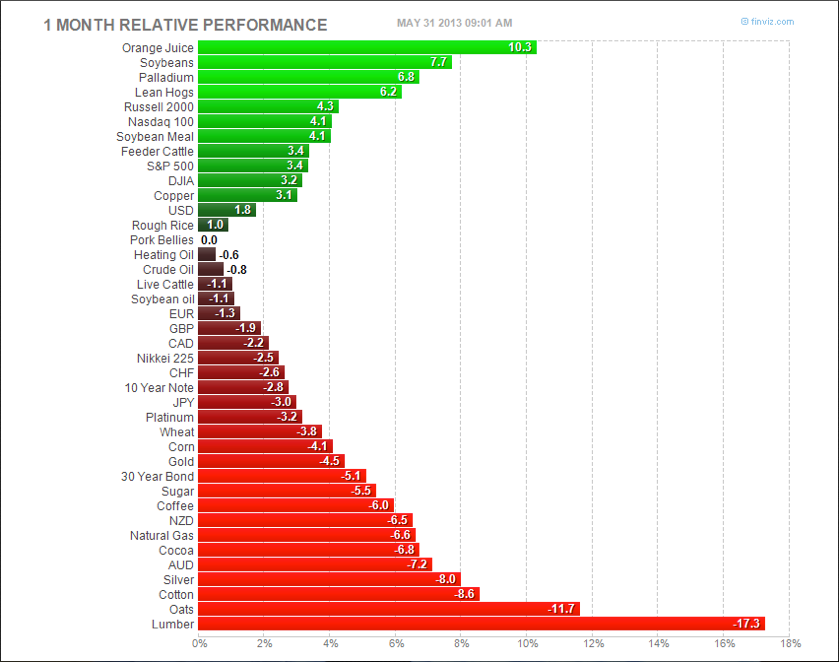

Well...If your inclination was to sell Lumber or the Precious Metals or any currency other than the U.S. Dollar, you would have done well. However, the Teflon Rally continues for U.S. Equities.

Here are the past Monthly closes/moves for the S&P futures (ESM13):

- 3/12: 1378.50

- 4/12: 1368.50 (0.007%)

- 5/12: 1283.25 (6.2%)

- 6/12: 1336.50 (4.2%)

- 7/12: 1353.75 (1.3%)

- 8/12: 1384.00 (2.2%)

- 9/12: 1420.00 (2.6%)

- 10/12: 1393.00 (1.9%)

- 11/12: 1401.00 (0.006%)

- 12/12: 1413.25 (0.009%)

- 1/13: 1486.75 (5.2%)

- 2/13: 1507.50 (1.4%)

- 3/13: 1562.75 (3.7%)

- 4/13: 1592.25 (1.9%)

- 5/13: As of right now 1650.00 (assuming we close here... +3.6%)

- 3 Down months w/ average drop of (2.7%)

- 11 Up months w/average gain of 2.4%

- Since March 2012 close S&P futures up 19.7%

The other side of the coin is that US interest rates are starting to move higher....and the move we saw this month was considerable.

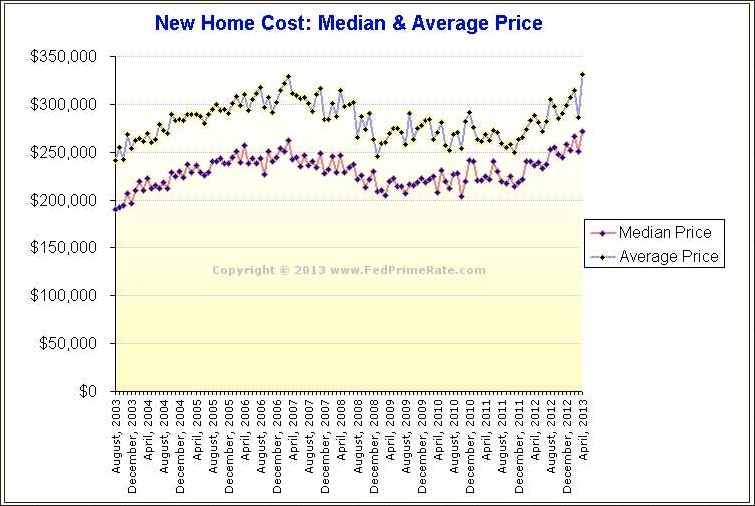

As I've mentioned regularly, Housing and it's adjunct businesses (lending/materials/construction/etc) is critically important to the "recovery story".

