- Strong China factory data boosts equities but rate hike fears limit gains

- Dollar pulls back, euro climbs as ECB starts QT

- Aussie and loonie up on China optimism but soft GDP numbers weigh

Markets buoyed as China reopening boost starts to materialize

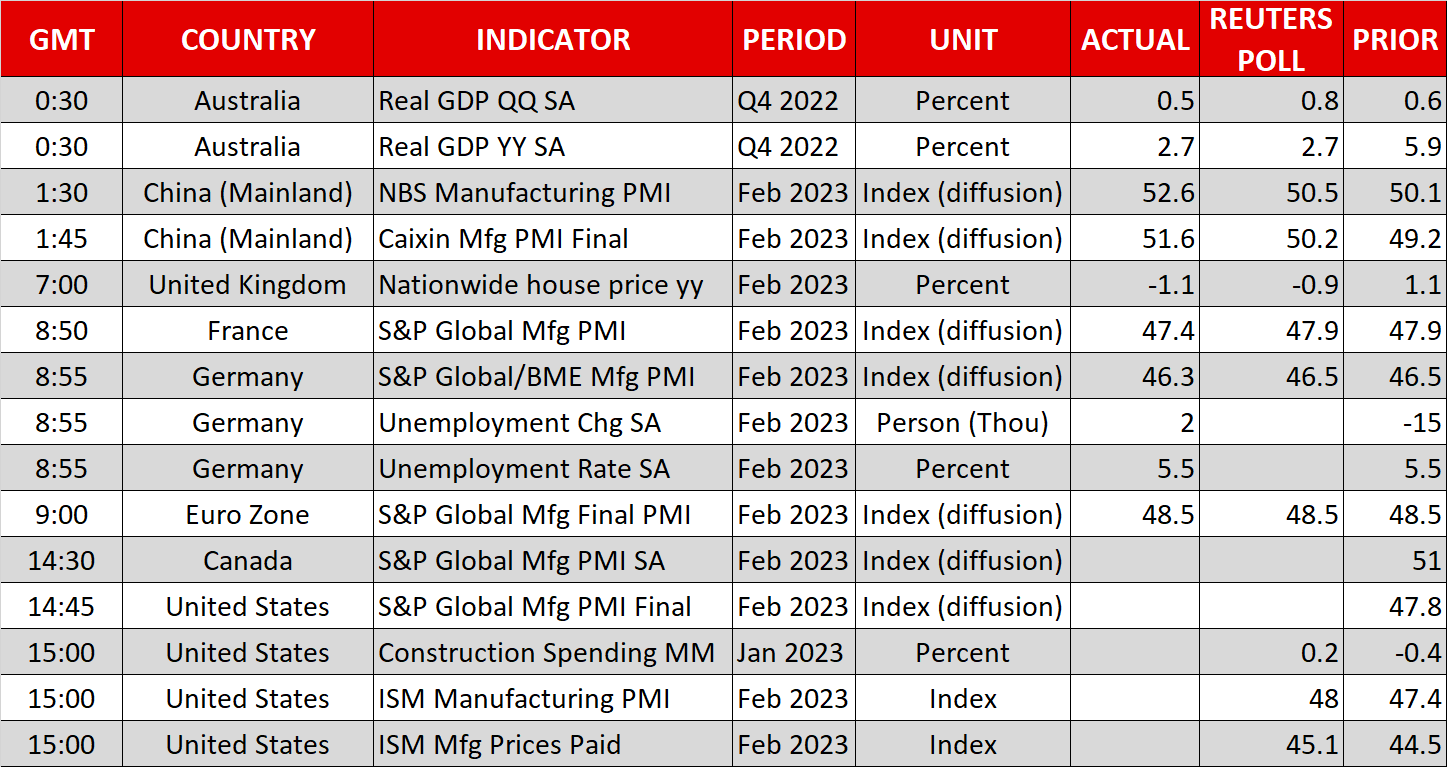

After ending February on a sour note, equity markets started the new month in a cheerier mood with the help of some much-needed positive headlines from China. Manufacturing activity in the world’s second largest economy grew at the fastest pace in more than a decade in February. Both the official and Caixin PMI readings topped expectations, in the strongest sign yet that demand and supply are being fully restored following the lifting of all Covid restrictions in December.

