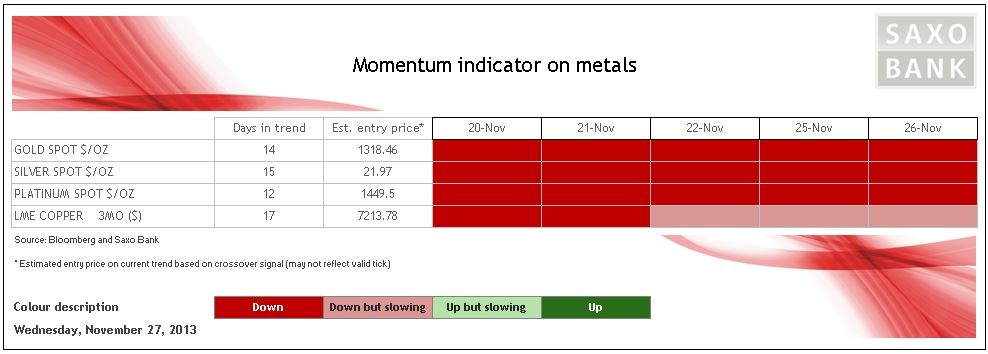

Both precious metals (gold and silver) and platinum group metals (platinum and palladium) have maintained their negative momentum despite a small recovery since Monday. Silver continues to be the weakest of them all and has so far failed to receive any support from the bounce in copper over the past week.

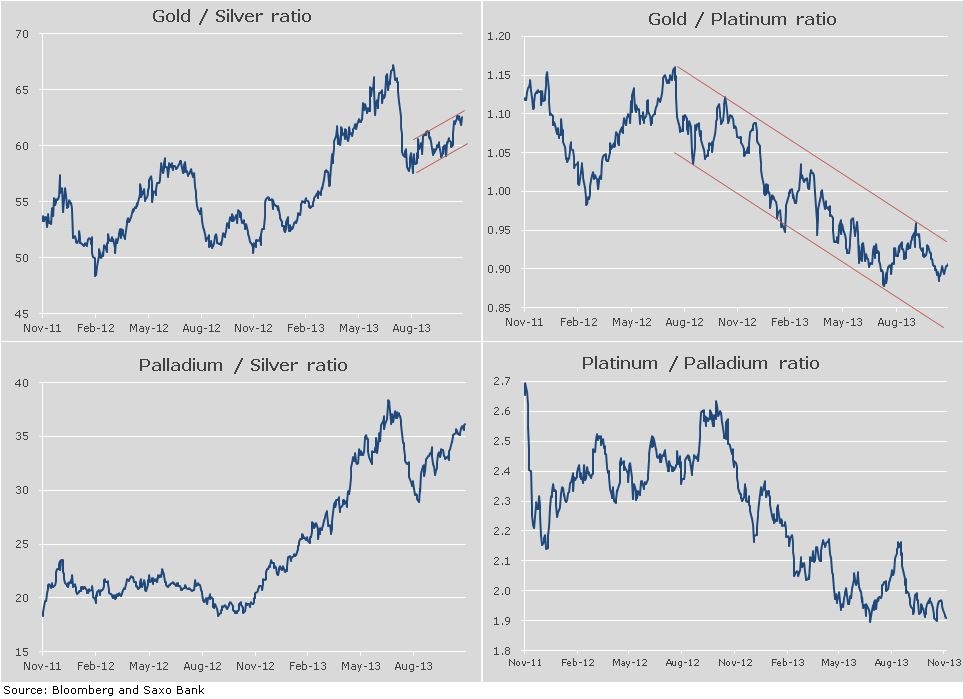

Looking at the ratios between the four metals, the current rank from weakest to strongest is as follows: silver, platinum, gold and palladium. One ounce of gold currently costs 62.6 ounces of silver, which is close to a three-month high, while palladium has resumed its outperformance of platinum. The ratio between the two is currently trading near an 11-year low as the outlook for palladium continues to favour this metal over platinum.

The momentum remains negative overall, with copper being the only metal showing a slowdown following the bounce back above USD 3.2/lb earlier in the week. The renewed selling of JPY this week has provided an improved risk sentiment, but so far stock markets continue to receive most of the attention. The recent sharp decline in gold and the subsequent USD 30-plus bounce may have given short sellers something to think about, which may lend some near-term support. Further improved sentiment towards gold and silver may require weaker-than-expected economic data from the US, something that has been in short supply so far this month. The current numbers continue to support speculation about an earlier-than-expected taper by the US Federal Reserve, which is continuing to put the sector under pressure.

We have today been challenging the steep downtrend from the late October highs. If a sustained break above 1,253 USD/oz occurs, some further consolidation could see the price move towards 1,260 USD/oz and possibly 1,268 USD/oz — but probably not much further than that at this stage.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Metals Are Higher, But Momentum Remains Negative

Published 11/28/2013, 04:45 AM

Updated 03/19/2019, 04:00 AM

Metals Are Higher, But Momentum Remains Negative

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.