- Fed minutes dent hopes of early rate cut but markets perk up anyway

- Higher services PMIs lift sentiment in Europe and Asia, boosting US futures too

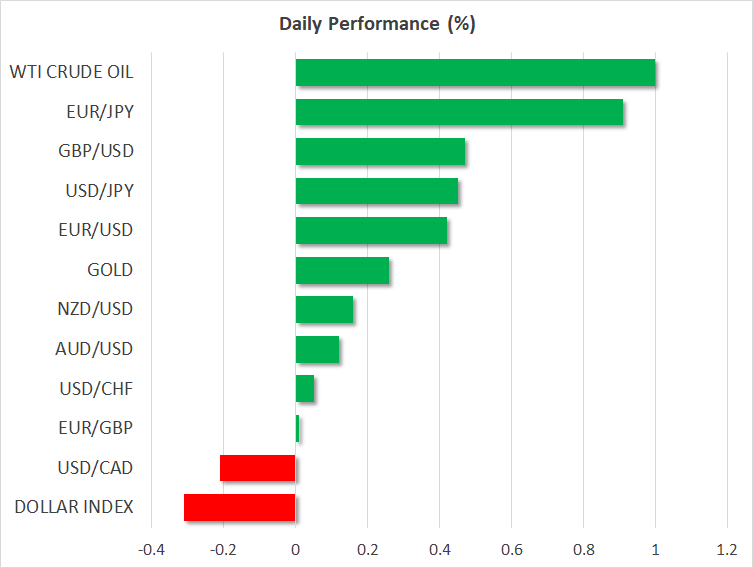

- Dollar rebound pauses for breath, oil jumps on supply concerns

Fed rate cut bets little changed after December minutes

Markets wavered after the Fed published the minutes of its December policy meeting on Wednesday as investors weighed the prospect of rate cuts amid mixed signals from policymakers. The minutes gave no indication that rate cuts were imminent, emphasizing the need to maintain restrictive policy for “some time”. There was also no change from the statement about the possibility of further rate increases. But investors jumped on the dovish segments of the minutes where policymakers acknowledged that “clear progress” had been made in bringing inflation down, which would warrant lower rates by the end of 2024.

But the real surprise in the minutes wasn’t so much the views on interest rates but on the balance sheet, as several committee members appeared to favour an early end to quantitative tightening, preceded by a slowdown in the runoff pace.

The 10-year Treasury yield took a dive after the minutes, dropping below 3.90%, having tested the 4.0% level ahead of it. The moves in bond yields came even as rate cut expectations for 2024 were scaled back only slightly.

Stocks show signs of life after upbeat services PMIs

On Wall Street, however, the major indices extended their decline, with the S&P 500 falling for the third straight session. It’s likely that profit taking was still at play on Wednesday as the FOMC minutes weren’t as dovish as investors had hoped. But there’s also some angst about the upcoming earnings season, highlighted by the downgrade in Apple (NASDAQ:AAPL) stock by Barclays yesterday, although it was Tesla (NASDAQ:TSLA) that led the losses in the tech sector by slumping as much as 4%.

But the mood seems to have improved overnight as Asian markets started the day in positive territory before turning negative, though European shares are so far holding onto their gains.

