Ergo, a lot of future optimism is already priced in, and reality needs to live up to these rosy expectations for these levels to hold.