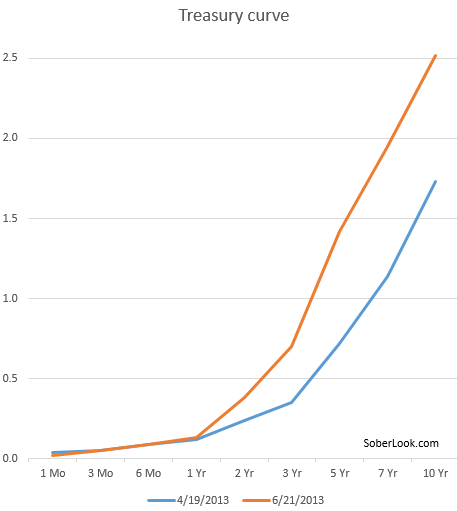

The treasury curve has steepened materially over the past few weeks, driven by Bernanke's seemingly hawkish statements. One group of companies that will benefit from this adjustment is the banking sector.

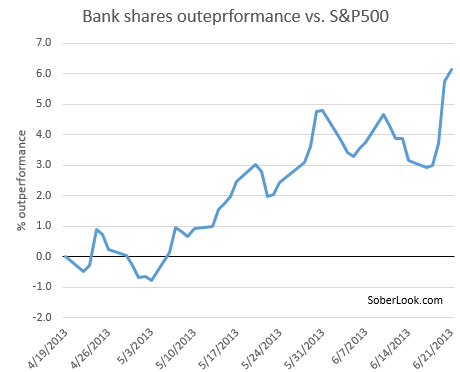

In fact bank shares have been outperforming the broader market by a significant margin - over 6% in the past couple of months.

The reason is simple. Given the short end of the curve has not budged, banks will continue to pay next to nothing on deposits. But they can now charge much higher rates on new term loans they make. That spread increase (net interest income) will flow right into equity and juice up bank dividends. Bank shareholders and executives should be thanking Bernanke.

But there are headwinds appearing on the horizon for the banking sector that may negate some of these gains. Here are a few examples:

1. A portion of bank revenue has been generated from mortgage refinancing in the past couple of years. But that game is over and the refi fee revenue will no longer be there. We'll let our friends who analyze bank shares quantify that number, but it can't be immaterial.

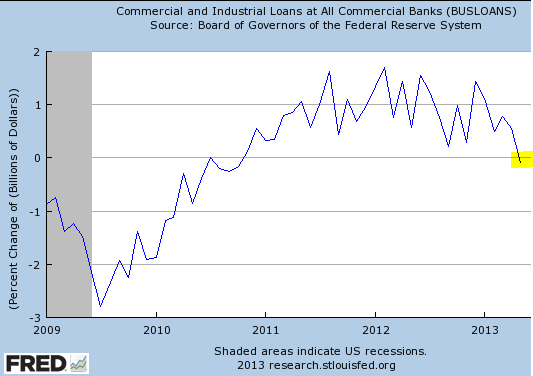

2. With rates rising, loan demand in the corporate sector may in fact decline. We are already seeing evidence of that.

On top of reducing origination fees and asset growth for banks, this trend could easily result in slower economic growth, which has been quite fragile to begin with.

3. Treasury and agency securities make up about 10% of bank assets. Even though not all of these securities will get marked to market, the recent bond correction can't be good for the old P&L. Customer flows in fixed income departments of banks will also decline materially.

4. New regulatory pressures could create tremendous headwinds for the larger banks, and could even result in dividends being shut off for years to come as banks are forced to build up capital.

Bloomberg: U.S. regulators are considering doubling a minimum capital requirement for the largest banks, which could force some of them to halt dividend payments.

The standard would increase the amount of capital lenders must hold to 6 percent of total assets regardless of their risk, according to four people with knowledge of the talks. That’s twice the level set by global banking supervisors.

For those who think banks haven't been lending enough, just wait till such rules go into effect. We will see an outright credit contraction in the U.S.

Given these headwinds in the banking sector, one should be careful jumping on the bank shares bandwagon. There may be some nasty earning surprises along the way. With banks under pressure, those who are predicting the U.S. GDP to grow at 2.5% or higher should go back to the drawing board.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Steepening Yield Curve Benefits Banks, But Major Headwinds Remain

Published 06/23/2013, 02:11 AM

Updated 07/09/2023, 06:31 AM

Steepening Yield Curve Benefits Banks, But Major Headwinds Remain

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.