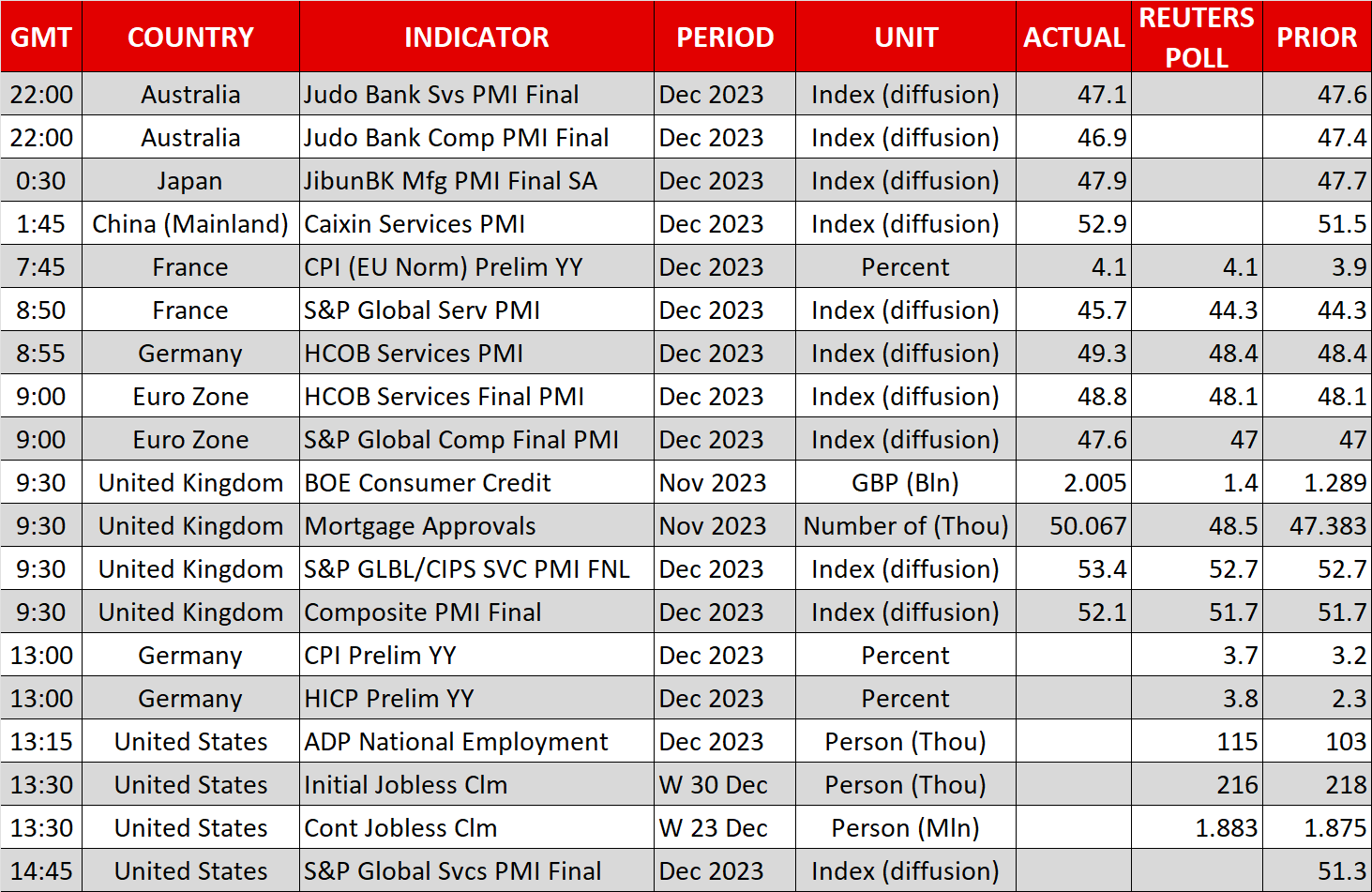

A better-than-expected reading in China’s Caixin services PMI is contributing to the somewhat brighter mood on Thursday, while the Eurozone’s and UK’s services PMIs were revised higher in the final estimates, easing fears about a deteriorating economic outlook.

In the US, however, there is some uncertainty about where the economy is headed. Job openings according to yesterday's JOLTS data fell for the third month in a row in November, but the latest ISM manufacturing PMI was stronger than expected.

This puts all the more focus on tomorrow’s nonfarm payrolls report and the ISM’s non-manufacturing gauge, making a meaningful rebound in equities unlikely before then. US futures were marginally higher during European trading.

Setback for dollar bulls, yen struggles too

The positive surprise in European services PMIs helped the euro and pound to rebound against the US dollar and the risk-sensitive aussie also managed to halt its slide.

Against a basket of currencies, the greenback turned red, ending four consecutive days of gains. But the worst performer was the yen, as the Japanese currency came under pressure on doubts as to whether the Bank of Japan would be able to exit negative rates while the country recovers from the damaging earthquake on New Year’s Day.

Oil rises to one-week high

In commodities, gold edged higher for the first time this year, as the dollar slipped, and oil prices were higher too. Crude oil has found support lately from increased tensions in the Middle East amid the crisis in the Red Sea that’s threatening shipments along the route. Protests at a major oilfield in Libya that’s led to its shutdown are also inflicting upside pressure on oil, while there was a further boost on Wednesday from a large drawdown in US crude stocks according to API figures. The official EIA inventory data is due later today.

All this, along with the broader improvement in risk sentiment drove oil prices to one-week highs on Thursday, with WTI and Brent futures climbing more than 1%.