Earlier this month, I shared with you a quote from Arnoud Balhuizen, chief commercial officer of BHP Billiton (LON:BLT), the largest mining company in the world. In a September interview with Reuters, Balhuizen called 2017 the “revolution year [for electric vehicles], and copper is the metal of the future.”

Balhuizen’s assessment couldn’t be more accurate, and the implications for investors is too compelling to ignore.

In the third quarter, global sales of electric vehicles (EVs) soared 63 percent compared to the same period last year, 23 percent compared to the second quarter. A total of 287,000 units were reportedly sold in the September quarter, leading Bloomberg New Energy Finance to project total annual sales to exceed 1 million units for the first time.

As the world’s largest auto market, China was responsible for about half of the sales as the crackdown on polluting industries has propelled renewable alternatives from power generation to consumer products.

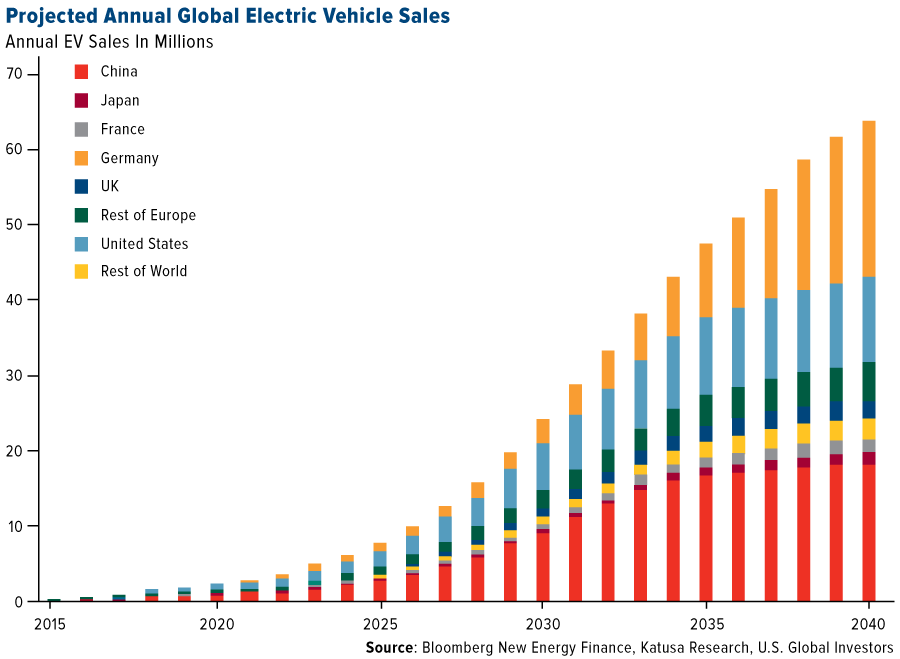

60 Million Electric Cars by 2040?

This is only the beginning. The chart below, highlighted by Katusa Research and originally provided by Bloomberg New Energy Finance, takes a look at annual global EV sales forecasts through the year 2040. As you can see, China, the U.S. and Germany will push the adoption of EVs forward, with the rest of the world following closely behind. Many analysts believe that by 2040, the global EV market could exceed 60 million vehicles sold per year.

