- Slump in Chinese trade numbers weighs on risk-linked assets

- Dollar waiting for US inflation test, yen retreats after wage data

- Stocks bounce back despite Apple’s troubles, gold trades quietly

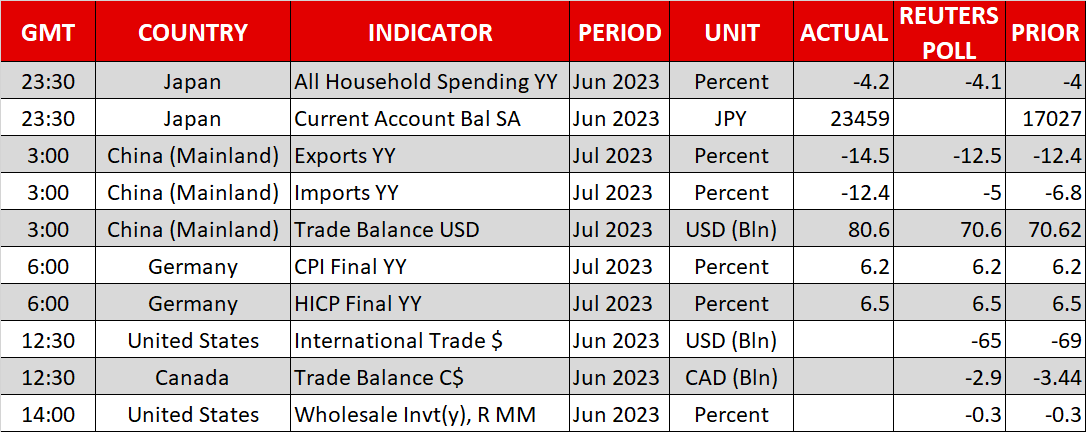

China’s trade slump

The slowdown in the world’s second-largest economy seems to be deepening, as the dual crises in the manufacturing and real estate sectors have dampened growth momentum. Earlier today, China’s latest trade data revealed a worsening contraction in exports and imports, which is a warning sign that both international and domestic demand is losing power.

Amplifying these concerns was a major Chinese property developer - Country Garden - which missed two dollar bond coupon payments today. The home builder cited “liquidity stress” and blamed a worsening backdrop for sales, reviving fears about a potential default and pushing its shares 15% lower.

Chinese authorities have unveiled a plethora of stimulus measures lately to counter the economic slowdown, but investors have been underwhelmed by the scope and size of these policies, as they seem to lack the firepower necessary to truly kickstart growth. Behind this reluctance lie concerns about elevated debt levels, particularly in the private sector.

Investors responded by dumping China-linked assets, with oil prices and Hong Kong equities taking the most damage, alongside currencies of economies that rely on Chinese demand to absorb their commodity exports, namely Australia and New Zealand. If China’s inflation stats tomorrow confirm that the economy has fallen into deflation, these moves could persist.

Dollar gains, yen retreats as wage growth slows

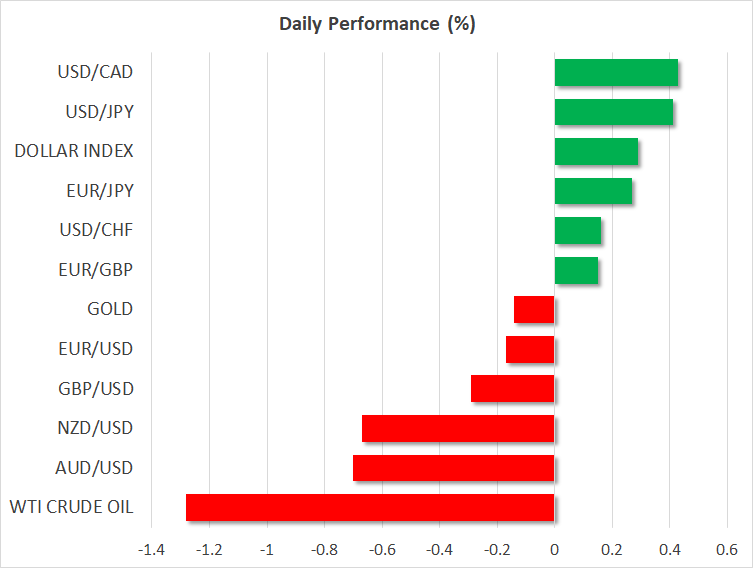

The US dollar advanced against all major currencies on Tuesday, boosted by a general flight to safety that was also evident in the bond market as global yields edged lower. Looking ahead, the main event of the week will be the US inflation report on Thursday, which could inject some volatility into financial markets as there is some scope for higher-than-expected CPI prints.

Commodity prices rose steadily in July, business surveys revealed a reacceleration in inflationary pressures, and the Cleveland Fed's inflation Nowcast model suggests that both the headline and core CPI rates could come in much hotter than what economists anticipate. Coupled with the US Treasury increasing its debt issuance both in size and duration, a hot CPI report could put upward pressure on US yields, helping to revitalize the dollar.

Elsewhere, the Japanese yen came under renewed selling interest following the release of the nation’s wage growth numbers. Labor cash earnings rose by 2.3% in June, a slowdown from the previous month, which was revised higher to 2.9%. The yen usually shines on days where global yields and stocks are falling, so its underperformance today suggests that traders interpreted the softer wage data as an obstacle to further policy tightening by the Bank of Japan.

Equities remain volatile, gold grinds lower

Stocks on Wall Street staged a comeback on Monday. The S&P 500 gained nearly 1% to more than erase its losses from Friday, even as the market’s most prominent general - Apple (NASDAQ:AAPL) - extended its post-earnings retreat. That said, futures have turned lower again today, likely spooked by China’s worsening slowdown.

All told, the equity rally this year has been striking considering that corporate earnings are down by around 5% from last year. Therefore, this rally was built purely on an expansion in valuation multiples, even despite the sharp rise in yields since spring that normally compresses valuations. Fading recession fears and liquidity injections have helped stocks ignore the adverse signals from bonds and earnings, but it’s questionable whether this dynamic can persist for long.

Finally, gold prices have resumed their retreat. It seems that the recovery in the dollar has overpowered the decline in real yields this week, keeping bullion on the back foot. A hotter-than-expected CPI report on Thursday could exacerbate gold’s troubles, turning the spotlight towards the $1,900 region, where the 200-day moving average has also converged.