- OPEC meets today, supply decision could impact euro and stocks too

- Dollar supported by solid US data and rising yields, sterling tumbles

- Gold defies fundamental drivers, Swiss franc jumps on inflation data

Beyond oil

The world’s dominant oil cartel will convene today to decide on production targets. This is the most important OPEC meeting in a year and the outcome could have far-reaching implications for several asset classes as the global economy grapples with the hardest energy shock in decades.

There’s been a dramatic change in tone from OPEC lately, with Saudi Arabia appearing willing to ramp up production to help cool oil prices. This shift has the White House’s fingerprints all over it, with President Biden even considering a visit to Saudi Arabia soon in a last-ditch attempt to offer struggling consumers some relief and avert a shellacking for the Democrats in the US midterm elections.

Reports around what OPEC might do have been mixed. Some stories suggest no policy changes have been discussed, while other sources suggest the cartel could bring forward some production increases that were scheduled for later in the year. Speculation alone has knocked oil prices down this week, because ultimately, why would OPEC make such a fuss about boosting supply and then do nothing?

Any signs that OPEC is finally willing to put a ceiling on oil prices would mean less threat of inflation running wild, less need for aggressive central bank tightening, and less recession risks - which would be music to the ears of riskier assets like stocks. It would also be good news for energy importing currencies such as the euro and Japanese yen.

Dollar gains, loonie flat, sterling down

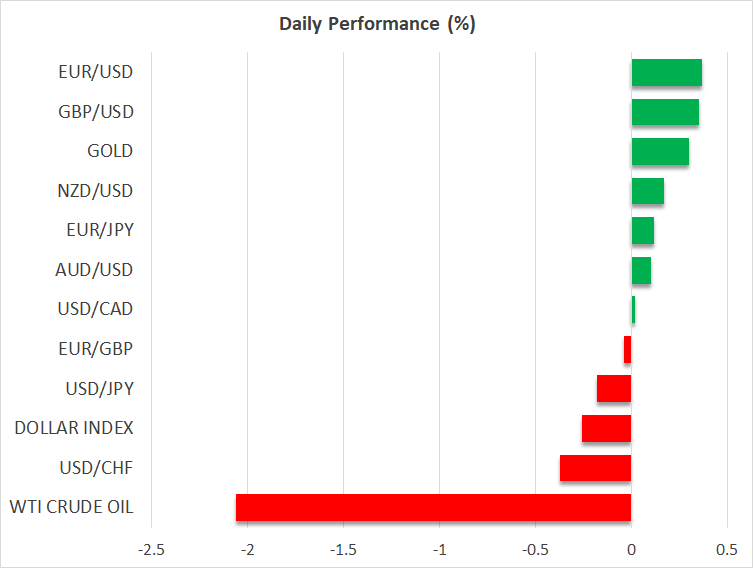

Over in the FX arena, it was another episode of the dollar trampling over its competitors with a little help from solid US data and rising Treasury yields. Yesterday's ISM manufacturing PMI had something for everyone, with the employment index falling into contractionary territory but the new orders index jumping, calming some nerves about a sharp economic slowdown.

The Bank of Canada raised interest rates and warned that it is prepared to act more forcefully, yet the loonie could not rally in the aftermath. Instead, it was pinned down by an even stronger US dollar and softer oil prices.

Meanwhile, the British pound slipped on another banana peel. Sterling remains hostage to any moves in stock markets, with the 60-day rolling correlation between Cable and the S&P 500 standing at an astonishing 0.89 currently. The pound has essentially turned into a proxy for global risk sentiment.

Gold shines, franc climbs

Gold prices came back swinging yesterday, erasing some early losses to close in the green despite a stronger US dollar and a spike higher in real yields - both factors that are typically detrimental for bullion. Safe-haven demand seems to have returned, although if the upward trends in the dollar and yields persist, the yellow metal might not be able to resist gravity for long.

Elsewhere, the Swiss franc is back in the spotlight after another acceleration in the nation’s inflation. This provides the Swiss National Bank the perfect cover to begin raising interest rates later this year, although the current market pricing seems way too aggressive as it implies the hiking cycle is likely to begin this month already. SNB officials haven't even shown any signs this is under consideration so far, leaving scope for some short-term disappointment in the franc.

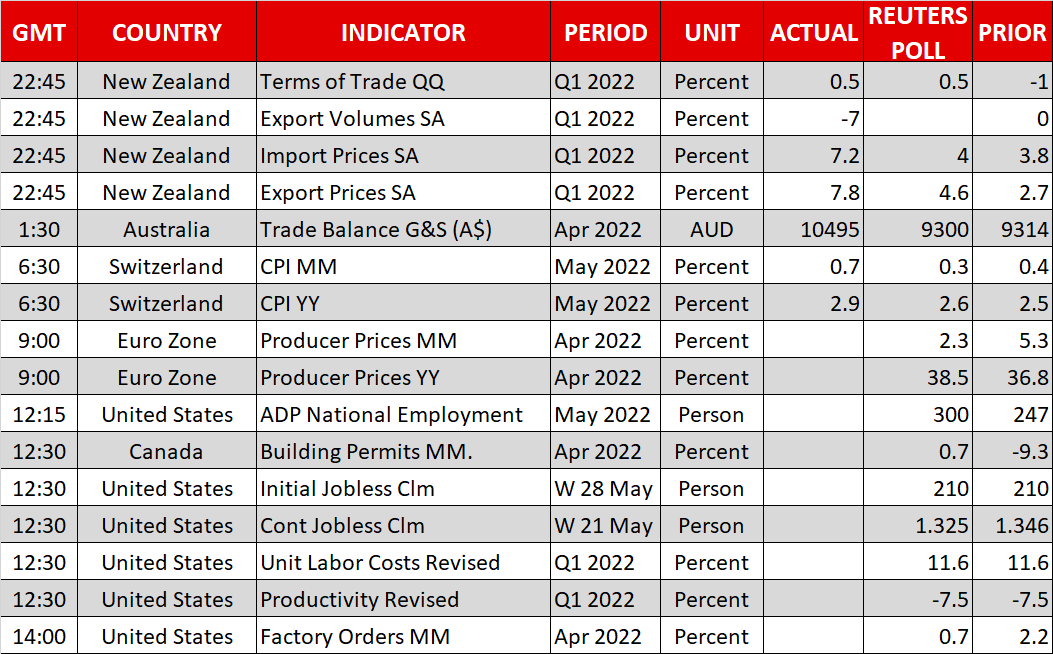

Finally, the ADP jobs report was delayed until today and investors will pay close attention ahead of tomorrow’s edition of nonfarm payrolls.