Texas Instruments (NASDAQ:TXN) or TI’s second-quarter 2017 earnings and revenues came ahead of expectations.

Earnings of $1.03 per share surpassed the Zacks Consensus Estimate by 8 cents. Revenues of $3.7 billion beat the consensus mark by $139 million.

The strong results were driven by strength in auto, industrial, communications and personal electronics markets.

Texas Instruments continues to prudently invest its R&D dollars into several high-margin, high-growth areas of the analog and embedded processing markets. This is gradually increasing its exposure to industrial and automotive markets and increasing dollar content at customers, while reducing exposure to volatile consumer/computing markets.

Internally, the company has always executed rather well. It, along with chipmaker Intel (NASDAQ:INTC) , is one of the few semiconductor companies that depend on internal capacity for manufacturing the bulk of its devices. Since the company usually builds out capacity well ahead of demand, it is able to make opportunistic purchases. As a result, it is able to contain capex at up to 4% of sales even while on an expansion plan.

At the call, management stated that the company will remain focused on increasing free cash flow per share and strengthening competitive advantages. Notably, free cash flow over the past 12 months was $4.04 billion or 28.5% of revenues. Overall, we remain optimistic about TI’s compelling product line, the differentiation in its business and manufacturing efficiencies that include growing 300-millimeter Analog output.

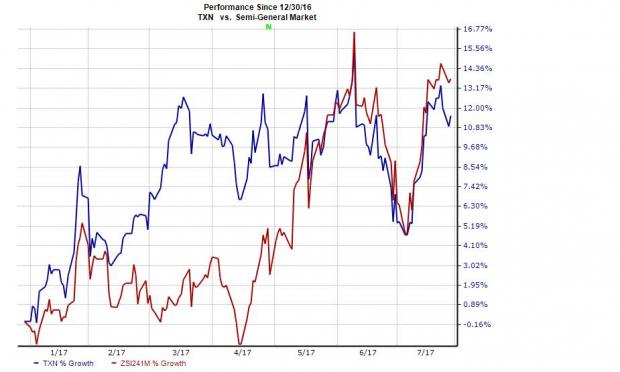

However, risks associated with a high debt level persist. Year to date, the stock has underperformed the industry it belongs to. It gained 11.5% compared with the industry’s gain of 13.8%.

Let’s see what the numbers say.

Revenue

Revenues were up 8.6% sequentially and 12.8% year over year and came at the higher end of the guidance range of $3.40 billion and $3.70 billion.

The automotive market continued to be strong. The company also saw broad-based improvement in the industrial market. The communications market and personal electronics grew well. Enterprise systems revenues were flat.

Growth of analog and embedded processing applications business was strong. It typically yields a more stable longer-lived business as well as strong margins. The Other segment declined. The company continues to return cash to investors in the form of share repurchases and dividends.

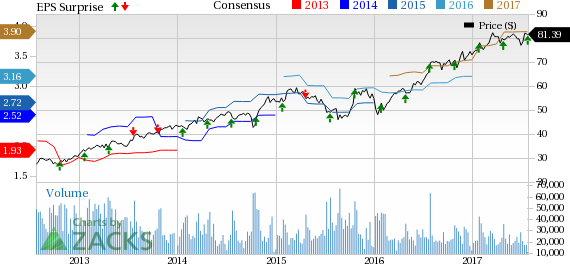

Texas Instruments Incorporated Price, Consensus and EPS Surprise

Texas Instruments Incorporated Price, Consensus and EPS Surprise | Texas Instruments Incorporated Quote

Segment Revenues

The Analog, Embedded Processing and Other Segments generated 65%, 24% and 11% of quarterly revenues, respectively.

The Analog business was up 6.9% sequentially and 18% from the year-ago quarter. The year-over-year growth was driven by strong performance in product lines - power and signal chain, and high volume.

The Embedded Processing segment, which includes processor, microcontroller and connectivity product lines, was up 8.1% sequentially and 15% year over year. The year-over-year growth was driven by stronger sales across all product lines - processors and connected microcontrollers.

The Other segment, which includes DLPs, custom ASICs, calculators, royalties and some legacy wireless products, was up 20.7% sequentially but down 14% year over year. The decline was mainly due to custom ASIC and royalties moving to other income and expenses beginning in the first quarter of 2017.

Margins and Net Income

Texas Instruments’ gross margin of 64.3% was up 126 basis points (bps) sequentially and 309 bps from the year-ago quarter. The company’s gross margin has been improving consistently as more production shifts to its 300mm line.

Operating expenses of $894 million were up 0.2% sequentially and 0.9% from the last year. Operating margin was 40.1%, up 327 bps sequentially and 595 bps from the year-ago quarter.

The Analog, Embedded Processing and Other segments generated operating margin of 29.2%, 7.3% and 11.2%, respectively. Analog, Embedded Processing and Other segment margin contracted 1220 bps, 2260 bps and 1120 bps, respectively on a sequential basis. Analog, Embedded and other segment margins however expanded 530 bps, 140 bps and 640 bps, respectively year over year.

Pro forma net income was $1.1 billion, or a 28.6% net income margin compared with 1 billion, or 29.3% in the previous quarter and $779 million, or 23.8% in the year-ago quarter.

Balance Sheet and Cash Flow

Cash and short-term investments balance was $3 billion, down $50 million during the quarter.

The company generated $917 million in cash from operations, spending $151 million on capex, $650 million on share repurchases and $498 million on cash dividends.

Texas Instruments is one of the few technology companies that return a significant amount of cash to investors. Over the trailing 12 months, the company returned 4.1 billion of cash through a combination of dividends and stock repurchases.

At quarter-end, TI had $3.1 billion in long-term debt and $499 million in short-term debt. As of Mar 31, 2017, the company’s net debt position was $599 million.

Guidance

The company provided guidance for the third quarter.

It expects revenues between $3.74 billion and $4.06 billion (up 5.4% sequentially at the mid-point). The mid-point of the guidance is higher than the Zacks Consensus Estimate of $3.8 billion.

The annual effective tax rate and the rate to be applied for the third quarter is around 29%.

Earnings for the quarter are expected to be in the range of $1.04 to $1.18 per share. The Zacks Consensus Estimate is pegged at $1.06 per share.

The capex target remains at 4% of revenues.

Zacks Rank & Stocks to Consider

Texas Instruments carries a Zacks Rank #3 (Hold). Better-ranked tocks in the broader technology sector include Alibaba (NYSE:BABA) and Lam Research Corporation (NASDAQ:LRCX) , each carrying a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Long-term earnings per share growth for Alibaba and Lam Research are projected to be 30.4% and 16.4%, respectively.

The Hottest Tech Mega-Trend of All

Last year, it generated $8 billion in global revenues. By 2020, it's predicted to blast through the roof to $47 billion. Famed investor Mark Cuban says it will produce "the world's first trillionaires," but that should still leave plenty of money for regular investors who make the right trades early.

See Zacks' 3 Best Stocks to Play This Trend >>

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

Intel Corporation (INTC): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Original post