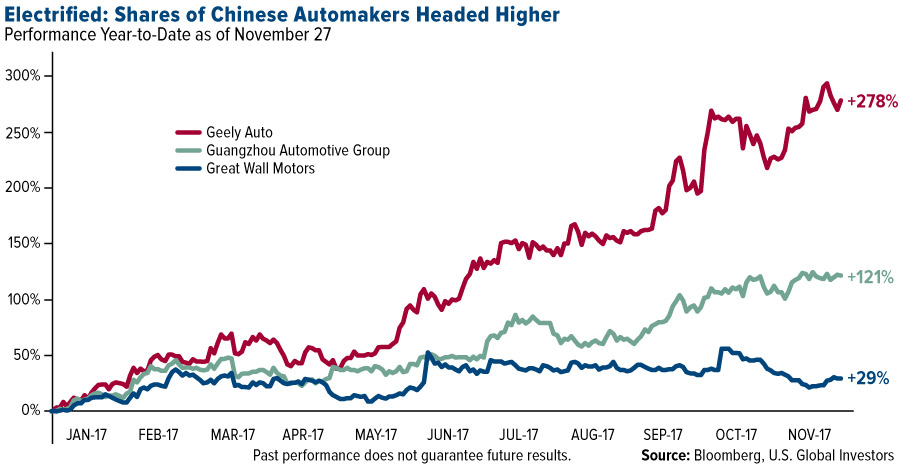

Chinese automakers are moving fast to meet the demand. Volvo Cars, owned outright by Hangzhou, China-based Geely Auto, has already stated it will cease production of fossil fuel-powered vehicles by 2020. On top of that, the company is currently building electric versions of London’s iconic taxis, and Uber is rumored to buy as many as 24,000 electric Volvos.

In October, Great Wall Motors announced its plans to form a joint venture with Germany’s BMW to begin production on a new fleet of EVs. Toward that end, the manufacturer bought a 3.5 percent stake in an Australian lithium-mining company to support long-term development of battery resources and control pricing power.

And although it’s not as big a powerhouse as its peers, relative newcomer Guangzhou Automobile Group also has high ambitions to introduce EVs in as many as 14 global markets including North America, Africa, South and Eastern Europe and South East Asia. It recently signed an agreement with tech behemoth Tencent to cooperate on artificial intelligence (AI)-driving and “smart” vehicles.

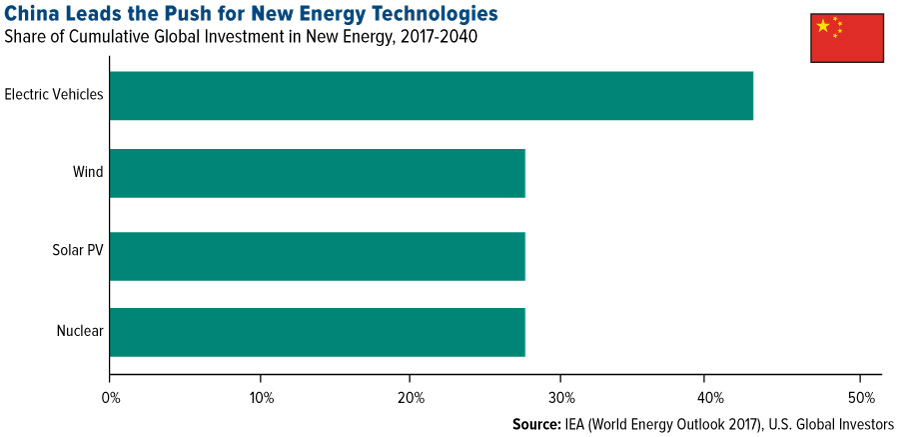

Looking ahead to 2040, China is forecast to capture more than 40 percent of the world EV market, according to a recent report from the International Energy Agency (IEA), as well as nearly 30 percent of total new wind, solar and nuclear capacity additions.

As for the European market, Germany is expected to outpace its neighbors in adopting EVs as Volkswagen (DE:VOWG_p), the world’s number one automaker by sales, seeks to become a global leader in electric and self-driving cars. The Wolfsburg-based company announced plans to invest as much as $40 billion over the next five years to expand its selection of EVs.

China’s Campaign Against Pollution to Could Drive Global Energy Trends

China’s interest in EVs is only part of a much broader effort to improve its deteriorating air quality. Faced with worsening smog in large East Coast cities, the Asian giant has ordered thousands of factories and manufacturers, especially those that burn coal, to shut down in accordance with the government’s four-year climate action plan. The capacity cuts are contributing to higher metals prices, with the S&P GSCI Industrial Metals Index having gained more than 24 percent year-to-date.

Take a look at the following chart courtesy of the IEA. Whereas President Donald Trump is seeking to revitalize coal mining in the U.S., coal demand in China, the world’s largest energy consumer, is expected to decline nearly 500 million tonnes of coal equivalent (mtce) between 2016 and 2040. This comes after demand stood at more than 2 billion tonnes between 1990 and 2016. Instead, the country is actively pivoting into cleaner-burning natural gas and renewables such as wind, solar and hydro.

According to the Wall Street Journal, coal power production in China was negative for the second straight month in October, bringing 2017 growth to negative 3 percent. Hydropower output, on the other hand, grew 17 percent.

