The great 'Sandy debate' is on. U.S. economic data is coming in weaker than expected and some argue that it can't all be explained by the hurricane. Case in point is the initial jobless claims report from last week.

Econoday: Hurricane or not, it's hard to ignore an incredible 78,000 surge in initial jobless claims for the November 10 week to 439,000. Adding to the pressure is a 6,000 upward revision to the prior week to 361,000. The four-week average is up a very sizable 11,750 to a 383,750 level that is more than 15,000 above month-ago levels which does not point to improvement for November payroll growth or the unemployment rate.

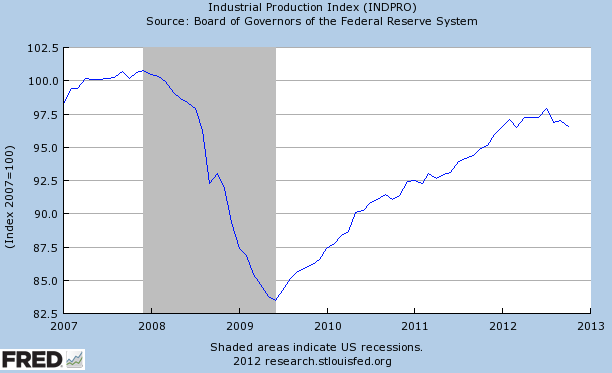

Another example is the U.S. industrial production, which clearly looks like it has stalled.

So far the explanation has been that Hurricane Sandy disrupted production in late October, causing this decline.

NYTimes: Industrial production fell unexpectedly in October because of Hurricane Sandy, the Federal Reserve reported on Friday, but factory growth appeared at a standstill even aside from the storm.

Production at the nation’s mines, factories and refineries contracted 0.4 percent last month, after a 0.2 percent increase in September, the Fed said. It said the storm, which hit the East Coast at the end of October, cut output by nearly 1 percentage point. Utilities and producers of chemicals, food, transportation equipment, and computers and electronic products were the most affected, it said.

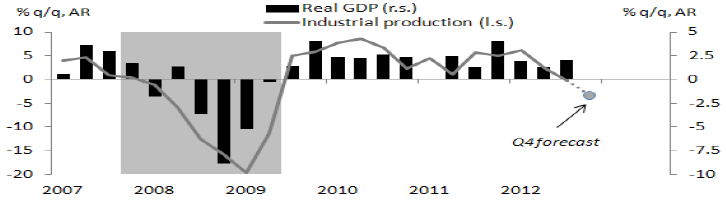

Does that mean we should dismiss these results as temporary? Some suspect that the U.S. industrial output would have been weak event without the hurricane. DB economists also think that the weakness will persist through November, dramatically lowering the U.S. GDP (below 1.3% annualized). According to DB the quarter-over-quarter changes in industrial production (IP) have an 83% correlation to the GDP. And the bank is forecasting a material Q4 decline in IP. The recent weakness may not be as transient as some expect.

DB: If the November decline [in IP] matches that of October, the annualized change [in IP] will be -3.4%. While there have been occasions in recent history when industrial production contracted but real GDP growth remained positive, weakness in the former is generally an ominous sign for the latter.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

How Transient Is The 'Sandy Effect' On Economic Data?

Published 11/19/2012, 11:35 AM

Updated 07/09/2023, 06:31 AM

How Transient Is The 'Sandy Effect' On Economic Data?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2025 - Fusion Media Limited. All Rights Reserved.