Hong Kong’s Hang Seng index rallied the most on the back of the upbeat data, surging by more than 4%, while China’s benchmark CSI 300 index jumped 1.4%.

The initial tepid pickup in the economy had raised some concerns about how long it would take for the full effects of the reopening to transpire so it’s very encouraging for investors to see that the recovery is well under way.

Nevertheless, there is still some caution as the pent-up demand could fade quite quickly amid other woes facing the Chinese economy.

Positive start to March for stocks after February losses

For global investors, any positive takeaway from China has to be weighed against the angst about central banks overreacting to the inflation threat and causing a hard economic landing. Those lingering risks are holding back the gains in Europe and the US.

Apart from London’s FTSE 100, which is benefiting from a rally in mining stocks, shares elsewhere are up modestly and US e-mini futures are only marginally in positive territory.

All of Wall Street’s main indices ended February in the red as traders were forced to reassess how many more times the Fed will raise rates in 2023 following a series of stronger-than-expected US data, including on inflation. However, this week’s releases have been rather mixed, adding to the uncertainty about whether or not US growth is slowing or accelerating.

Investors will be hoping that the ISM manufacturing PMI due later today will shed some more light on the state of the American economy.

Euro heads higher on CPI data and QT

In the meantime, bond yields continue to edge up, with Eurozone yields in particular racing higher as the European Central Bank begins running down its balance sheet today. The start of quantitative tightening is a major test for the ECB, whose holdings now exceed €5 trillion after years of asset purchases.

But the uptick in yields is likely a reaction to yesterday’s hotter-than-expected flash CPI figures out of France and Spain ahead of tomorrow’s Eurozone ones. The various regional German CPI readings are so far not pointing to the same upside surprise, but nevertheless, expectations for the ECB’s terminal rate have risen to fresh highs on Wednesday and are fast approaching 4%.

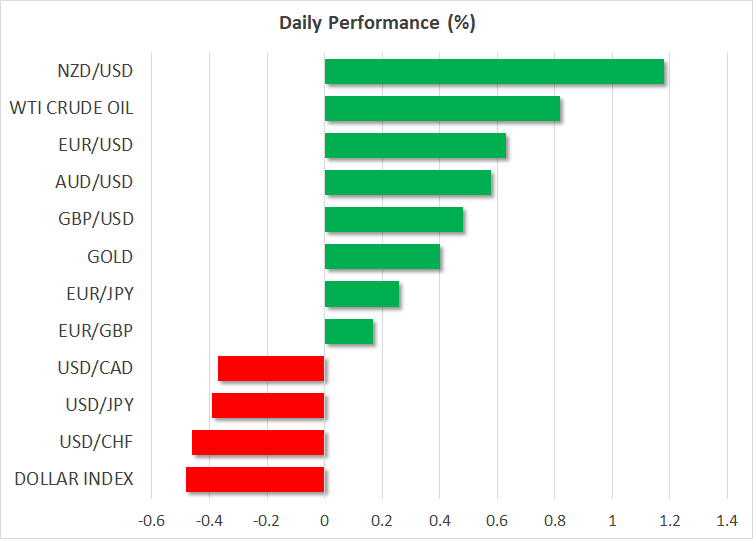

This is giving the euro a significant leg up against the US dollar, hitting a one-week high of $1.0657 earlier in the session. The pound was also up, resuming its advance from Monday when it was boosted from the UK and EU resolving their dispute over Northern Ireland after the rebound was cut short yesterday from an attempted comeback by the dollar.

But the greenback is on the backfoot today as risk sentiment improves and the yen is mostly weaker too.

Kiwi shines, but aussie and loonie lag after GDP misses

Among the commodity-linked currencies, the New Zealand dollar is leading the gains by a wide margin. The optimism around the recovery in Chinese demand is likely driving the risk-sensitive aussie, kiwi and loonie higher. But with the Bank of Canada pausing its rate increases and question marks about how much further the Reserve Bank of Australia will tighten, only the kiwi is able to stage a solid rally today.

Canada’s economy did not grow at all in the last quarter of 2022, underscoring the BoC’s plans to pause, while Australian GDP growth for the same period also disappointed today, prompting investors to pare back some of their more hawkish bets on the RBA.

If it wasn’t for the GDP miss, the Australian currency would probably have soared after the Chinese PMI numbers, though this does not necessarily imply that RBA policy will be affected much by the softer-than-anticipated data.