Gold hasn’t provided much protection against spiraling inflation this year, but things are finally changing. With traders looking for inflation hedges, rising geopolitical tensions, and favorable seasonals, this party could keep going for a few months. Sadly though, it may prove to be a bear market rally as a slowdown in inflation and rising interest rates next year ultimately take the shine off the precious metal.

Gold strikes back

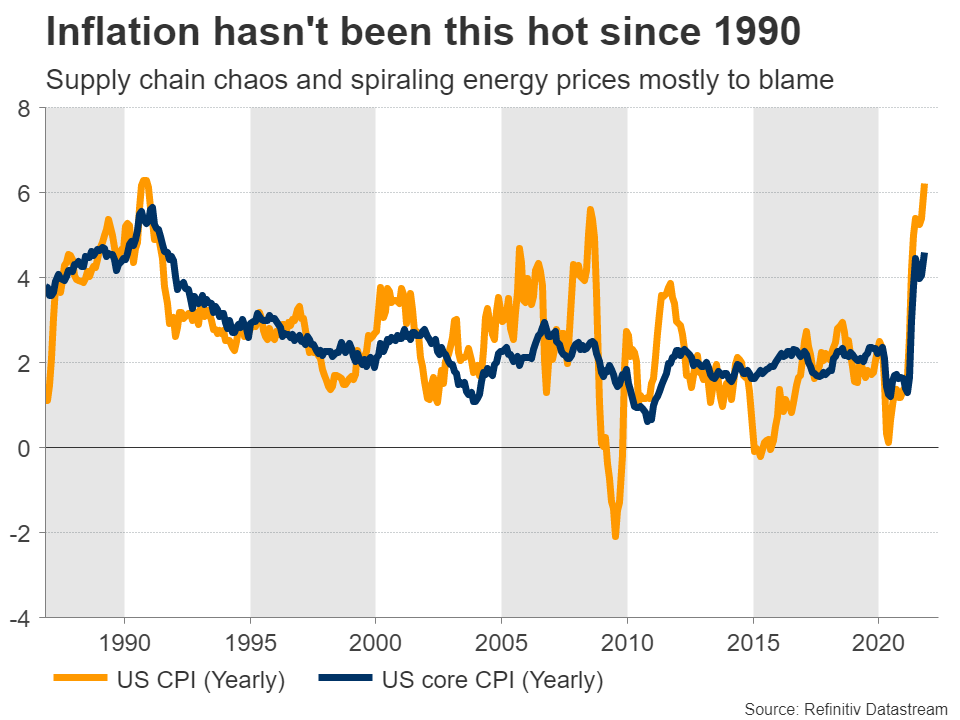

For centuries, gold has been the supreme place to hide whenever there was instability in the world or inflation got out of hand. But in this crisis, it didn’t really behave as an inflation hedge. Every time inflation surged, gold prices got smashed. The logic was that central banks would be forced to fight soaring inflation by raising interest rates, which is negative for bullion.

That pattern finally broke last week. US inflation accelerated to the fastest pace in three decades, propelling the dollar and bond yields much higher as investors priced in faster rate increases by the Fed - but gold still moved higher.

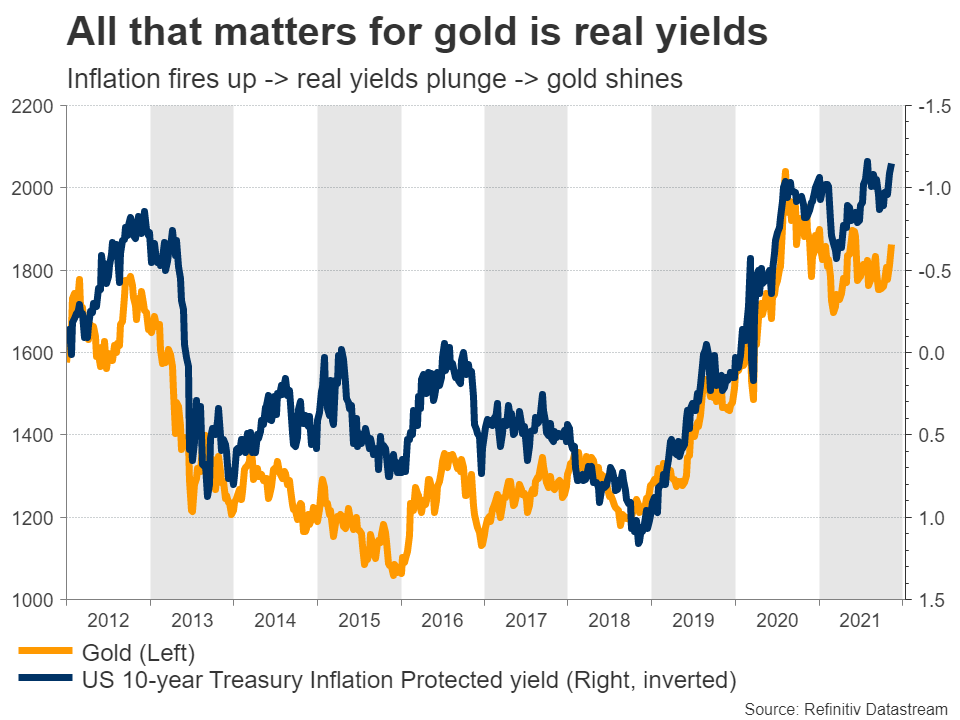

The simple way of reading this is that bullion is becoming an inflation hedge again. To be more precise, the precious metal is benefiting from the weakness in ‘real’ Treasury yields. Let’s explain.

Real yields matter most

The US Treasury issues bonds called Inflation-Protected Securities. These bonds are linked to the inflation rate and pay a higher coupon if inflation fires up, essentially protecting the investor from any inflationary spike. The return on these securities is called the ‘real’ yield.

When traders or funds want protection against inflation, they buy these inflation-protected bonds. But when everyone rushes to buy the same bonds, the yield drops. That’s precisely what boosted gold lately. Gold is very sensitive to real yields. Since the metal pays no interest to hold, it becomes more attractive when real yields fall. The opposite is true as well.

So this was a complicated way of saying yes, gold is behaving like an inflation hedge again. But not because fund managers are suddenly lining up to buy the metal per se. Rather, it is because real yields have fallen so much as everyone rushes to buy inflation-protected bonds, indirectly bringing gold back in fashion.

What’s next?

The burning question now is whether this rally can continue. It probably can, for a variety of reasons. First and foremost, the inflation story could get even spookier in the coming months. The supply chain doesn't seem to be getting better, wages are firing up, and price pressures seem to be broadening out into different sectors of the US economy like rents and medical care.

That could fuel demand for inflation hedges even further, keeping real rates pinned near record lows. The Fed is still buying truckloads of those inflation-protected bonds each month, even if the pace of its purchases will slow down now that the tapering process has commenced.

Geopolitical tensions have also intensified. Two theaters deserve close attention - Taiwan and Ukraine. For months now China has been conducting military exercises around Taiwan, which it considers a runaway province. Similarly, Russia has been amassing troops next to Ukraine, leading America to warn an invasion may be imminent. Neither is likely to escalate into actual war, but the risk alone could be enough to boost safe-haven demand for gold.

The last leg of the bull argument is favorable seasonality. Even though seasonal patterns shouldn’t really work in ‘efficient’ markets, they apparently work in gold, which has a history of performing well in January. Bullion has gained in the last 8 out of 10 Januaries, and in recent years, traders seem to be frontrunning this pattern from December.

But the big picture isn’t so bright

Having said all that, it’s difficult to envision any rally being sustained for long. Everything hinges on inflation staying scorching hot, but there is a strong chance that inflationary pressures will cool towards the end of next year.

The chaos in supply chains will eventually subside, more energy production is coming back online, and year-over-year comparisons will become much tougher from April onwards, artificially lowering the yearly CPI rate. And if inflation doesn’t cool by itself, central banks will raise rates enough to bring it down.

In other words, this is the goldilocks environment for gold. It could persist for a while longer, but heading into the middle of next year, all bets are off. Real yields can’t stay this depressed forever with central banks raising rates.

Enjoy the party while it lasts, but don’t stick around too long.