Mortgage buyer Freddie Mac says the average rate for the 30-year loan rose to 3.81%, up from 3.59% last week. That's still not far from the 3.31% rate reached in November, the lowest on records dating to 1971.

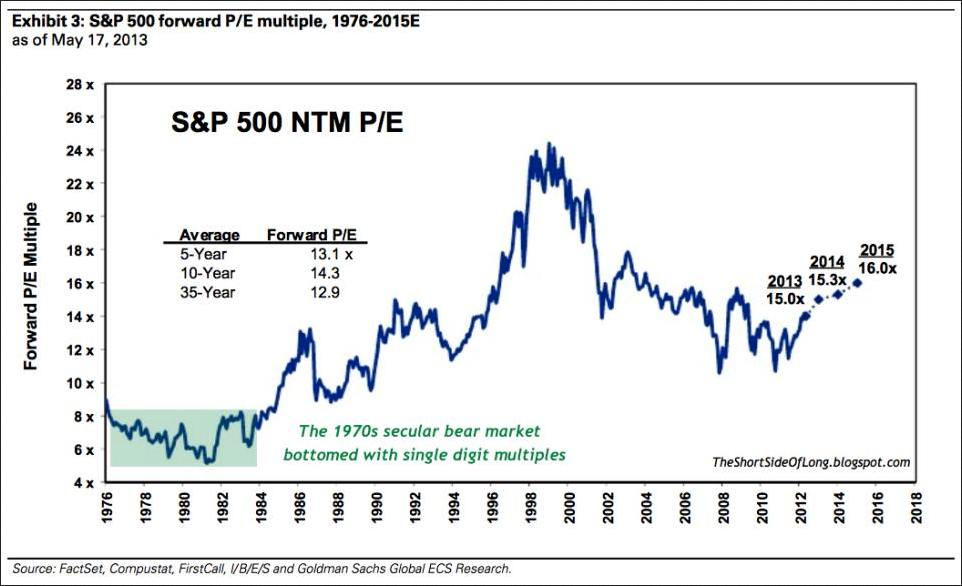

Let's evaluate some recent information from the Fed.

Avg. New Home Price in April 2013 = $330k (November of 2007 was $317k.....so are homes cheap?) No, but RATES ARE VERY (artificially?) low which makes borrowing to buy things (leverage) attractive. Median Home Price in Nov 2007 = $250k, last month it was $272k.

Guess what Funds/Private Equity have been doing for the past two years and it's reaching a fever pitch -- buying property and flipping it/renting it out.

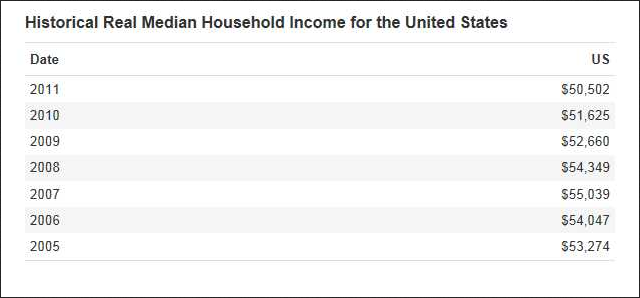

Here's a look at US Median Household Income:

In 2007, we had a median household income of $55k ($4,580/month). In 2011, we had a median household income of $51k ($4,250/month).

I'm not intent on being contrarian, and I believe the Housing Recovery is a great story, but it's all predicated on CHEAP MONEY. The cause of and solution to every problem since Long Term Capital Management went belly up in September of 1998.

If rates continue to move higher (and they should because the longer you suppress a market the more violent the eventual move could be....) the collateral damage could be considerable.

From my standpoint, I believe the Fed is well aware of that and will do anything they can to avoid deflation by continuing to buy Treasuries and MBS. The taper story is an interesting one and the CME is doing record volume in the Financials because of it (next FOMC meeting June 18 - 19), but at the same time, they continue to expand their balance sheet.

In other news, Lumber has rebounded smartly after a 32% selloff.

And finally, the Gold Silver ratio is back to 62 (you could buy 62 ozs of Silver or 1 oz of Gold) which has been the point where Silver tends to outperform lately.

There was a very strong Chicago PMI number this morning which put a bid in the Dollar and pressure on Commodities.

If Crude Oil (WTI) trades below $91 I would look for a place to get long deltas (Long future with a stop or sell puts at a level you would be comfortable owning).

Alternatively, if RBOB (gasoline) trades below 2.75 I would sell puts.

Yesterday with some clients we sold strangles in front month Natural Gas.

Implied vols. in the Precious Metals (particularly Gold) came in considerably over the past two-three sessions.