On Jul 5, 2016, we issued an updated research report on DaVita HealthCare Partners Inc. (NYSE:DVA) .

Davita remains well poised for long-term growth supported by its consistent service upgrades, global expansion initiatives and strategic acquisitions. These efforts of the company are in turn backed by its strong financial position.

Davita regularly undertakes strategic acquisitions and mergers to bolster its client base and augment its primary care, specialty physician, hospital and other healthcare services. The insurer is expected to engage in more acquisitions and alliances going forward as uncertainties related to the bundling rule and the capital markets have eased.

Over the past few years, Davita has turned its focus toward emerging and developing markets to expand its its global presence. This strategy of the company has been brought to light by the recent alliances as well as acquisitions of dialysis centers Collaborations with local hospitals should also boost Davita’s competitive advantage and operating leverage.

In its efforts to focus more on cost efficiencies through various deals and alliances, Davita expects its seven-year Epogen purchase deal with Amgen Inc. (NASDAQ:AMGN) to eventually receive various discounts and rebates over the tenure of the agreement and also limit Amgen’s ability to increase Epogen’s price without the consent of DaVita.

Davita boasts a solid financial position with a strong operating cash flow owing to improved earnings, robust cash collections and the timing of payments for working capital expenditures. The strong cash flow enables the company to meet its capital expenditure needs and spend handily on acquisitions. The company expects operating cash flow of about $5.5 billion over the next three years. Of this, the projected amount for 2016 lies between $1.55 billion and $1.75 billion.

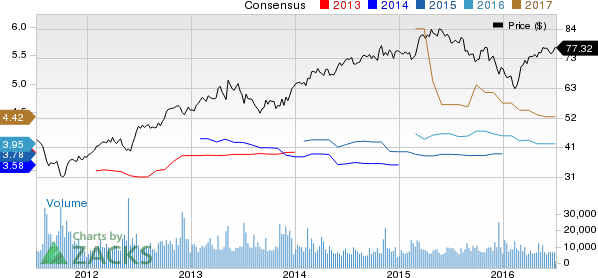

All these together make Davita, the leading dialysis service provider in the U.S., and an attractive pick for the yield seeking investors. The company’s expected long-term growth rate is currently pegged at 10.6%. In fact, the Zacks Consensus Estimate moved up 3% to $3.90 for 2016 and 11.9% to $4.42 for 2017 over the last 90 days.

However, inclination toward government medical insurance scheme poses a challenge for Davita. The overall increase in Medicare Advantage beneficiaries in the U.S. is creating additional pressure on the company’s profitability as inadequacy of government reimbursements could force it to close a number of centers. Also, the new Medicare screening procedure delays the overall reimbursement process. Factors like these are likely to affect earnings and cash flows adversely.

The company’s debt refinancing continues to keep DaVita’s financial leverage at high levels. The company depends upon future borrowings to service its debt and fund other liquidity needs. DaVita may face difficulties in expanding its business, taking advantage of business opportunities, dealing with competitive pressures or refinancing maturing debt. Any increase in debt obligations may further increase the company’s interest expenses and adversely affect earnings and cash flow and its ability to service debt.

The impact of the health care reform legislation could also hurt DaVita’s earnings. The establishment of health insurance exchanges has already reduced the number of policyholders opting for commercial insurance, thereby posing a threat for Davita.

Investors interested in medical sector can also look at LHC Group, Inc. (NASDAQ:LHCG) and PharMerica Corporation (NYSE:PMC) .

AMGEN INC (AMGN): Free Stock Analysis Report

DAVITA HEALTHCR (DVA): Free Stock Analysis Report

LHC GROUP LLC (LHCG): Free Stock Analysis Report

PHARMERICA CORP (PMC): Free Stock Analysis Report

Original post

Zacks Investment Research