Lots of Room for Potential Growth

Returning to EVs, adoption isn’t currently widespread across the globe, with only 14 large metropolitan areas accounting for roughly a third of all sales, according to a recent report by the International Council on Clean Transportation (ICCT). The group highlights 20 “electric vehicle capitals” of the world, where EV sales beat the global norm in the past two years. China claimed seven of these cities, Europe a further seven. Only four U.S. cities made the list: New York City, Los Angeles, San Francisco and San Jose.

Local laws and ordinances have inevitably played a huge role in speeding up the transition from gas-powered to electric cars. In Shenzhen, for instance, all public buses must be emission-free by the end of the year, making it the first city in the world to have an all-electric fleet. Beijing will be replacing all 69,000 of its taxis with EVs. And Qingdao, about midway between Shenzhen and Beijing, is offering consumers subsidies of between $5,000 and $9,000 per electric vehicle.

Like blockchain technology and cryptocurrencies, electric vehicles are still in the early innings, with great potential growth still ahead.

Metals Gaining Leadership in Commodities Space

As I’ve pointed out a number of times before, this is all very constructive for copper, cobalt, lithium and other metals that are used predominantly in the production of EVs. On average, an electric vehicle requires three to four times as much copper as a car with a traditional internal combustion engine.

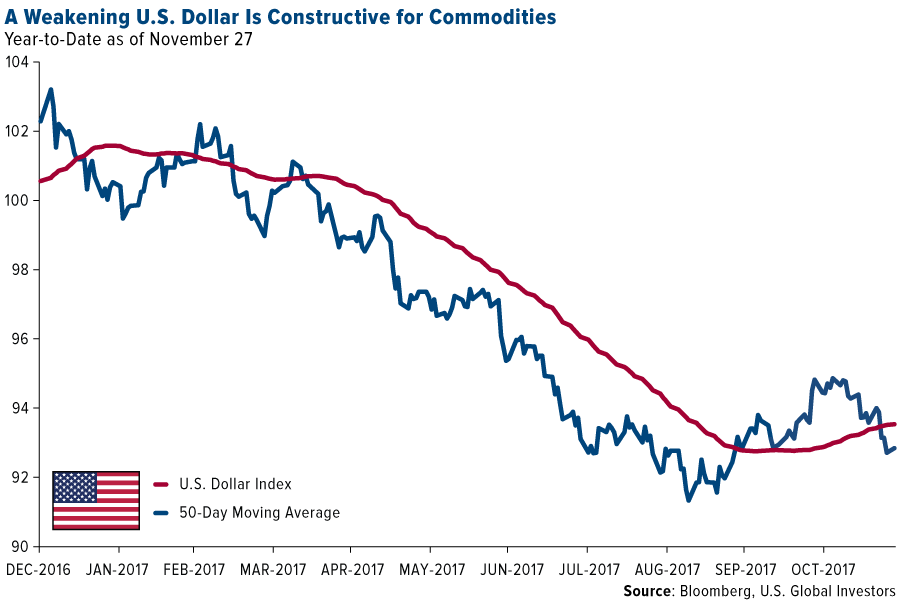

The red metal is one of the best performing materials for the 12-month period, currently up more than 17 percent on increased demand and a weakening U.S. dollar. Over the same period, cobalt has returned an incredible 112 percent.

In a Bloomberg Intelligence report this week, commodity strategist Mike McGlone says that “positive second-half commodity-market momentum is set to accelerate in 2018,” adding that “metals are poised to sustain leadership, particularly as the dollar has peaked.”

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The U.S. Dollar Index is an index (or measure) of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S.trade partners' currencies.

The S&P GSCI Industrial Metals Index provides investors with a reliable and publicly available benchmark for investment performance in the industrial metals market.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 9/30/2017: BHP Billiton Ltd., Geely Automotive Holdings Ltd., Guangzhou Automobile Group Co., Great Wall Motor Co. Ltd., Tencent Holdings Ltd.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes 6 winning stock portfolios chosen by our advanced AI. In 2024 alone, ProPicks AI identified 2 stocks that surged over 150%, 4 additional stocks that leaped over 30%, and 3 more that climbed over 25%. Which stock will be the next to soar?

Unlock ProPicks AI