I have no love for opinion masquerading as economic fact. Opinion is when there is little or no data in support of a conclusion. All too often, any economic "data" used is cherry picked (ignoring data points to the contrary) or anecdotal.

Follow up:

I was schooled as an engineer, and built mega-projects around the world. I have managed cash flows larger than some governments. Talking out of orifices would get you fired. What got me interested in economics was the complete lack scientific basis for the economic "facts" and opinion being espoused a distressing amount of the time.

Scientific evidence needs to be empirical and interpreted in accordance with scientific methods. Economics is a "science" void of enough hard data to have any scientific basis for many economic beliefs. This week Professor Paul Krugman stated:

In recent years many economists, including people like Larry Summers and yours truly, have come to the conclusion that growing monopoly power is a big problem for the U.S. economy — and not just because it raises profits at the expense of wages. Verizon-type stories, in which lack of competition reduces the incentive to invest, may contribute to persistent economic weakness.

I too believe monopoly power is a big problem for the USA and the global economy in general. We can correlate growing monopoly control by sector to a lot of bad effects (including impacts on employment, wage growth and taxes). But is monopoly growth THE cause or just an effect of an ignored root cause? Let's propose some root causes.

Campaign Finance Laws

One hypothesis is that the root cause of monopoly growth is collusion between big business and politicians. The same smell comes from powerful special interest groups (say labor unions, environmental groups, trade groups). Any group that contributes to politicians wants something - and special interest groups and big business are likely working against the public good, pursuing their own good. Big business contributes to politicians to protect and expand its turf . It takes money to get elected, and big business has money. If this hypothesis is correct, at least one root cause of monopoly growth is campaign financing laws.

Regulation

There could be a different hypothesis: Regulation is the root cause of monopoly growth. In protecting citizens, governments pass regulations. Could any Joe Smuck even think of manufacturing anything - or could he even open a lemonade stand - without jumping through interminable hoops? Layers and layers of regulations, licenses, and reports present a high hurdle for market entry. My opinion is that only the deepest pockets can successfully start a business. (Yah, I know there are exceptions.) Compliance with regulations is a relatively small part of product costs for big business. For Joe Smuck, compliance is an overwhelming cost and time burden. Compliance tilts the competitive scales toward big business, and adjusts the optimum point for economy of scale into monopoly territory. If it was NOT profitable - no business would want to grow into a monopoly. If this hypothesis is correct, a significant cause of monopoly growth is applying the same regulations regardless of size of the business.

Taxation

Another hypothesis is that monopoly growth is based on taxation. Big business has the power to move money around - to legally work the crevices in tax codes both domestically and internationally. The larger a company becomes, the more lawyers and wizards they can employ to avoid tax with an ever decreasing burden to the bottom line the larger the company becomes. Big business can throw a lot of money at tax avoidance. If this hypothesis is correct, a cause of monopoly growth is taxing all business at the same rate regardless of size.

I could keep throwing down hypothesis after hypothesis. Yes, monopolies work against the public good - but it has been difficult to effectively outlaw monopolies. A monopoly may be broken up, but the result is usually temporary. Time warp back to 1911 when Standard Oil was broken apart using antitrust laws. Today, we see the same kind of vertical, horizontal, and global integration in big business. Good luck in breaking the current monopolies up.

As for the rest of the Professor Krugman quote above, it is the old bait and switch technique. Start with a statement everyone believes is true, and then start attributing other bad things to the original statement. It is simply illogical that lack of competition reduces the incentive to invest. All business invests to increase profits - and hangs on to money when investments do not have adequate return.

I would propose a statement of general desirability: It should not be profitable to be a monopoly. I admit this may be debatable and expect some reader reaction.

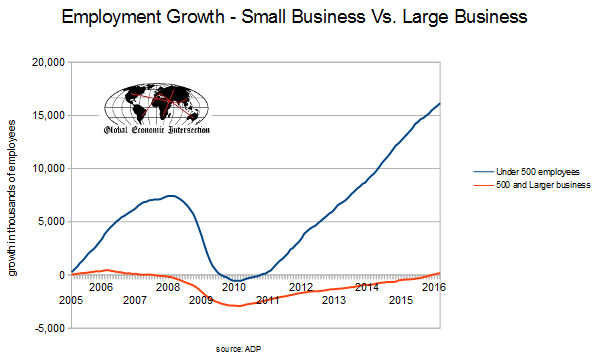

There may be debate about the relative value to consumers from multi-sourced competition vs. economies of scale for one (or a very few) large corporation(s). But my primary concern with big business monopolies is employment. Of course, not all big business is a monopoly - but data shows small business (defined as business which employs less than 500 people) is the employment driver. For employment growth to be maintained, the economy needs small business more than big business.

Simply put, big businesses employ people like me to streamline organization structures - optimizing the variables of cost, quality, technology, productivity and output. The goal of big business is to do more with less people. Small businesses are usually overwhelmed just managing expansion.

To emphasize my point, I conclude with the employment contribution of big business - see red line on graph below.

Other Economic News this Week:

The Econintersect Economic Index for April 2016 again insignificantly improved but remains relatively weak. The index continues near one of the lowest values since the end of the Great Recession. This marginal index improvement is due to data being compared against relatively soft data - both month-over-month and year-over-year. Our employment six month forecast is for slightly weaker employment growth for April - and the long term decline in the employment forecast remains in play.

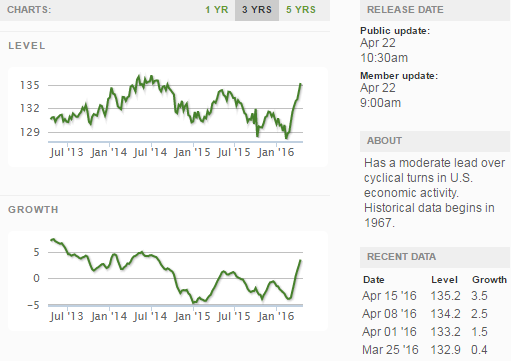

Economic Cycle Research Institute (ECRI) Weekly Leading Index (WLI) Growth Index is now in positive territory and forecasting a marginally strengthening economy six months from now.

Current ECRI WLI Growth Index

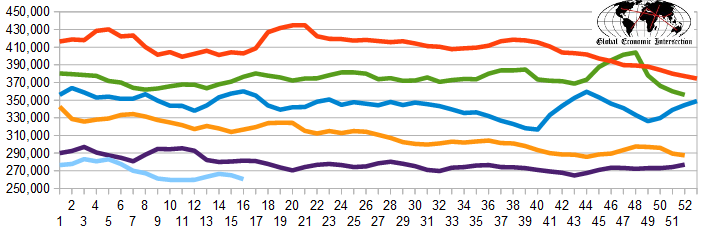

The market expectations for weekly initial unemployment claims (from Bloomberg) were 261,000 to 280,000 (consensus 265,000), and the Department of Labor reported 247,000 new claims. The more important (because of the volatility in the weekly reported claims and seasonality errors in adjusting the data) 4 week moving average moved from 265,000 (reported last week as 265,000) to 260,500. The rolling averages generally have been equal to or under 300,000 since August 2014.

Weekly Initial Unemployment Claims - 4 Week Average - Seasonally Adjusted - 2011 (red line), 2012 (green line), 2013 (blue line), 2014 (orange line), 2015 (violet line)

Bankruptcies this Week: Goodrich Petroleum, SunEdison (fka MEMC Electronic Materials)

Click here to view the scorecard table below with active hyperlinks

Weekly Economic Release Scorecard: