Markets traded in narrow ranges today as investors sat on the sidelines as they await the release of the all-important US non-farm payrolls figure. Investors are also looking to the European Central Bank Mario Draghi after he signalled that the bank will be doing more to fight the debt crisis. His condition was that Eurozone governments would have to work towards some sort of a fiscal union. The EUR/USD is closing the Asian session at 1.3458 while the GBP/USD is trading below 1.5680.

In other news, the US Senate rejected the Republican proposal to extend a payroll tax cut till 2013 which would have involved the reduction of the Federal workforce by 10% and the freezing of pay. Standard and Poor’s also cut the credit ratings of the big four Australian banks as the agency tightens its definitions of risks. In more sobering news, Georges Soros, the famed hedge fund manager and philanthropist, has made comments at a New York event that the world financial system not only isn’t functioning but is on the brink of collapse. He stated that the global financial system is in a “self-reinforcing process of disintegration” which may have disastrous consequences. The Australian dollar closed the afternoon at 1.0215.

Equity markets were relatively subdued today. The MSCI Asia Pacific Index is largely unchanged with the Nikkei rising 0.4% to 8,632 while the Hang Seng is down 0.42% to 18,922. The ASX 200 has closed 1.4% higher to 4,288 closing the best week for Australian shares in 3 years. Consumer staples and financials led the way. The news was not so good in China as stocks headed for the fourth straight weekly loss as falling property prices and a slump in manufacturing weighed on the markets.

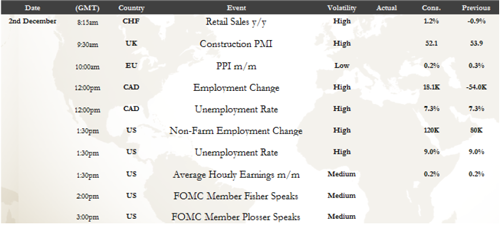

Commodity prices consolidated after a very eventful week. WTI Crude Oil is unchanged trading just above $100.00 as supply concerns were heightened with increasing tensions surrounding Iran. Precious metals gained with gold higher by 0.44% to $1,747 while silver gained 0.54% to $32.94. Soft commodities were mixed while copper gained 0.37%. Tonight we have the release of Swiss Retail Sales, UK Construction PMI, Canadian Employment Change and the US Non-Farm Payrolls.

GOLD was quiet yet again in Asia today as recently strong gains have seen profit taking set in and consolidation has been the theme prior to major short-term resistance and payrolls data in the US tonight. Gold held up very well throughout the session even as equities retreated and the USD managed to post some minor gains. Gold traded in a $1,737-46 range and finished the session stronger by 0.40% at $1,745. Another tight range and resistance towards $1,750/52 continued to limit gains ahead of key US payrolls data tonight. We did see the US senate reject the Payrolls Tax Bill today and this did cause some brief USD strength but was ultimately expected. Australian Banks were also downgraded but after early losses the banks paired gains. This left little direction for Gold until payrolls as the USD steadies and equities see small declines. Gold could be a very big mover tonight and we continue see big risks to the upside in the short-term and we could hit $2000 by years end. Major ST resistance at 41,750/52 is holding firm and we must see this area taken out tonight otherwise we could see some further profit taking back towards support at $1,700/11. We favour buying dips down to $1,735 tonight with stops below $1,711 and look for the break of $1,750 if payrolls improve.

AUD/USD closes the day slightly lower as the market expectations of a rate cut at next week’s last RBA meeting for the year grow on the back of the actions seen from the Big 6 Central Banks to help the state of the global economy. Also, helping the change in rates is that there is no January meeting and the mar-kets don’t believe that Gov. Stevens could wait despite his normal reluctance to change anything. The AUD/USD price dipped to 1.0206 during the afternoon after earlier in the day trying to get above 1.0250 offers.

The sideways pattern that is being seen across the market will likely continue into the US morning, as the fear of a better than expected US Non-Farm number builds around the markets. The level that we will be watching is a break above 1.0260 to see a possible squeeze back to the weekly high of 1.0330. Anything above this has to be unlikely whilst a move back to 1.0150 is our favoured option. A break below after payrolls could get nasty!

In other news, the US Senate rejected the Republican proposal to extend a payroll tax cut till 2013 which would have involved the reduction of the Federal workforce by 10% and the freezing of pay. Standard and Poor’s also cut the credit ratings of the big four Australian banks as the agency tightens its definitions of risks. In more sobering news, Georges Soros, the famed hedge fund manager and philanthropist, has made comments at a New York event that the world financial system not only isn’t functioning but is on the brink of collapse. He stated that the global financial system is in a “self-reinforcing process of disintegration” which may have disastrous consequences. The Australian dollar closed the afternoon at 1.0215.

Equity markets were relatively subdued today. The MSCI Asia Pacific Index is largely unchanged with the Nikkei rising 0.4% to 8,632 while the Hang Seng is down 0.42% to 18,922. The ASX 200 has closed 1.4% higher to 4,288 closing the best week for Australian shares in 3 years. Consumer staples and financials led the way. The news was not so good in China as stocks headed for the fourth straight weekly loss as falling property prices and a slump in manufacturing weighed on the markets.

Commodity prices consolidated after a very eventful week. WTI Crude Oil is unchanged trading just above $100.00 as supply concerns were heightened with increasing tensions surrounding Iran. Precious metals gained with gold higher by 0.44% to $1,747 while silver gained 0.54% to $32.94. Soft commodities were mixed while copper gained 0.37%. Tonight we have the release of Swiss Retail Sales, UK Construction PMI, Canadian Employment Change and the US Non-Farm Payrolls.

GOLD was quiet yet again in Asia today as recently strong gains have seen profit taking set in and consolidation has been the theme prior to major short-term resistance and payrolls data in the US tonight. Gold held up very well throughout the session even as equities retreated and the USD managed to post some minor gains. Gold traded in a $1,737-46 range and finished the session stronger by 0.40% at $1,745. Another tight range and resistance towards $1,750/52 continued to limit gains ahead of key US payrolls data tonight. We did see the US senate reject the Payrolls Tax Bill today and this did cause some brief USD strength but was ultimately expected. Australian Banks were also downgraded but after early losses the banks paired gains. This left little direction for Gold until payrolls as the USD steadies and equities see small declines. Gold could be a very big mover tonight and we continue see big risks to the upside in the short-term and we could hit $2000 by years end. Major ST resistance at 41,750/52 is holding firm and we must see this area taken out tonight otherwise we could see some further profit taking back towards support at $1,700/11. We favour buying dips down to $1,735 tonight with stops below $1,711 and look for the break of $1,750 if payrolls improve.

AUD/USD closes the day slightly lower as the market expectations of a rate cut at next week’s last RBA meeting for the year grow on the back of the actions seen from the Big 6 Central Banks to help the state of the global economy. Also, helping the change in rates is that there is no January meeting and the mar-kets don’t believe that Gov. Stevens could wait despite his normal reluctance to change anything. The AUD/USD price dipped to 1.0206 during the afternoon after earlier in the day trying to get above 1.0250 offers.

The sideways pattern that is being seen across the market will likely continue into the US morning, as the fear of a better than expected US Non-Farm number builds around the markets. The level that we will be watching is a break above 1.0260 to see a possible squeeze back to the weekly high of 1.0330. Anything above this has to be unlikely whilst a move back to 1.0150 is our favoured option. A break below after payrolls could get nasty!